Imagine you have just finished building your dream home in Meerut, Uttar Pradesh. You spent months meticulously selecting the best PSC cement for the foundation and premium vitrified tiles for the flooring. However, just six months later, an unprecedented monsoon leads to severe flooding and soil subsidence, causing massive structural cracks in your walls and compromising the foundation. Without the right financial shield, the repair costs could run into lakhs, wiping out your savings. This is where structure on the property insurance becomes your most vital asset.

In the Indian real estate market, there is often significant confusion regarding what is actually covered when you buy “home insurance.” Many homeowners mistakenly believe that a basic policy covers everything from the bricks to the bread toaster. To be precise, structure on the property insurance (also known as building structure insurance or dwelling coverage) protects the physical structure of the building on your land—including the walls, roof, foundation, floors, and permanent fixtures. It ensures that the “shell” of your investment is protected against unpredictable perils.

Understanding this specific type of coverage is crucial for new home construction, accurate construction cost estimation, and long-term financial stability. Whether you are an individual builder in Delhi-NCR or a developer in a growing tier-2 city like Meerut, knowing how to value and protect the building structure is the difference between a secure project and a financial disaster. This comprehensive guide will walk you through everything you need to know about protecting your property structure in 2026.

For a broader understanding of the Indian insurance ecosystem, you may explore what is home insurance in India. This will help you see how structure coverage fits into the overall home protection strategy offered by insurers today.

What Exactly is Structure on the Property Insurance?

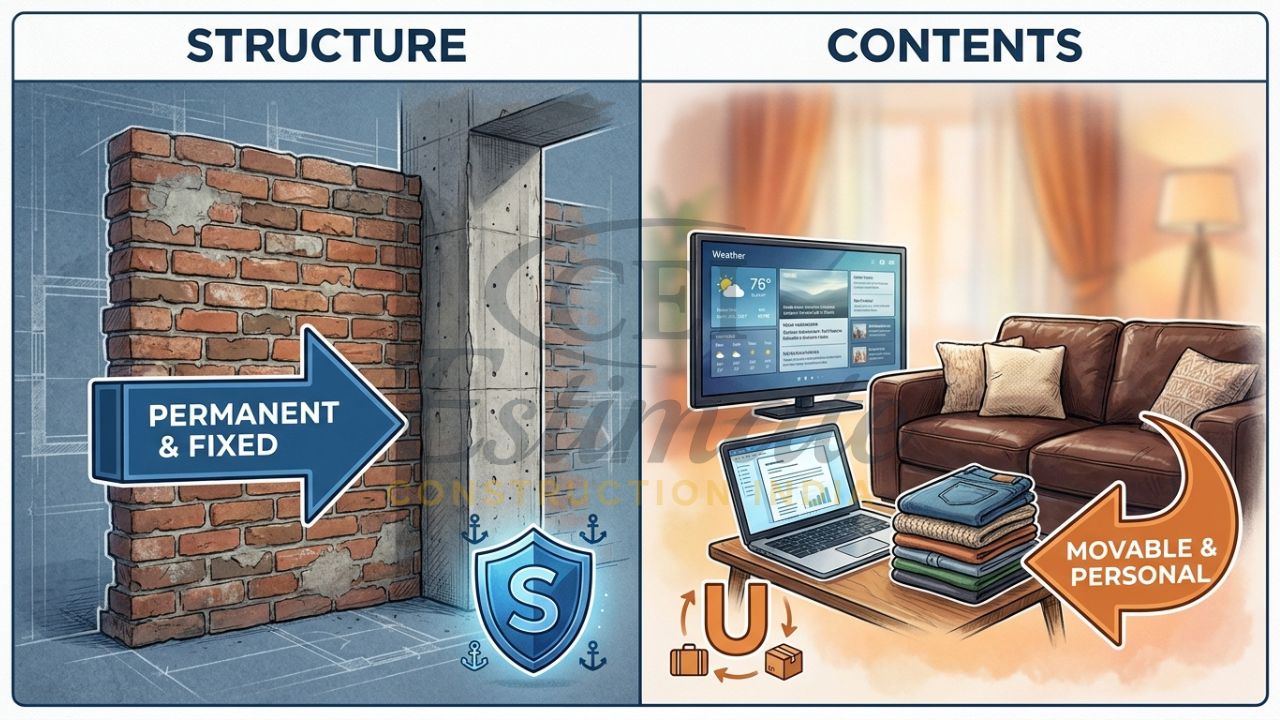

When we talk about structure on the property insurance, we are referring strictly to the immovable and fixed components of your property. Unlike “contents insurance,” which looks at what is inside the house, structure insurance focuses on the construction itself. If you were to turn your house upside down and shake it, everything that stays attached is generally considered part of the “structure.”

This insurance covers the following essential components:

- The Foundation and Plinth: The very base of your building, which is often the most expensive to repair.

- Walls and Roofs: All load-bearing and non-load-bearing walls, including the external facade and the roofing system.

- Floors and Ceilings: Permanent flooring material and the structural ceiling.

- Permanent Fixtures: This includes built-in wardrobes, kitchen cabinets, bathroom fittings, and even the electrical wiring and plumbing systems integrated into the walls.

- Exterior Features: Boundary walls, compound gates, and fences are typically included under the property structure umbrella.

It is important to clarify that this does not cover movable items. If your expensive LED TV is damaged, structure insurance won’t help; however, if the wall it is mounted on collapses due to an earthquake, that is a structure claim. In the Indian market, you might hear this referred to as home building insurance, dwelling insurance, or property structure insurance. Regardless of the name, the core intent remains the protection of your physical real estate asset.

If you want a detailed breakdown of protections, read our guide on what is covered by building insurance in India. The standard policy typically includes fire, natural calamities, and impact damage, ensuring your property’s shell is financially protected against major risks.

Structure on the Property Insurance vs Home Contents Insurance – Key Differences

In the Indian context, homeowners often find themselves choosing between these two or opting for a comprehensive package. To help you decide, here is a detailed comparison.

| Feature | Structure on the Property Insurance | Home Contents Insurance |

|---|---|---|

| Primary Focus | The physical building and fixed elements. | Personal belongings and movable items. |

| What is Covered? | Foundations, walls, roofs, plumbing, tiles. | Furniture, electronics, jewelry, appliances. |

| Who Should Buy? | Primarily the Property Owner. | Both Owners and Tenants. |

| Sum Insured Basis | Reinstatement Value (Cost to rebuild). | Market Value or Reinstatement Value. |

| Example Scenario | Wall cracks due to an earthquake. | A laptop stolen during a house break-in. |

| Policy Duration | Long-term options (up to 10-30 years). | Usually renewed annually. |

Most individual home builders in cities like Noida or Meerut prioritize insurance for building structure on property because the construction cost represents 70-80% of their total investment. Tenants, on the other hand, should only care about contents insurance. Many modern policies in 2026, such as those following the Bharat Griha Raksha framework, allow you to bundle both, but the premium for the structure is always calculated separately based on construction rates.

What Does Structure on the Property Insurance Cover in India?

In 2026, the standard for structure coverage in India is defined by the Bharat Griha Raksha (BGR) policy, a mandatory standard set by the IRDAI. This policy offers a robust “all-risk” feel for homeowners. When you secure building structure insurance, you are typically covered against the following “perils”:

- Fire and Explosions: Including lightning strikes and accidental fire.

- Natural Calamities: This is vital for India. It covers floods, storms, cyclones, typhoons, and earthquakes. For those in seismic zones like Delhi-NCR or flood-prone areas in Uttar Pradesh, this is non-negotiable.

- Landslides and Subsidence: Coverage if the ground beneath your home moves or sinks.

- Man-made Perils: Riots, strikes, and malicious acts that result in physical damage to the building.

- Impact Damage: If a vehicle crashes into your boundary wall or a falling tree damages your roof.

- Plumbing Disasters: Bursting or overflowing of water tanks, apparatus, and pipes.

- Theft: While usually associated with contents, structure insurance covers damage to the building caused during an attempted break-in (e.g., a broken door frame or smashed window).

A significant benefit of the Bharat Griha Raksha structure cover is that it automatically includes “additional structures.” This means your garage, compound wall, boundary wall, and even small outhouses or servant quarters on the same plot are covered under the same sum insured, provided they were factored into the initial valuation.

Common Exclusions – What is NOT Covered

While property structure insurance is comprehensive, it is not a “maintenance contract.” You must understand what the insurer will reject to avoid surprises during a claim.

- Wear and Tear: Gradual deterioration, such as paint peeling or minor dampness due to age, is not covered.

- Willful Negligence: If you intentionally damage the building or ignore major structural flaws, the claim will be denied.

- War and Nuclear Risks: Standard across almost all global insurance policies.

- Pre-existing Damage: Any cracks or issues present before you bought the policy.

- Illegal Construction: If you have built extra floors without municipal approval or violated local bylaws, the insurer may void the policy.

- Vacant Properties: Some policies exclude coverage if the house is left unoccupied for more than 30 or 60 consecutive days without prior notice.

Always read the “fine print” in your policy wording. In 2026, many Indian insurers are becoming stricter about “maintenance-related” water seepage vs. “burst pipe” damage.

Is Structure on the Property Insurance Mandatory?

Legally, the Government of India does not mandate that every homeowner must have structure on the property insurance. However, in practice, it often becomes mandatory in two scenarios:

- Home Loans: If you are taking a loan from banks like SBI, HDFC, or ICICI to build or buy a house, they will insist on a building insurance policy. Since the house is the collateral, the bank wants to ensure its value is protected against fire or natural disasters.

- RERA Projects: Under the Real Estate (Regulation and Development) Act, developers are often required to provide insurance for the project during the construction and maintenance phases.

Even if you don’t have a loan, voluntary purchase is highly recommended. With the increasing frequency of extreme weather events in North India—from Delhi’s seismic tremors to UP’s heavy monsoons—the small cost of a premium is a tiny price to pay for the security of your biggest asset.

How Much Does Structure on the Property Insurance Cost in India?

The premium for home structure insurance is not based on the market value of your property (which includes land price). Instead, it is based on the Reconstruction Cost.

- Reinstatement Value Method: This calculates how much it would cost to rebuild your house from scratch at current 2026 labor and material rates if it were totally destroyed.

- Premium Ranges: In 2026, the annual premium generally ranges from 0.15% to 0.50% of the sum insured. For a house with a reconstruction value of ₹50 Lakhs, the annual premium could be as low as ₹2,500 to ₹7,500.

- Calculation Factors:

- Location: Rates are higher in high-risk flood or seismic zones.

- Construction Type: An RCC (Reinforced Cement Concrete) frame building is viewed more favorably than a load-bearing brick structure.

- Tenure: Buying a 10-year or 15-year policy often comes with significant discounts compared to annual renewals.

For accurate structure on the property insurance India planning, you must link your insurance sum insured to a professional Bill of Quantities (BOQ). If your construction estimator projects a cost of ₹3,000 per sq. ft., your insurance should reflect that same value to ensure you aren’t “under-insured.”

Step-by-Step Guide to Buying Structure on the Property Insurance

Buying insurance in India has become significantly easier with digital platforms. Follow these steps to ensure you get the right coverage:

- Calculate the Area: Determine the total built-up area of your home in square feet.

- Estimate Rebuild Cost: Multiply the area by the current construction rate in your city (e.g., Meerut might be ₹2,200/sq. ft., while South Delhi might be ₹3,500/sq. ft.).

- Compare Quotes: Visit sites like PolicyBazaar or the direct portals of HDFC Ergo, ICICI Lombard, or SBI General to compare the Bharat Griha Raksha plans.

- Choose Add-ons: Consider “Escalation” (which increases the sum insured automatically as inflation rises) and “Debris Removal” coverage.

- Documentation: Keep your property tax receipts, sale deed, and the completion certificate (if available) ready. Most insurers in 2026 do not require a physical inspection for standard residential structures.

Claims Process and Tips to Avoid Rejection

If disaster strikes, you must act fast. The typical claims process for structure on the property insurance involves:

- Immediate Intimation: Inform the insurer within 24–48 hours.

- Surveyor Visit: An insurance surveyor will visit to assess the physical damage. Do not start repairs until they give the “okay.”

- Documentation: Provide the claim form, estimated repair quotes from a contractor, and photos/videos of the damage.

- Avoid Mistakes: Never hide the cause of damage. If the damage was caused by a leaking old pipe you ignored, don’t claim it as a “sudden burst.” Honesty ensures faster settlements.

Why Construction Estimators and Home Builders Must Include It?

If you are a contractor or a construction estimator, you should never overlook the cost of insurance in your project budgets. Factoring structure on the property insurance into the BOQ (Bill of Quantities) serves two purposes:

- Risk Mitigation: It protects the project during the handover phase.

- Professionalism: Providing a client with an estimate that includes the cost of protecting their new asset demonstrates a high level of expertise and care.

Under-estimating the “protection cost” of a building often leads to disputes when unforeseen damage occurs during the tail-end of a project. Including a small line item for insurance premiums ensures the developer and the homeowner are on the same page regarding risk.

As a builder or estimator, it is equally important to be aware of types of construction insurance in India. From structure coverage to contractor-specific policies, understanding the full spectrum helps you offer comprehensive risk management solutions to your clients.

Beyond property protection, responsible contractors also secure insurance for construction workers in India. This covers injuries, accidents, and liabilities during the building phase, making your project safer and more professional. Contractors and developers can further strengthen their risk management by exploring types of insurance for contractors in India. These policies complement home structure insurance and help safeguard both the project and the business.

Conclusion

Your home is more than just a place to live; it is a significant financial milestone. Understanding what is structure on the property insurance is the first step toward safeguarding that milestone against the unpredictable nature of the world. By focusing on the “reinstatement value” rather than the market price, and ensuring you have coverage for natural calamities like floods and earthquakes, you can sleep peacefully knowing your “shell” is secure.

Whether you are building a G+4 apartment in Meerut or a luxury villa in Delhi, don’t leave your structure to chance. Secure a robust policy today. For those who need help determining the exact reconstruction value of their property, contact Construction Estimator India for professional construction cost estimation and BOQ services that include integrated insurance premium analysis.

FAQ Section

What is structure on the property insurance?

It is a type of insurance that covers the physical components of a building—walls, foundation, roof, and fixed installations—against damage from fire, natural disasters, and other insured perils.

What is the difference between structure on the property insurance and contents insurance?

Structure insurance covers the permanent building and its fixed attachments (like pipes and floors), while contents insurance covers movable items inside the home (like furniture, clothes, and electronics).

Does structure on the property insurance cover earthquake and flood?

Yes, under the standard Bharat Griha Raksha framework in India, natural calamities including earthquakes, floods, and storms are covered.

How is the sum insured calculated for structure insurance?

It is calculated using the “Reinstatement Value” method, which is the total built-up area multiplied by the current cost of construction per square foot in your specific city.

Is structure on the property insurance mandatory in India?

It is not legally mandatory for all homeowners, but it is almost always required by banks and financial institutions if you have an active home loan on the property.

Can I buy insurance only for the structure on my property?

Yes, you can opt for a standalone building structure policy without including contents, although many homeowners find it more cost-effective to bundle them.

What is Bharat Griha Raksha and does it cover structure?

Bharat Griha Raksha is the standard home insurance policy introduced by IRDAI in 2021. It provides comprehensive coverage for the home building (structure) and optionally for home contents.

How much does structure on the property insurance cost in 2026?

Premiums are very affordable, typically ranging from 0.15% to 0.50% of the total reconstruction cost. For a ₹50 Lakh home, the annual premium is usually between ₹2,500 and ₹7,500.

What are the common exclusions in structure insurance?

Common exclusions include normal wear and tear, damage due to lack of maintenance, willful destruction, war, and illegal structural modifications.

Does it cover my boundary walls and garage?

Yes, standard policies in 2026 generally include boundary walls, compound gates, garages, and other permanent outhouses within the same premises.