Ramesh, a skilled mason working on a luxury villa project in Meerut, Uttar Pradesh, had always been careful. However, during the peak of the 2026 monsoon, a freak scaffolding collapse sent him falling twelve feet onto a pile of reinforcement bars. Within minutes, a productive worker and father of three was incapacitated, and his family faced sudden financial ruin. Fortunately, his contractor had prioritized comprehensive insurance for construction workers in India, ensuring that Ramesh received immediate medical attention and his family was supported through a workmen compensation claim. This real-life scenario underscores why safeguarding your workforce is not just a moral choice but a fundamental pillar of construction management.

The construction industry in India is characterized by its high-risk nature, where falls, electrocution, material collapses, and weather hazards are daily realities for millions of unorganized workers. As a contractor or project owner, providing insurance for construction workers includes mandatory policies like Workmen Compensation Insurance, government-backed schemes under the BOCW Act, and affordable group accident covers. Understanding these options is crucial for legal compliance, project risk management, and preparing an accurate Bill of Quantities (BOQ). In this guide, we will explore the mandatory requirements, costs, and benefits of worker insurance, providing you with a roadmap to protect your team and your business in 2026.

Why Insurance for Construction Workers is Critical in India?

In 2026, India is witnessing a massive infrastructure push, spanning from smart cities in the Delhi-NCR region to high-speed rail corridors. This boom relies heavily on migrant and unorganized workers who are often the most vulnerable. Construction sites consistently report some of the highest accident rates in the country. Without adequate insurance, a single major mishap can lead to crippling legal risks for you, including heavy fines, penalties, and lengthy lawsuits that could freeze your project entirely.

Beyond the legalities, there is a profound social responsibility. Most construction laborers lack a financial safety net. When you provide insurance, you ensure that injury or death does not result in generational poverty for the worker’s family. Furthermore, an insured workforce is often more confident and productive, knowing their well-being is valued. From a management perspective, having insurance prevents project delays caused by labor unrest or sudden liquidity crises resulting from out-of-pocket compensation payments.

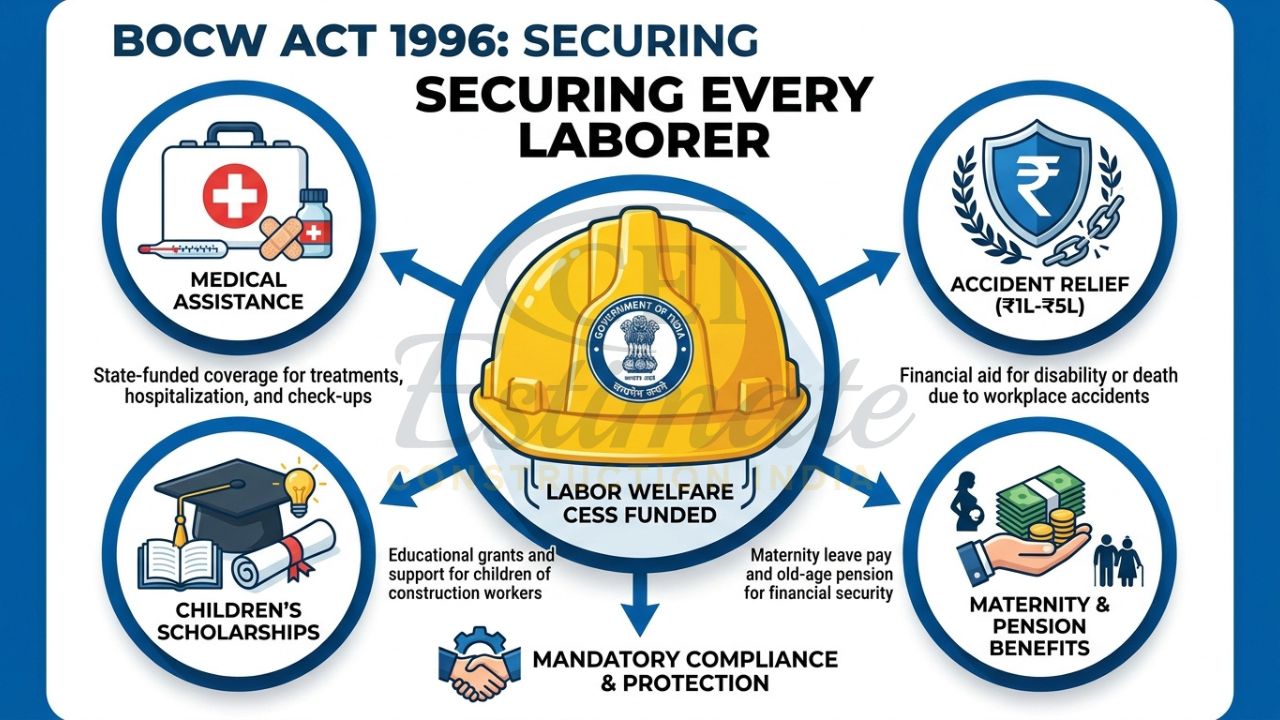

Legal Framework – BOCW Act and Mandatory Requirements

The primary legal backbone for worker safety is the Building and Other Construction Workers (Regulation of Employment and Conditions of Service) Act, 1996 (BOCW Act). This act mandates that every construction establishment must register its workers with the state’s BOCW Welfare Board. In states like Uttar Pradesh and Haryana, the government collects a labor welfare cess—typically 1% to 2% of the total project cost—to fund welfare measures, including insurance, health aid, and maternity benefits.

Compliance is no longer a “good-to-have” feature; it is mandatory. Non-compliance can lead to penalties exceeding ₹50,000 or even imprisonment in severe cases. Furthermore, the Code on Social Security 2020 has strengthened these protections by expanding the definition of workers and digitizing the registration process. As a contractor, you must ensure that every worker on your site is registered, enabling them to access state-level accident relief and insurance benefits that supplement your private policies.

Main Types of Insurance for Construction Workers in India?

Navigating the landscape of insurance for construction workers in India requires understanding the different layers of protection available:

1. Workmen Compensation Insurance (WCI)

Commonly known as Employer’s Liability insurance, this is mandatory under the Employees’ Compensation Act, 1923. It covers your legal liability to pay compensation to workers in case of death, permanent total disability (PTD), permanent partial disability (PPD), or temporary disability arising out of and in the course of employment. The sum insured is typically calculated based on the worker’s age and monthly wages.

2. Pradhan Mantri Suraksha Bima Yojana (PMSBY)

For just ₹20 per year, this government scheme offers accidental death and disability cover of ₹2 lakh. It is an incredibly affordable way to add an extra layer of protection for your laborers. You can facilitate their enrollment through their Jan Dhan bank accounts.

3. BOCW Welfare Board Benefits

Registered workers gain access to state-specific benefits. These include immediate accident relief (often between ₹1 lakh to ₹5 lakh), medical assistance, and even educational scholarships for their children.

4. Group Personal Accident (GPA) Insurance

While WCI covers work-related incidents, a GPA policy can provide 24/7 protection for your core team, covering accidents even outside the construction site.

| Insurance Type | Core Benefit | Annual Cost (Approx) | Mandatory? |

|---|---|---|---|

| Workmen Compensation | Legal liability for site injuries/death | 0.5% – 2% of wage bill | Yes |

| BOCW Registration | State-funded welfare & medical aid | 1-2% Project Cess | Yes |

| PMSBY | ₹2 lakh accidental death cover | ₹20 per worker | Recommended |

| Ayushman Bharat | ₹5 lakh health cover (Hospitalization) | Government Funded | For eligible |

As a contractor handling full projects, you should also review types of insurance for contractors in India to build a comprehensive risk strategy.

What Does Workmen Compensation Insurance Cover?

A Workmen Compensation policy is the cornerstone of site safety. It provides a structured payout for various unfortunate events:

- Death Benefit: A lump sum amount paid to the worker’s dependents, calculated based on the worker’s age and monthly wages (subject to statutory limits).

- Permanent Total Disability (PTD): Paid if the worker loses the ability to perform any work (e.g., loss of both limbs or sight).

- Permanent Partial Disability (PPD): Compensation for the loss of a finger, a single limb, or hearing, which reduces the worker’s earning capacity.

- Medical Expenses: Reimbursement for hospitalization and treatment costs resulting from a site accident.

- Occupational Diseases: Coverage for illnesses like silicosis or asbestosis that develop due to long-term exposure to construction dust and chemicals.

For accurate project budgeting, refer to our detailed analysis on how much is insurance for construction in India.

Common Exclusions and Limitations

While insurance provides a safety net, you must be aware of typical exclusions to ensure claims are not rejected:

- Intoxication: Claims are generally denied if the worker was under the influence of alcohol or drugs at the time of the accident.

- Willful Negligence: If a worker intentionally ignores safety protocols or fails to use provided safety gear (like harnesses), the insurer may contest the claim.

- Non-Employment Injuries: Injuries occurring during a worker’s personal time or commute (unless provided by the employer) are often excluded from WCI.

- Pre-existing Conditions: Disability resulting from a condition that existed before employment began.

- War and Nuclear Risks: Standard exclusions across most Indian insurance products.

How Much Does Insurance for Construction Workers Cost in India?

In 2026, the cost of workmen compensation insurance in India is relatively affordable, usually ranging from 0.5% to 2% of the total wage bill. For instance, if your annual labor payroll for a project in Noida is ₹50 lakhs, the premium could range between ₹25,000 and ₹1,00,000.

Several factors influence this cost:

- Risk Class: Workers handling heavy machinery or working at great heights (high-rise residential) attract higher premiums than those in finishing or painting roles.

- Location: Projects in high-risk seismic zones or remote areas may see slight variations.

- Safety Records: Contractors with a history of zero accidents can often negotiate lower premiums.

For estimators, it is vital to include worker insurance in the BOQ. Treating insurance as a separate line item ensures that the project budget remains realistic and that you aren’t forced to cut corners on safety when costs escalate. For full project coverage during the building phase, explore construction all risk insurance in India.

Step-by-Step Guide for Contractors to Arrange Insurance

- Register with BOCW: Ensure your firm and your workers are registered with the State Labor Department to comply with cess requirements.

- Assess the Wage Bill: Calculate the total number of workers and their average monthly wages to determine the required sum insured for WCI.

- Choose a Reputable Insurer: Compare quotes from leading providers like New India Assurance, ICICI Lombard, or HDFC Ergo. Ensure the policy specifically mentions “Workmen Compensation.”

- Enroll Workers in PMSBY/PMJJBY: Help your workers link their bank accounts to these government schemes for low-cost life and accident cover.

- Maintain Documentation: Keep clear records of worker attendance, wage slips, and safety training logs. These are essential during the claims process.

Many contractors also secure dedicated protection for the structure itself. Learn more in our guide on what is covered by building insurance.

Claims Process and Best Practices

If an accident occurs, speed and accuracy are paramount. Immediately report the incident to the insurance company and the local labor commissioner. Secure medical reports, police FIRs (if required), and photographs of the accident site. Maintain a detailed “Incident Log” that includes witness statements. Proper documentation ensures that the insurance company cannot reject the claim on technical grounds, allowing the worker to receive their payout without unnecessary delays.

Why Estimators and Contractors Must Factor Worker Insurance into Project Costs?

At Construction Estimator India, we emphasize that insurance is a non-negotiable project expense. Under-bidding by ignoring insurance for construction workers in India is a recipe for disaster. If an accident happens and you aren’t covered, the resulting compensation could exceed your entire profit margin. Including insurance premiums in your tenders protects your financial liquidity and establishes you as a professional, law-abiding contractor.

For detailed protection of buildings while they are still being constructed, see our article on insurance for building under construction in India.

Conclusion

Providing comprehensive insurance for construction workers in India is the most effective way to manage the inherent risks of our industry. By combining mandatory Workmen Compensation Insurance with state BOCW benefits and affordable government schemes like PMSBY, you create a robust safety net for your team. In 2026, compliance is not just about avoiding fines; it is about building a sustainable, ethical, and resilient construction business.

Don’t leave your project’s future to chance. Ensure your workforce is fully protected and your project costs are accurately calculated. Contact Construction Estimator India today for professional BOQ and construction cost estimation services that account for every compliance and insurance cost, ensuring your projects are both safe and profitable.

FAQ Section

What is insurance for construction workers in India?

It refers to a combination of mandatory and voluntary policies—such as Workmen Compensation Insurance and BOCW Welfare schemes—that provide financial compensation for workers in case of site accidents, disability, or death.

Is Workmen Compensation Insurance mandatory for construction sites?

Yes, under the Employees’ Compensation Act, 1923, any employer in a hazardous industry like construction is legally liable to compensate workers for employment-related injuries or death.

What benefits are available under BOCW Act for construction workers?

Registered workers can receive accident relief, medical assistance, maternity benefits, pensions, and educational support for their children through state welfare boards.

How does Pradhan Mantri Suraksha Bima Yojana help construction workers?

PMSBY provides a very affordable accidental death and disability cover of ₹2 lakh for a premium of just ₹20 per year, which is ideal for low-income laborers.

What does Workmen Compensation Insurance cover in case of worker death?

It provides a lump sum payment to the worker’s legal heirs, calculated based on the worker’s age and monthly salary at the time of the incident.

How much does workmen compensation insurance cost for a construction project?

The premium typically ranges from 0.5% to 2% of the total labor wage bill, depending on the risk level of the work being performed.

Can self-build homeowners get insurance for their workers?

Yes, individual homeowners can and should buy a Workmen Compensation policy to protect themselves from legal liability if a laborer is injured while working on their home.

How to register construction workers under BOCW Welfare Board?

Registration can be done through the state labor department’s portal by providing worker details, age proof, and a certificate of 90 days of work in a year.

How to include worker insurance cost in BOQ?

Estimators should calculate the insurance premium as a percentage of the labor component or the total project cost and include it as a specific line item under “Compliance & Insurance.”

Suggestions: