Imagine you are a contractor in Meerut or a bustling hub in Uttar Pradesh, meticulously preparing your next big bid for a premium residential project in the Delhi-NCR region. You’ve calculated material costs, labor hours, and logistics, but one lingering question remains: “What is the best insurance for contractors?” This isn’t just a matter of checking a box for compliance; it is a critical financial decision. In the volatile landscape of 2026, one unseasonable monsoon storm, a site accident, or a localized theft of high-value TMT bars can erase your entire profit margin and leave you personally liable for millions in damages.

There is no single, magic policy that serves as the “best” for every single person in the industry. The ideal choice depends heavily on your project type, the size of your operation, and the specific risks associated with your site. However, for the vast majority of professionals in India, Contractors’ All Risk (CAR) Insurance is widely regarded as the most essential and comprehensive policy. It serves as the cornerstone of risk management, protecting your hard work from the moment materials are unloaded until the final handover.

With the 2026 infrastructure and housing boom reaching peak levels in North India, site hazards like natural calamities, theft, and worker accidents are statistically more probable. This guide will help you navigate these risks. We will compare the major policies available, explain why CAR often tops the list of recommendations, and provide a realistic breakdown of costs. More importantly, as an estimator, you will learn how to accurately factor these premiums into your Bill of Quantities (BOQ) to ensure your projects remain both protected and profitable.

Why “Best” Insurance Depends on Your Specific Needs?

When searching for the best insurance for contractors in India 2026, you must first acknowledge that your risk profile is unique. A small independent contractor specializing in interior renovations in Meerut faces different threats than a general contractor managing a ₹100-crore multi-story housing society in Noida.

Several factors dictate what will be the most effective coverage for you:

- Project Size and Complexity: A simple boundary wall construction requires far less coverage than a deep-foundation high-rise project. Larger projects often have stricter bank-mandated requirements for comprehensive policies.

- Geographical Risks: If you are building in the Delhi-NCR region, you are in a high seismic zone (Zone IV/V). If your site is in a flood-prone area of Uttar Pradesh, your “best” policy must prioritize natural peril add-ons.

- Contractual Mandates: Many government tenders and private developers specify exactly which insurance policies you must hold. Failing to meet these requirements can disqualify your bid or lead to a breach of contract.

- Budget and Firm Maturity: Independent contractors often seek a balance between affordability and essential coverage, whereas large construction companies need complex enterprise-level risk portfolios, including Directors and Officers (D&O) liability.

Relying on a single, basic policy can leave dangerous gaps in your protection. A “best” strategy usually involves a layered approach where different policies cover different facets of the business—structural, human, and mechanical.

For growing or smaller operations, explore tailored and affordable solutions in our article on best insurance for small construction business in India.

Why Contractors’ All Risk (CAR) Insurance is Often the Best Choice?

In the professional opinion of seasoned estimators, the best CAR insurance for contractors is the gold standard because of its “all-risk” nature. Unlike a “named peril” policy that only covers what is explicitly listed, a CAR policy covers everything except what is specifically excluded. This makes it the most comprehensive shield for your civil works.

For accurate project costing of this vital policy, check our breakdown on how much does builders risk insurance cost in India.

Comprehensive Protection for the Entire Project

A CAR policy protects the “physical anatomy” of your construction project. This includes the permanent structure (walls, foundation, slabs), raw materials (cement, steel, electrical fittings) stored on-site, and temporary works such as scaffolding and site offices. Crucially, the coverage begins as soon as materials are unloaded at the site and can extend through a “maintenance period,” protecting you against defects discovered even after the building is completed.

The Critical Third-Party Liability Shield

One of the primary reasons CAR is considered the best insurance for contractors is its inclusion of Third-Party Liability (TPL). Construction sites are dynamic and dangerous. If a falling brick damages a neighbor’s car in a congested Meerut colony, or if an excavation causes structural cracks in an adjacent building, the TPL section of your CAR policy handles the legal defense and the compensation payouts.

Resilience Against Indian Realities

In North India, we face specific risks that CAR policies are uniquely equipped to handle:

- Monsoon and Floods: Heavy rains can collapse shuttering or ruin thousands of bags of cement.

- Theft and Burglary: Site theft is a massive hidden cost. CAR policies cover the loss of materials like copper wiring and sanitary fittings.

- Natural Calamities: With seismic tremors frequently felt in Delhi-NCR, having a policy that covers earthquake damage to the work-in-progress is non-negotiable.

When comparing Contractors All Risk insurance vs other policies like Bharat Griha Raksha, the difference is clear: Bharat Griha Raksha is for finished buildings. CAR is specifically engineered for the high-risk, unroofed, and vulnerable state of a building under construction. For any contractor managing the building phase, CAR is the undisputed winner for structural protection.

Other Strong Insurance Options for Contractors

While CAR is the foundation, a complete safety net for your business in 2026 requires looking at a few other essential covers. Often, the most robust “best” package for a contractor is a combination of CAR, WCI, and CPM.

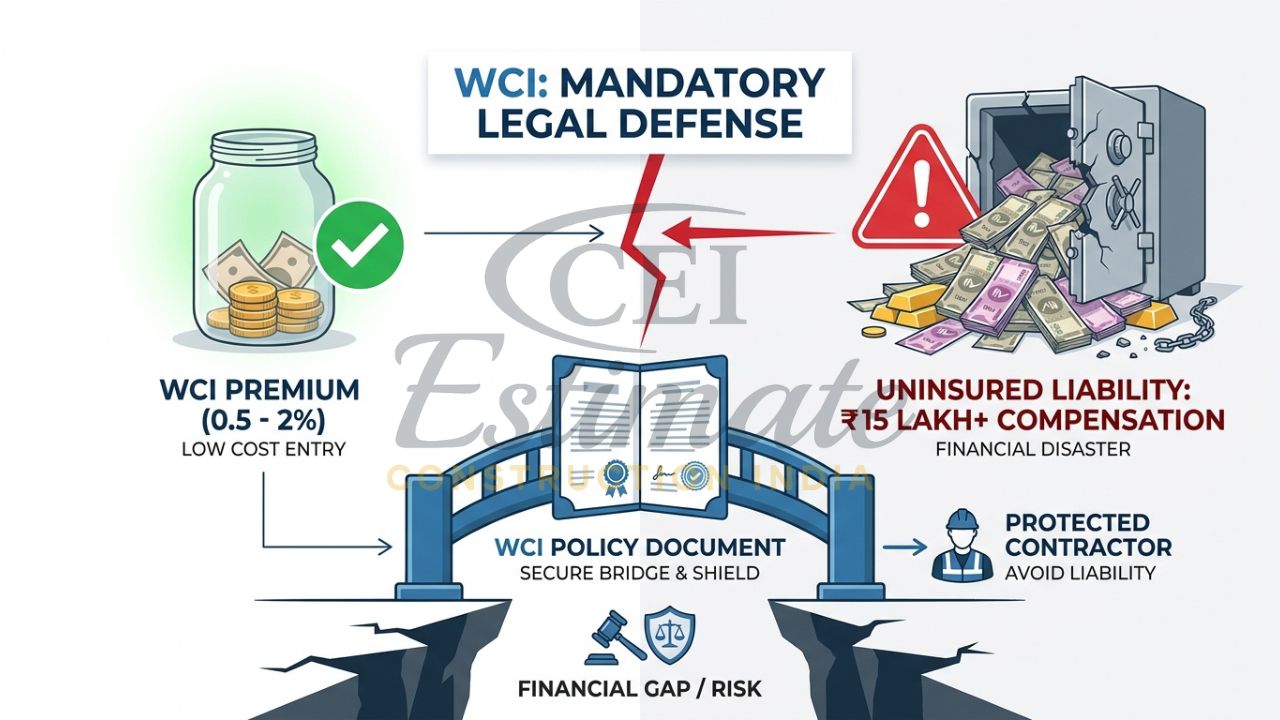

- Workmen Compensation Insurance (WCI): This is not just a recommendation; it is a legal mandate under the Employees’ Compensation Act. In 2026, the cost of labor-related legal claims is skyrocketing. WCI protects you from massive payouts if a worker suffers an injury, disability, or death on your site.

- Contractors Plant & Machinery (CPM): If you use expensive equipment like JCBs, tower cranes, or concrete mixers, you need CPM. While CAR might cover small tools, a standalone CPM policy protects high-value assets from accidental damage, breakdown, and theft, even when they are moved between different project sites.

- Erection All Risk (EAR): If your project is less about “bricks and mortar” and more about “nuts and bolts”—such as installing a centralized HVAC system or a power plant—EAR is the better choice. It focuses on the mechanical and electrical risks of installation and testing.

- Professional Indemnity (PI): If you are an independent contractor who also provides design-build services or site supervision, PI protects you against claims of professional negligence or errors in your architectural plans.

By integrating these, you create a seamless barrier. CAR protects the project, WCI protects the people, and CPM protects the equipment.

To understand worker-specific legal requirements, refer to our guide on insurance for construction workers in India. For commercial and large-scale projects, specific compliance becomes even more important. Read our guide on commercial construction insurance requirements in India. When coordinating with external teams, proper arrangements are essential. Learn more in our guide on how to get insurance for subcontractors in India.

CAR Insurance vs Other Policies – Detailed Comparison

To help you decide what constitutes the best construction insurance for small contractors versus large firms, refer to this 2026 market comparison.

| Feature | Contractors’ All Risk (CAR) | Workmen Compensation (WCI) | Plant & Machinery (CPM) |

|---|---|---|---|

| Coverage Scope | Physical works, materials, & third-party liability. | Worker death, injury, & medical expenses. | Accidental damage & theft of equipment. |

| Who it Protects | The Contractor, Owner, & the Project. | The Laborers & the Contractor (Legal Shield). | The Owner of the Machinery. |

| Sum Insured Basis | Total Project Value + Escalation. | Total Annual Wage Bill. | Replacement Value of Machine. |

| 2026 Premium Range | 0.5% – 1.5% of Contract Value. | 0.5% – 2.0% of Wage Bill. | 1.0% – 2.5% of Machine Value. |

| Best Suited For | All civil & residential builds. | All labor-intensive sites. | Infrastructure & heavy builds. |

| Why it Ranks Top | Most comprehensive “all-in-one” cover for project assets. | Non-negotiable legal requirement in India. | Vital for protecting high-capital assets. |

How to Choose the Best Insurance for Your Contracting Business?

The process of finding the best insurance for contractors in India 2026 requires a methodical approach. You shouldn’t just buy the cheapest policy; you should buy the most relevant one.

- Assess Project Risks: Is the site near a river? Is it in a high-density urban area? These factors determine which add-ons (like debris removal or surrounding property cover) you need.

- Review Contract Clauses: Don’t guess. Check your tender documents. Most clients will specify the “Limit of Indemnity” required for third-party liability.

- Calculate Reinstatement Value: Ensure your sum insured reflects what it would cost to rebuild today, not what it cost three years ago. Include an escalation clause (typically 10-15%) to account for rising steel and cement prices.

- Compare Reliable Insurers: Look for providers with high claim settlement ratios. Companies like HDFC Ergo, ICICI Lombard, New India Assurance, and SBI General are popular choices in North India for their local claim processing capabilities.

- Factor in Subcontractors: If you hire specialists, ensure your policy covers their workers, or mandate that they carry their own insurance to avoid leaving you with “secondary liability.”

Realistic Costs and How to Include Insurance in Your BOQ?

Understanding how to choose insurance for contractors India is only half the battle; the other half is making sure you don’t lose money on it. In 2026, a standard CAR policy for a residential project in Meerut typically costs between 0.5% and 1.5% of the project value. WCI usually costs about 0.5% to 2% of your labor wage bill.

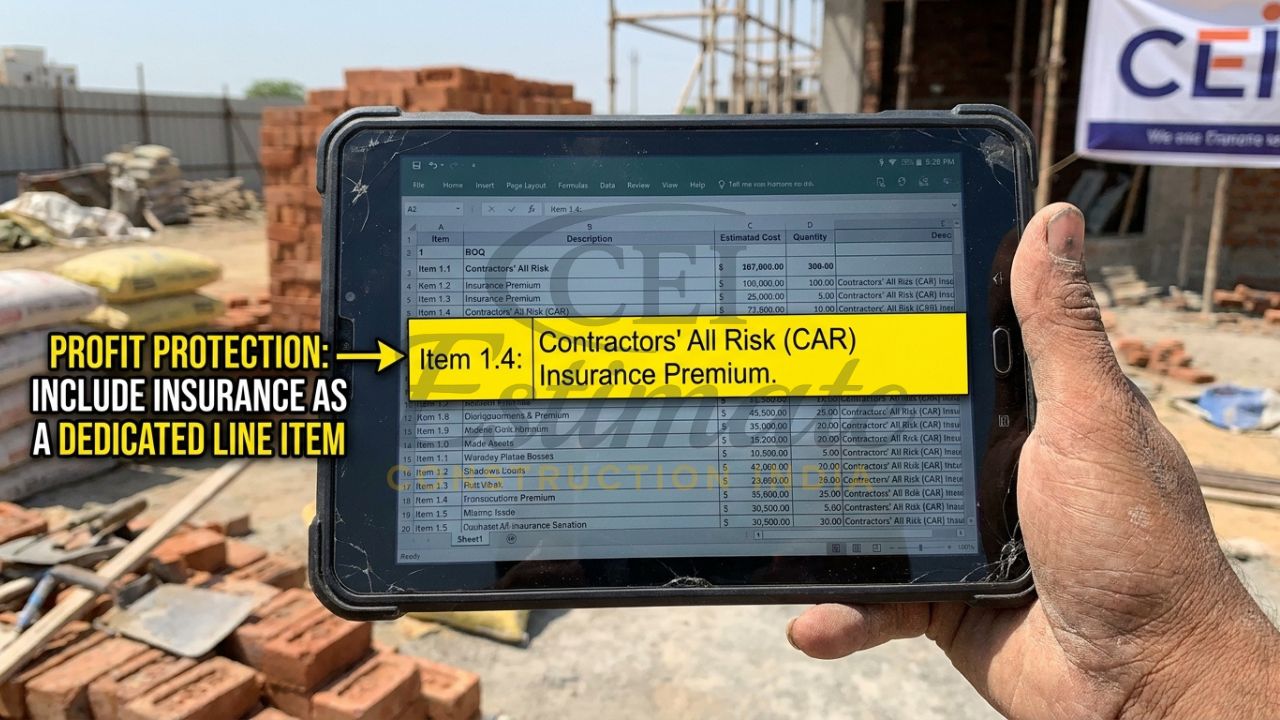

For a professional construction estimator, insurance should never be a hidden overhead. It must be a distinct line item in your Bill of Quantities (BOQ). Categorize it under “General Requirements” or “Preliminaries.” By itemizing these costs, you demonstrate professionalism to the client and ensure that your profit margin is protected. If you forget to add a ₹50,000 premium to a ₹1-crore project, that’s ₹50,000 straight out of your pocket.

For overall accurate budgeting, refer to our detailed analysis on how much is insurance for construction in India.

Step-by-Step Guide to Buying the Right Insurance

Follow these simple steps to secure your business:

- Identify Needs: List your project value, worker count, and machinery list.

- Gather Project Details: Have your site address, blueprints, and project timeline ready.

- Get Multiple Quotes: Use digital platforms or brokers to compare at least three different quotes.

- Customize with Add-ons: Ensure you have “Natural Perils” and “Burglary” included.

- Maintain Records: Keep site logs and safety records; these often lead to lower premiums during renewals.

Conclusion

Determining what is the best insurance for contractors doesn’t have a one-size-fits-all answer, but the path is clear. While Contractors’ All Risk (CAR) Insurance is the most vital and comprehensive single policy for civil work, the ultimate “best” solution is a tailored combination that accounts for your workers and your machinery. In the competitive Indian market of 2026, being “insured and assured” is your greatest competitive advantage. It allows you to bid with confidence, knowing that a single accident won’t derail your business.

Don’t leave your financial foundation to chance. At Construction Estimator India, we specialize in providing professional BOQs and construction cost estimation services that accurately factor in all necessary insurance costs based on 2026 market rates. Contact us today to ensure your next build is as safe as it is profitable.

FAQ Section

What is the best insurance for contractors in India?

For most contractors, a Contractors’ All Risk (CAR) policy is considered the best single option because it covers structural damage, material loss, and third-party liability in one package.

Is CAR Insurance the best option for all contractors?

It is the best for civil and residential builders. However, if your work is strictly mechanical or equipment-based, Erection All Risk (EAR) or Plant & Machinery (CPM) insurance might be more suitable.

What does Contractors All Risk (CAR) Insurance cover?

It covers damage caused by fire, theft, flood, earthquake, and accidents to the work-in-progress, raw materials, and temporary site structures, along with liability for third-party injuries.

How much does the best insurance for contractors cost in 2026?

For a typical project, CAR insurance premiums range from 0.5% to 1.5% of the total project value. WCI costs depend on the total wage bill and site risk category.

Do I need Workmen Compensation along with CAR?

Yes. CAR focuses on the property and third parties, while Workmen Compensation (WCI) is a legal requirement that specifically protects you from liabilities related to worker injuries or death.

What is the difference between CAR and EAR insurance?

CAR is for civil construction like houses and bridges. EAR (Erection All Risk) is for projects involving the installation and testing of machinery and electrical systems.

Can small or independent contractors afford the best insurance?

Absolutely. For a small house project worth ₹50 Lakh, a CAR policy can cost as little as ₹8,000 to ₹15,000, which is very affordable compared to the risk of a total loss.

How do I include insurance costs in my project estimates?

You should list insurance as a separate line item in your BOQ under “Preliminaries” or “Project Overheads,” usually calculated as a percentage of the total contract value.

Is CAR Insurance mandatory for contractors?

While not always legally mandatory like WCI, it is almost always required by banks for home loans and by clients for government and large private tenders.

Which insurers offer the best CAR policies in India?

Top providers include New India Assurance, ICICI Lombard, HDFC Ergo, and SBI General, known for their comprehensive coverage and reliable claim settlement history.

Related Articles: