Imagine you have just completed your dream home in Meerut, Uttar Pradesh, after months of meticulous planning and a significant financial investment. The plaster is fresh, and the premium electrical wiring—which typically accounts for 10–18% of your total construction cost—is safely concealed behind the walls. Suddenly, an unusually heavy monsoon triggers localized flooding or a short circuit leads to a devastating fire. In minutes, your hard-earned asset is compromised, leaving you with repair bills that could run into lakhs. This is a harsh reality many face in North India due to evolving climate risks and increasing natural calamities like earthquakes or flash floods. To protect your investment, understanding what is home insurance in India has become more critical than ever for every homeowner, contractor, and builder in 2026.

As construction costs in India continue to rise, with high-end apartments in cities like Gurgaon or Mumbai requiring defensible, line-itemized data for any repair, you cannot afford to leave your property’s shell unprotected. What is home insurance in India? Put simply, it is a specialized financial safeguard designed to cover the cost of repairing or rebuilding the physical framework of your house and its contents if they are damaged by an insured peril like fire, flood, or theft. Since 2021, the IRDAI has standardized this landscape through the Bharat Griha Raksha policy, ensuring that every homeowner has access to uniform and transparent protection. For a detailed breakdown of protections, read our guide on what is covered by building insurance in India.

For a construction estimator or builder, home insurance is no longer an afterthought; it is a vital component of modern project estimation and risk management. In this comprehensive guide, we will explore the nuances of home insurance India 2026, the specific protections offered by the Bharat Griha Raksha policy, and how you can accurately factor these costs into your financial planning.

What Exactly is Home Insurance in India?

At its core, home insurance in India is a policy that covers the “shell” or the physical anatomy of your property, and often, the precious items kept within it. If you were to take your house, turn it upside down, and shake it, everything that stays attached is generally what the “Building Cover” protects. This includes the foundation, load-bearing walls, roof, floors, and permanent fixtures like windows, doors, and concealed plumbing systems.

In the Indian context, especially for independent floors in Delhi-NCR or villas in Tier-2 cities like Meerut, this is often referred to as building structure insurance or dwelling coverage. However, a complete home insurance policy typically offers two distinct layers of protection:

- Home Building Cover: This protects the physical structure, including permanent installations such as built-in kitchen cabinets, bathroom fittings, solar panels, and compound walls.

- Home Contents Cover: This protects your movable belongings—electronics, furniture, jewelry, and clothes—against risks like burglary or accidental damage.

It is vital to recognize that since April 2021, the IRDAI mandated a standard product called the Bharat Griha Raksha (BGR) policy, which every general insurance company in India must offer. This policy is designed to restore your home to its original state by covering “reinstatement” costs—the actual price of materials and labor required for reconstruction—rather than just the market value of the property.

Bharat Griha Raksha – The Standard Home Insurance Policy in India

The introduction of the Bharat Griha Raksha policy marked a significant shift in how home insurance India 2026 is delivered. Previously, home insurance was often filled with complex jargon and varied significantly between insurers. Today, BGR provides a uniform level of protection across the country, whether you are buying from a large public sector insurer or a modern digital-first company.

Key features of the Bharat Griha Raksha policy include:

- Uniform Tenure: These policies are available for a tenure ranging from 1 to 10 years, offering long-term peace of mind for homeowners.

- Automatic Contents Cover: A standout feature is that if you insure your home structure, the policy automatically includes cover for general home contents (up to 20% of the sum insured for the building, capped at ₹10 lakh) without requiring a detailed list of items.

- 10% Annual Auto-Escalation: To account for the rising cost of materials like steel and cement, the sum insured automatically increases by 10% every year during the policy term.

- In-built Benefits: The policy includes coverage for “Loss of Rent” or “Rent for Alternative Accommodation” if your home becomes uninhabitable due to a covered peril.

- No Underinsurance Clause: In many cases, if your sum insured is at least 85% of the actual value, the insurer will not penalize you for being slightly under-insured during a claim—a major relief for homeowners.

Note that standard home insurance does not cover buildings while they are still under construction. For that specific phase, you need a dedicated under construction building insurance policy, also known as Builder’s Risk or Construction All Risk (CAR) insurance.

What Does Home Insurance Cover in India?

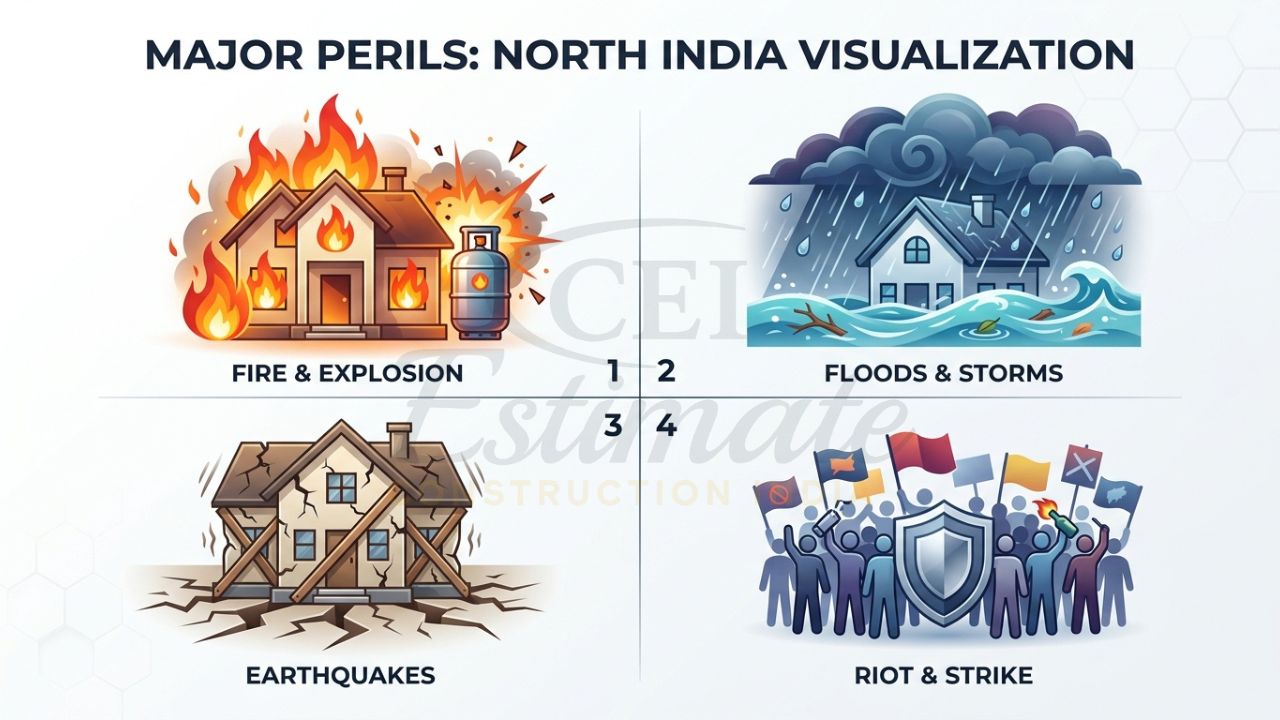

Understanding home insurance coverage India is essential for recognizing the risks you are mitigating. When you purchase home building insurance India, the BGR framework typically covers a wide range of major perils that are particularly relevant to the Indian climate and urban environment.

Natural Calamities and Climate Risks

This is perhaps the most crucial section for residents in North India, including Uttar Pradesh and Delhi-NCR. The policy covers damage from:

- Floods and Storms: Protection against monsoon flooding or cyclonic winds.

- Earthquakes: Vital for seismic zones IV and V, which cover large parts of North India.

- Landslides and Rockslides: Critical for hilly regions or areas with unstable soil.

Accidental and Malicious Hazards

- Fire and Explosion: Covers damage from accidental fires, lightning strikes, or domestic gas cylinder explosions.

- Impact Damage: Damage caused by a vehicle, a falling tree, or even an aircraft.

- Malicious Damage: Coverage against riots, strikes, or acts of terrorism.

Infrastructure Failures

- Water Damage: Bursting or overflowing of water tanks, apparatus, and pipes.

- Theft Following an Event: If a wall collapses due to a storm and theft occurs within 7 days, it is often covered under the standard policy.

Additional In-built Covers

Beyond the main structure, the policy provides financial aid for:

- Debris Removal: Covers the cost of clearing the site after a fire or collapse (up to 2% of the claim amount).

- Professional Fees: Covers fees for architects, surveyors, and consulting engineers (up to 5% of the claim amount) to help you redesign and rebuild.

Home Building Insurance vs Home Contents Insurance

One of the most common mistakes Indian homeowners make is assuming that “home insurance” automatically covers everything. There is a distinct boundary between the structure and what lies within it. For a construction estimator or builder, the focus is usually on the “Building” portion to ensure the project budget accounts for potential total loss scenarios.

| Feature | Home Building Insurance | Home Contents Insurance |

|---|---|---|

| What it Protects | Walls, roof, foundation, plumbing, and fixed wiring. | Furniture, appliances, jewelry, and personal items. |

| Basis of Sum Insured | Reinstatement Value (cost to rebuild). | Market value or replacement value of items. |

| Target Audience | Homeowners and landlords. | Tenants and homeowners. |

| Key Example | Repairing a cracked pillar after an earthquake. | Replacing a laptop stolen during a burglary. |

| Mandatory Status | Often required by banks for home loans. | Purely voluntary. |

Common Exclusions – What is NOT Covered

No insurance policy covers every possible scenario. To avoid disputes with loss assessors—a common issue in the Indian restoration industry—you must be aware of the “Fine Print”. Standard exclusions in home insurance India 2026 include:

- Wear and Tear: Gradual deterioration, rust, or damage caused by lack of maintenance is not covered.

- Willful Negligence: Damage caused intentionally by the insured person or their family members.

- War and Nuclear Risks: Losses arising from war, invasion, or nuclear radiation.

- Pre-existing Damage: Any structural issues or cracks that existed before the policy start date.

- Illegal Constructions: If your home was built in violation of local building codes or on encroached land, claims may be rejected.

- Cash and Valuables: Standard policies usually exclude cash and may require specific add-ons for high-value jewelry or paintings.

How Much Does Home Insurance Cost in India in 2026?

The cost of home insurance in India is surprisingly affordable compared to health or motor insurance. The premium is calculated based on the “Reinstatement Value”—the cost of rebuilding the house (materials + labor)—rather than the market value, which includes the cost of land.

For a typical 1000 sq. ft. house in a city like Meerut, if the construction cost is ₹2,000 per sq. ft., your sum insured should be ₹20 Lakhs. In 2026, realistic premium ranges are:

- Standard Rates: 0.15% to 0.40% of the Sum Insured.

- Sample Premium: For a ₹20 Lakh sum insured, the annual premium is approximately ₹3,000 to ₹8,000.

- High-Value Property: A premium of roughly ₹2,466 annually can sometimes cover properties with a sum insured up to ₹1 Crore depending on the insurer and location.

For builders and estimators, including these premiums in the Bill of Quantities (BOQ) for new homes demonstrates professionalism and ensures the project is protected from day one.

Step-by-Step Guide to Buying Home Insurance in India

Buying home building insurance India in 2026 is a digital-first process. Follow these steps:

- Calculate Reinstatement Value: Use an accurate material and labor breakdown. For example, if your electrical work cost ₹1.8 Lakhs, ensure the total value reflects these finishes.

- Compare Quotes: Use platforms like Policybazaar or go directly to insurer websites like ICICI Lombard, HDFC Ergo, or SBI General.

- Choose Tenure and Add-ons: Consider long-term policies for discounts and add-ons like “Debris Removal” or “Personal Accident” cover.

- Submit Property Details: You will need the property address, carpet area, and age of construction; no physical inspection is usually required for newer buildings.

Claims Process and Tips for Smooth Settlement

If disaster strikes, immediate action is required. In 2026, insurance companies demand line-itemized data and photographic evidence.

- Immediate Intimation: Inform the insurer via their app or toll-free number within 24–48 hours.

- Document Everything: Take high-quality photos and videos of the damage before starting any repairs.

- The Surveyor’s Role: A professional surveyor will visit to assess the loss. Provide them with a defensible estimate or BOQ for repairs using current market rates.

Why Home Builders, Estimators & Homeowners in India Should Buy It?

At Construction Estimator India, we view insurance as a vital component of risk management. For contractors, including home insurance premiums in your project estimates protects your client’s largest financial asset and ensures your professional reputation remains intact even if an unforeseen event occurs. In a state like Uttar Pradesh, which sits on various seismic zones, the cost of the premium is a small price to pay for total peace of mind.

Beyond property protection, responsible contractors also secure insurance for construction workers in India. This covers injuries, accidents, and liabilities during the building phase, making your project safer and more professional.

Contractors and developers can further strengthen their risk management by exploring types of insurance for contractors in India. These policies complement home structure insurance and help safeguard both the project and the business.

For a clear picture of overall project costs, you can also refer to how much is insurance for construction in India.

Conclusion

Protecting your home’s physical framework is not just a financial decision; it is about safeguarding your family’s future. What is home insurance in India? It is your safety net against the unpredictable elements of nature and accidental hazards that can strike without warning. From the foundation to the roof, ensuring your structure is insured allows you to build with confidence in 2026.

Don’t wait for a calamity to strike. Whether you are building a new home in Meerut or managing a development in Delhi-NCR, make insurance a priority. For professional construction cost estimation and BOQ services that properly include insurance costs, contact Construction Estimator India today.

FAQ Section

What is home insurance in India?

Home insurance is a policy that protects your home’s physical structure and its contents against risks like fire, flood, earthquake, and theft.

What is Bharat Griha Raksha policy?

It is a standardized home insurance policy introduced by IRDAI in 2021 that offers uniform coverage across all general insurance companies in India.

Does home insurance cover earthquake and flood in India?

Yes, under the standard Bharat Griha Raksha (BGR) policy, natural calamities like earthquakes and floods are covered by default.

What is the difference between home building and home contents insurance?

Home building insurance covers the permanent structure (walls, roof, fixtures), while contents insurance covers movable items like furniture and electronics.

How is sum insured calculated for home insurance?

It is calculated based on the “Reinstatement Value,” which is the current cost of construction (Area x Cost of construction per sq. ft.), excluding land value.

Is home insurance mandatory in India?

It is not mandatory by law, but banks require it for home loans, and it is essential for RERA compliance during construction.

How much does home insurance cost in India in 2026?

Premiums generally range from 0.15% to 0.40% of the sum insured, making it very affordable.

Can I buy home insurance for an under-construction house?

Standard home insurance is for completed buildings. For properties under construction, you need a “Builder’s Risk” or “Contractor’s All Risk” (CAR) policy.

What is covered under loss of rent in home insurance?

If a covered peril makes your home uninhabitable, the policy pays for the rent you lose from a tenant or the cost of alternative accommodation for yourself.

Which companies offer Bharat Griha Raksha policy?

Every general insurer in India, including HDFC Ergo, ICICI Lombard, and SBI General, is mandated to offer this standardized policy.

Suggestions:

- Learn more about: What is Structure on the Property Insurance?

- Read also: What is Covered by Building Insurance?

- Read our guide on: Difference Between Building Insurance and Home Insurance