Imagine you are a contractor in Meerut, Uttar Pradesh, preparing a detailed quotation for a new ₹50 lakh residential villa. As you finalize the material costs and labor schedules, a critical question arises: how much is insurance for construction? If you treat insurance as a negligible “lump sum” guess or, worse, ignore it entirely, you are not just risking an under-bid project; you are leaving yourself exposed to catastrophic financial losses from monsoon floods, theft, or site accidents. In the 2026 Indian construction boom, where material prices for steel and cement are volatile and climate risks in the Delhi-NCR region have escalated, understanding the precise cost of insurance is no longer optional—it is a fundamental pillar of professional risk management.

Generally, the total construction insurance cost India 2026 can range from 0.5% to over 2% of the total project value, depending on the complexity and the specific covers required. This cost isn’t a single flat fee but a combination of specialized policies like Contractors’ All Risk (CAR), Workmen Compensation Insurance (WCI), and Plant & Machinery (CPM) insurance. For construction estimators and small builders in North India, getting these figures right in your Bill of Quantities (BOQ) ensures that your profit margins remain protected regardless of what happens on-site. In this comprehensive guide, we will break down the realistic 2026 premium ranges, the factors that drive these prices, and provide a step-by-step method to calculate insurance costs accurately for any project.

For a complete overview of all available policies, read our detailed guide on types of construction insurance in India.

Factors That Determine How Much Insurance Costs for Construction Projects?

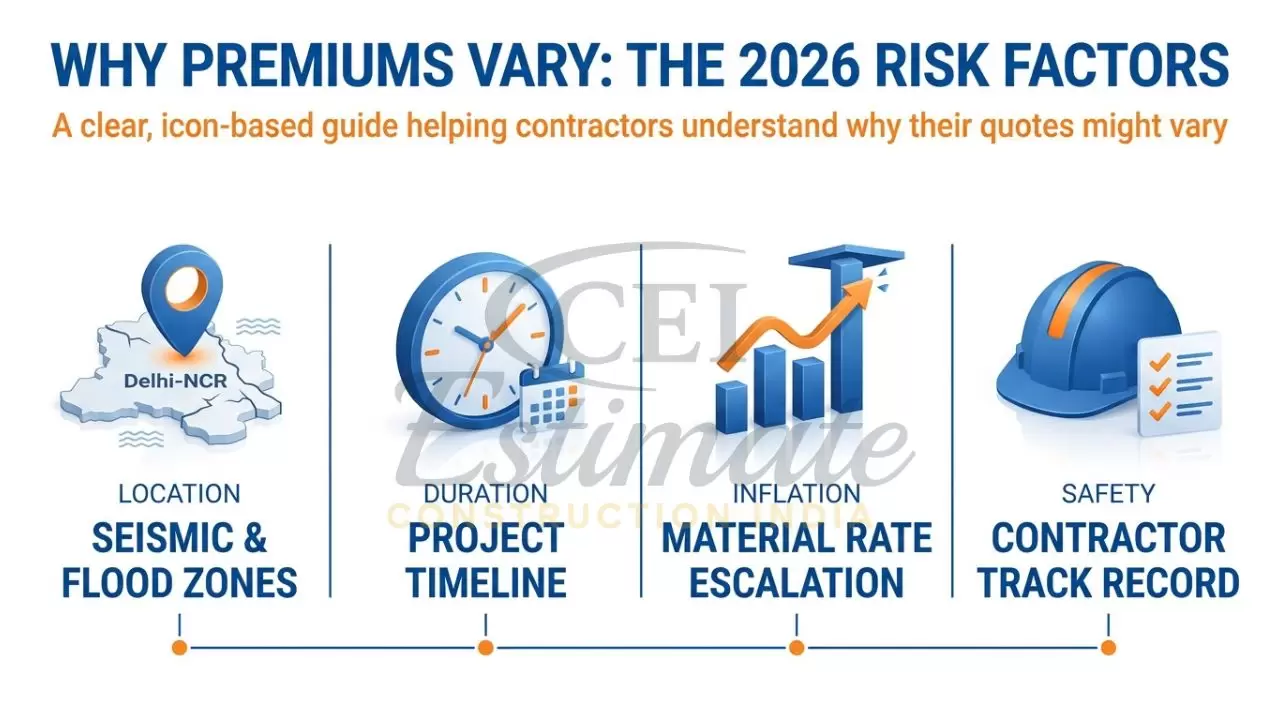

Determining how much does construction insurance cost in India depends on several variables that help insurers assess the level of risk your project carries. No two construction sites are identical, and therefore, premiums are tailored to the specific environment of the build.

- Project Value (Sum Insured): The most significant factor is the total contract value. This includes the cost of materials, labor, professional fees, and temporary works. Insuring for the “reinstatement value”—the actual cost to rebuild in 2026—is vital to avoid under-insurance penalties.

- Project Duration: A 12-month residential build in Meerut will naturally have a lower premium than a 36-month high-rise project in Noida. Longer durations mean extended exposure to weather events and theft.

- Location Risks: Geography plays a massive role. Projects located in seismic Zone IV or V (like parts of Delhi-NCR) or flood-prone areas of Uttar Pradesh will attract higher premiums due to the increased probability of natural calamities.

- Type of Construction: RCC frame structures are generally viewed as lower risk compared to structures involving significant timber work or deep basement excavations that threaten neighboring properties.

- Contractor Experience: Your track record as a builder matters. If you have a history of zero claims and a reputation for strict safety protocols, you can often negotiate more competitive rates.

For detailed protection during the active building phase, explore our guide on insurance for building under construction in India.

Cost of Contractors’ All Risk (CAR) Insurance

In the Indian residential and civil market, CAR insurance premium cost is the most substantial part of your insurance budget. It serves as a comprehensive “all-risk” shield covering physical damage to the works, materials on-site, and third-party liability.

For most projects in 2026, the basic premium for CAR insurance typically ranges from 0.5% to 1.5% of the total project value. However, for large-scale infrastructure or long-term projects, the rate might be structured as an initial fee followed by smaller monthly payments ranging from 0.02% to 0.05%. For a standard ₹1 crore residential project in North India, your premium would likely fall between ₹50,000 and ₹1,50,000 depending on the selected add-ons like debris removal or escalation clauses.

For small and growing businesses, check our recommendations on best insurance for small construction business in India.

CAR Insurance Cost Breakdown by Project Size (2026 Estimates)

| Project Value | Estimated Premium Range (Basic) | Typical Add-ons Included |

|---|---|---|

| ₹10 Lakh (Renovation) | ₹5,000 – ₹12,000 | Third-Party Liability, Small Tools |

| ₹50 Lakh (House Build) | ₹25,000 – ₹60,000 | Debris Removal, Monsoon Cover |

| ₹1 Crore (Villa/Small Comm.) | ₹50,000 – ₹1,30,000 | Escalation Clause, Maintenance Period |

| ₹5 Crore (Mid-size Housing) | ₹2,50,000 – ₹6,50,000 | Surrounding Property, Architect Fees |

The “Escalation Clause” is particularly important in 2026. Given the inflation in material rates, adding a 10–15% escalation rider ensures that if a fire destroys your site in the final months, the payout covers the current replacement cost of materials rather than the rates from the project’s start.

Cost of Workmen Compensation Insurance for Construction

As a contractor or builder, workmen compensation insurance cost for construction is a non-negotiable legal requirement under the Employees’ Compensation Act 1923 and the BOCW Act. This policy protects you from the massive legal liabilities that arise if a worker suffers an injury, disability, or death on your site.

The premium is primarily based on your total wage bill rather than the project value. In 2026, the premium for WCI typically ranges from 0.5% to 2% of the total labor cost. For a site in Noida with a ₹50 lakh annual labor payroll, the premium would range between ₹25,000 and ₹1,00,000.

It is also mandatory to factor in the labor welfare cess (BOCW cess), which in states like Uttar Pradesh and Haryana is usually 1% to 2% of the total project cost. While not a private insurance premium, it is a statutory cost that funds state-level insurance and welfare benefits for registered workers. For budget-conscious independent contractors, linking workers to government schemes like PMSBY (at just ₹20 per year) can provide an additional layer of low-cost accident protection.

To understand worker-specific protections and compliance, refer to our complete guide on insurance for construction workers in India.

Other Construction Insurance Costs

While CAR and WCI are the essentials, a professional cost of insurance for building construction must often include additional protections depending on the project’s nature.

- Contractors Plant & Machinery (CPM): If you use high-value equipment like tower cranes or JCBs, CPM insurance is vital. This typically costs 0.5% to 1.5% of the market value of the equipment. For a ₹50 lakh excavator, the annual premium would be approximately ₹25,000 to ₹75,000.

- Erection All Risk (EAR): For projects focused on machinery installation (like HVAC systems or industrial plants), EAR is used instead of CAR. Premiums range from 0.6% to 2.0% of the machinery value.

- Third-Party Liability (Standalone): While included in CAR, some large developers opt for standalone Commercial General Liability (CGL) for much higher limits. This is often priced on a case-by-case basis but is highly affordable for the protection it offers.

- Completed Building Insurance: Once construction is over, the cost drops significantly. A “Bharat Griha Raksha” policy for a completed home (up to ₹50 lakh value) often costs as little as ₹2,000 to ₹5,000 per year, which is a fraction of the cost of insuring the same building while it was under construction.

For larger or commercial-scale projects, specific requirements apply. Read our guide on commercial construction insurance requirements in India.

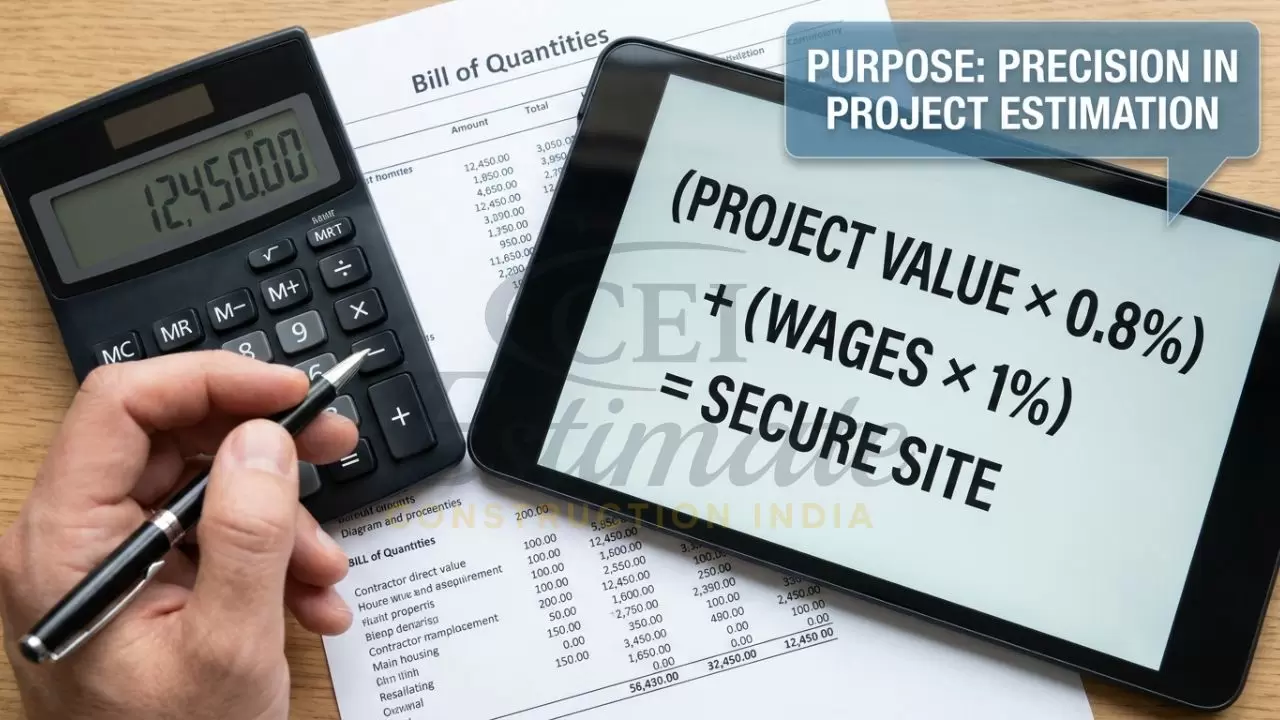

How to Calculate Construction Insurance Cost – Step-by-Step?

To determine how to calculate construction insurance premium for your next BOQ, you can follow this practical formula used by expert Indian estimators.

Formula:

(Project Value × CAR Base Rate) + (Annual Wage Bill × WCI Rate) + (Add-on Costs) + 18% GST = Total Insurance Cost

Example Calculation (₹40 Lakh Residential House in Meerut):

- Step 1: Define Sum Insured. Total project cost (excluding land) = ₹40,00,000.

- Step 2: Apply CAR Rate. Using a 2026 average rate of 0.8% for a 12-month project: ₹40,00,000 × 0.008 = ₹32,000.

- Step 3: Calculate WCI. Estimated labor cost (approx. 30% of project) = ₹12,00,000. At a 1% WCI rate: ₹12,00,000 × 0.01 = ₹12,000.

- Step 4: Add-ons & GST. Add ₹5,000 for Debris Removal and Escalation. Subtotal = ₹49,000. Plus 18% GST (₹8,820).

- Total Estimated Insurance: ₹57,820.

In this scenario, the total insurance cost represents approximately 1.45% of the project value, providing full protection for the structure, materials, and workers.

When working with multiple parties, proper arrangements are essential. Learn more in our guide on how to get insurance for subcontractors in India.

Real Examples – How Much Insurance Costs for Different Projects in India

To give you a clearer picture of how much is insurance for construction in various real-world scenarios, consider these three case studies based on 2026 market data.

- Case 1: Small Independent House (₹20 Lakh Construction)

- Location: Tier-3 city in Uttar Pradesh.

- Insurance Strategy: Basic CAR + WCI for 10 workers.

- Total Insurance in BOQ: ₹18,000 – ₹25,000.

- Case 2: Premium Residential Villa (₹1.5 Crore Construction)

- Location: Meerut / NCR Region (Seismic Zone IV).

- Insurance Strategy: Comprehensive CAR with Escalation Clause + CPM for on-site mixer/lift + WCI.

- Total Insurance in BOQ: ₹1,10,000 – ₹1,60,000.

- Case 3: Commercial Basement & 3-Story Plaza (₹5 Crore Contract)

- Location: Noida Sector 150.

- Insurance Strategy: CAR with Surrounding Property Cover + EAR for HVAC + CGL for Public Liability + Full WCI.

- Total Insurance in BOQ: ₹4,50,000 – ₹7,00,000.

Tips to Reduce Construction Insurance Costs Without Compromising Coverage

You can manage your construction insurance price per crore by being proactive about risk management.

- Implement Site Safety: Insurers often provide discounts if you have 24/7 security, gated access, and a clear safety policy for laborers using PPE.

- Choose the Right Sum Insured: Don’t insure the land value—only the reconstruction cost of the building. Over-insuring is a waste of premium.

- Bundle Policies: Buying your CAR, WCI, and CPM from a single insurer like ICICI Lombard or HDFC Ergo can often result in a 10–15% “package discount”.

- Maintain a Good Claims History: Much like a No-Claims Bonus for car insurance, a history of safe, accident-free sites will help you secure the best rates in 2026.

How to Include Insurance Costs Accurately in Your BOQ and Estimates?

For a professional construction estimator, insurance should never be hidden within “miscellaneous” or “contingency” funds. It must be a dedicated line item in your BOQ. By listing insurance separately, you demonstrate transparency to your client and ensure that these “soft costs” don’t erode your 10–15% profit margin if an accident occurs.

Always calculate the premium based on actual current quotes rather than historical data. If you are an independent contractor, explaining to your client that this 1% fee protects their entire investment usually makes it a very easy cost to justify. Including the maintenance period (usually 12 months post-handover) in your CAR policy is another expert move that protects your reputation against structural defects discovered after the client moves in.

Conclusion

Understanding how much is insurance for construction is the difference between building a sustainable business and one that is a single storm away from bankruptcy. In 2026, with an average cost ranging from 0.5% to 2% of your project value, insurance remains one of the most affordable ways to protect 100% of your capital investment. Whether you are a small builder in Meerut or a developer in Delhi-NCR, accurate insurance costing in your BOQ is your greatest competitive advantage.

Don’t leave your project’s financial foundation to chance. At Construction Estimator India, we specialize in providing professional BOQs and construction cost estimation services that accurately factor in all necessary insurance premiums based on 2026 market rates. Contact us today to ensure your next build is as safe as it is profitable.

FAQ Section

How much is insurance for construction in India in 2026?

On average, expect to pay between 0.5% and 2% of the total project value. For a typical ₹50 lakh home, this amounts to roughly ₹35,000 to ₹75,000 including taxes and basic labor cover.

What is the average cost of CAR insurance for a residential project?

The CAR premium usually falls between 0.5% and 1.5% of the contract value. Factors like the project’s location in a seismic zone and the inclusion of debris removal will influence the final rate.

How is construction insurance premium calculated?

It is calculated by applying a percentage (the rate) to the total sum insured (project value), adding premiums for specific labor counts (WCI), and then adding 18% GST.

How much does Workmen Compensation insurance cost for construction workers?

WCI typically costs between 0.5% and 2% of your total labor wage bill. For a site with a ₹10 lakh labor cost, the premium would be around ₹5,000 to ₹20,000.

Is construction insurance mandatory?

Workmen Compensation is legally mandatory under the BOCW Act. While CAR insurance isn’t always legally required for private builds, it is almost always mandated by banks for construction-linked loans.

How much insurance cost should I add to my BOQ?

A safe estimate is to add 1% to 1.5% of the total project value as a separate line item for “Insurance and Compliance” to cover CAR, WCI, and basic site risks.

Does home insurance cover under-construction buildings?

No. Standard home insurance like “Bharat Griha Raksha” only covers completed, occupied dwellings. You must have a Builders Risk or CAR policy during the construction phase.

How can independent contractors reduce insurance costs?

By implementing strict site safety, bundling policies with one insurer, and ensuring the sum insured accurately reflects the reconstruction cost without the land value.

Where can I get accurate quotes for construction insurance in India?

You can use digital aggregators like Policybazaar or contact major insurers like New India Assurance, ICICI Lombard, or HDFC Ergo directly for project-specific quotes.

Related Articles: