Imagine you are a self-building homeowner in Meerut, Uttar Pradesh, meticulously planning your dream three-story residence. You have mapped out the cost of every TMT bar and every pallet of cement, but as you finalize your budget, a nagging question arises: how much does builders risk insurance cost? You realize that an unseasonal monsoon cloudburst or a localized fire could wipe out your life savings in an instant if your project isn’t protected. For independent contractors and small-scale builders in the Delhi-NCR region, getting this figure right is the difference between a profitable venture and a financial catastrophe.

Builders Risk Insurance, often referred to as insurance for building under construction or as a component of a Contractors All Risk (CAR) policy, is your most vital financial ally during the high-risk construction phase. However, its cost is not a fixed number; it varies based on geography, project complexity, and chosen safety riders. In this comprehensive 2026 guide, we provide realistic cost breakdowns for various project sizes in India, analyze the factors that drive premiums, and show you how to accurately include these costs in your Bill of Quantities (BOQ). We will also share a step-by-step guide to securing the best quotes from top Indian insurers. By the end of this article, you will have the clarity needed to protect your investment with a robust and accurately budgeted safety net.

What is Builders Risk Insurance and Why Does Its Cost Matter?

Builders Risk Insurance is a specialized product designed to protect the “work-in-progress” from the moment of groundbreaking until the final handover or the issuance of a completion certificate. In the Indian market, this is typically obtained through a Contractors All Risk (CAR) policy, which provides a comprehensive “all-risk” shield against physical damage to the structure, raw materials on-site, and even temporary works like scaffolding. It treats the construction site as a dynamic environment where risks like structural collapse, theft of expensive materials, and third-party liabilities are constant threats.

Knowing the exact how much does builders risk insurance cost is critical because insurance should never be a “lump sum” guess hidden within a contingency fund. For construction estimators and builders, accurate costing ensures that profit margins are protected and that the project remains financially viable even if a calamity strikes. Furthermore, most Indian banks and NBFCs mandate this insurance as a prerequisite for construction-linked home loans. Failing to budget for it accurately can lead to unexpected out-of-pocket expenses that erode your project’s solvency.

Factors That Affect Builders Risk Insurance Cost

Determining how much does builders risk insurance cost in 2026 requires an understanding of the specific risk variables that insurers use to calculate premiums. No two sites are identical, and your costs will reflect the unique environment of your build.

- Project Value (Sum Insured): This is the most significant driver. The sum insured must reflect the “reinstatement value”—the total cost of materials, labor, and professional fees required to rebuild from scratch.

- Construction Duration: A 12-month residential project will naturally attract a lower premium than a 36-month high-rise development, as longer durations mean extended exposure to weather events and theft.

- Project Location: Geography plays a massive role in Indian premiums. Projects in high seismic zones (Zone IV/V) like Delhi-NCR or flood-prone areas in Uttar Pradesh will see higher rates due to increased risk of natural calamities.

- Type of Construction: RCC frame structures are generally viewed as lower risk compared to structures involving significant timber work or deep basement excavations that might threaten neighboring properties.

- Contractor Experience: Builders with a proven track record of safe sites and zero previous claims can often negotiate more competitive rates with insurers.

- Safety Measures: The presence of 24/7 security, gated access, and strict adherence to safety protocols for laborers can lead to premium discounts.

| Factor | Impact on Premium | 2026 Indian Context |

|---|---|---|

| Seismic Zone (IV/V) | Increase (10-25%) | Crucial for Delhi, Noida, Meerut |

| Duration Extension | Pro-rata Increase | Common for monsoon-related delays |

| Deep Excavation | Increase (Liability) | Vital for basement projects in urban colonies |

| RCC Structure | Baseline / Decrease | Preferred construction method for lower rates |

Average Cost of Builders Risk Insurance in India 2026

In the current 2026 market, the how much does builders risk insurance cost generally falls between 0.5% and 1.5% of the total project value. This range ensures that the structure, materials, and third-party liabilities are fully covered throughout the construction lifecycle. For professional estimators, calculating the builders risk insurance price per crore is a common way to benchmark these costs, with premiums typically ranging from ₹60,000 to ₹1,20,000 per crore of construction value.

Small Residential House (₹20 Lakh – ₹50 Lakh)

For a small independent house or floor in a tier-2 city like Meerut, the premium is surprisingly affordable.

- Project Value: ₹30 Lakhs.

- Estimated Premium: ₹15,000 – ₹25,000 for a 12-month period.

- Typical Coverage: Basic CAR policy including fire, natural perils, and site theft.

Medium Residential Villa (₹50 Lakh – ₹1.5 Crore)

Medium-sized projects often require additional riders to handle increased complexity.

- Project Value: ₹1 Crore.

- Estimated Premium: ₹60,000 – ₹1,20,000.

- Typical Coverage: Comprehensive CAR with escalation clauses and third-party liability.

Larger Projects (₹2 Crore+)

For larger housing complexes or high-end villas, the cost of insurance for building under construction is often structured with more competitive baseline rates but higher costs for specific add-ons.

- Project Value: ₹5 Crores.

- Estimated Premium: ₹2,50,000 – ₹6,50,000.

- Typical Coverage: Advanced CAR including surrounding property cover, professional fees, and debris removal.

In terms of premium structure, most Indian insurers require a one-time payment for the entire project duration. However, for very large infrastructure projects, some firms may offer an initial fee followed by smaller installments.

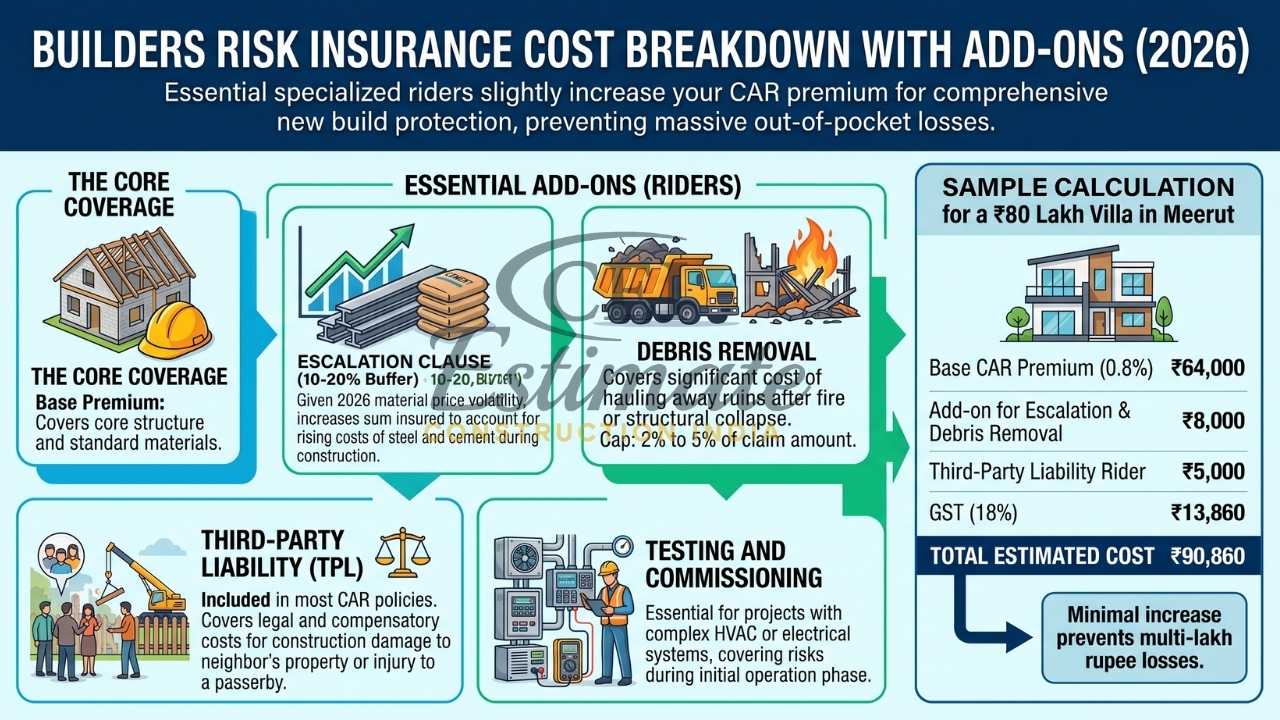

Builders Risk Insurance Cost Breakdown with Add-ons

The base premium covers the core structure and materials, but in 2026, specialized add-ons are essential for full protection. These riders will slightly increase the CAR insurance premium for new build projects, but they prevent massive out-of-pocket losses.

- Escalation Clause (10-20% Buffer): Given the volatility of material prices in 2026, this rider automatically increases the sum insured to account for rising costs of steel and cement during the build.

- Debris Removal: This covers the significant cost of hauling away ruins after a fire or structural collapse, usually capped at 2% to 5% of the claim amount.

- Third-Party Liability (TPL): Included in most CAR policies, TPL covers legal and compensatory costs if your construction activities damage a neighbor’s property or injure a passerby.

- Testing and Commissioning: Essential for projects involving complex HVAC or electrical systems, covering risks during the initial operation phase.

Sample Calculation for a ₹80 Lakh Villa in Meerut:

- Base CAR Premium (0.8%): ₹64,000.

- Add-on for Escalation & Debris Removal: ₹8,000.

- Third-Party Liability Rider: ₹5,000.

- GST (18%): ₹13,860.

- Total Estimated Cost: ₹90,860.

Builders Risk (CAR) Insurance Cost vs Other Construction Insurance

To understand how much is builders risk insurance in India, it is helpful to compare it with other mandatory or recommended policies.

- Workmen Compensation Insurance (WCI): While CAR covers the property, WCI covers the people. The cost is based on your wage bill, typically ranging from 0.5% to 2% of total labor costs. For a project with ₹20 Lakh labor costs, WCI would cost roughly ₹10,000 – ₹40,000.

- Contractors Plant & Machinery (CPM): If you use high-value equipment like cranes or mixers, CPM insurance costs about 1% to 2.5% of the equipment’s market value.

- Completed Building Insurance (Bharat Griha Raksha): Once construction ends, the cost of insurance drops significantly. A standard BGR policy for a completed ₹1 Crore home often costs as little as ₹5,000 – ₹10,000 per year, compared to the much higher construction-phase premium.

How to Reduce Builders Risk Insurance Cost Without Compromising Coverage?

Managing your builders risk insurance price per crore involves proactive risk mitigation rather than just looking for the cheapest policy.

- Insure the Reconstruction Cost Only: Never include the land value in your sum insured. Over-insuring is a waste of premium since land doesn’t “burn down”.

- Bundle Your Policies: Many Indian insurers like HDFC ERGO or ICICI Lombard offer discounts of 10-15% if you bundle CAR, WCI, and CPM insurance together.

- Enhance Site Security: Installing CCTV cameras, proper fencing, and 24/7 guarding can make your project a “lower risk” in the eyes of an underwriter.

- Choose the Correct Tenure: It is cheaper to buy a policy for 18 months upfront than to buy for 12 months and pay for expensive extensions later.

- Maintain a Good Safety Track Record: Builders who demonstrate a history of zero accidents often receive “no-claim” benefits or better baseline rates.

How Estimators Should Include Builders Risk Insurance in BOQ?

For a professional estimator, builders risk insurance is not an afterthought; it is a critical line item. It should be listed separately under “Preliminaries” or “Project Overheads” in the Bill of Quantities (BOQ).

- Transparency: Listing the insurance cost separately shows your client exactly how their investment is being protected.

- Accuracy: Use actual quotes based on 2026 market rates rather than historical percentages to ensure your bid is competitive but realistic.

- Profit Protection: By itemizing these “soft costs,” you ensure they don’t eat into your 10-15% intended profit margin if a lender or RERA authority mandates a specific policy level later.

Step-by-Step Guide to Getting Accurate Builders Risk Insurance Quotes

Getting an accurate quote for how much is builders risk insurance in India requires clear documentation and comparison.

- Define the Sum Insured: Calculate the total project value including materials, labor, and professional fees.

- Prepare Project Details: Have your site address, sanctioned plans, construction schedule, and contractor details ready.

- Compare Multiple Quotes: Use digital aggregators or contact insurers like New India Assurance, ICICI Lombard, and HDFC ERGO directly.

- Check the “Fine Print”: Pay attention to the “excess” (the amount you pay per claim) and specifically check for “Special Perils” like earthquake and flood coverage.

- Finalize in Joint Names: For bank-financed projects, ensure the policy is in the joint names of the owner, contractor, and the bank.

Conclusion

Understanding how much does builders risk insurance cost is a fundamental step in modern Indian project management. In 2026, with average premiums ranging from 0.5% to 1.5% of your project value, insurance remains one of the most affordable ways to protect 100% of your capital investment. Whether you are a self-builder in Meerut or a developer in the Delhi-NCR region, accurate budgeting for builders risk insurance ensures that your dream project survives the construction phase to become a reality.

Don’t leave your financial foundation to chance. Get accurate quotes early and build with the confidence that your project is fully protected from groundbreaking to handover. For professional BOQ services and construction cost estimation that accurately factor in all necessary insurance premiums, contact Construction Estimator India today. Let us help you build a secure and profitable future.

FAQ Section

How much does builders risk insurance cost in India in 2026?

On average, the premium ranges from 0.5% to 1.5% of the total project value. For a ₹50 Lakh residential project, this typically amounts to ₹25,000 to ₹75,000 including taxes and basic riders.

What is the average premium rate for builders risk insurance?

The standard rate in India is approximately 0.8% to 1.2% for most residential and civil projects, though it can vary based on location and risk.

How is builders risk insurance cost calculated?

It is calculated by applying a specific rate (based on risk) to the total sum insured (reinstatement value), then adding premiums for any selected add-ons and 18% GST.

Is builders risk insurance cheaper for small projects?

While the total premium is lower, the percentage rate for small projects (like ₹10-20 Lakh renovations) can sometimes be slightly higher than for multi-crore projects due to minimum administrative fees.

What factors increase the cost of builders risk insurance?

Key cost-drivers include being in high seismic or flood zones, having a long construction duration, involving deep basement work, and adding expensive riders like escalation or surrounding property cover.

How much should I add for builders risk insurance in my BOQ?

A safe estimate for your BOQ is to allocate 1% to 1.5% of the total civil construction value as a distinct line item for “Insurance and Statutory Compliance”.

Does adding add-ons significantly increase the cost?

Add-ons like debris removal or escalation clauses usually only add a small fraction (often 10-15%) to the base premium but provide essential coverage for 2026 market realities.

Can self-build homeowners get affordable builders risk insurance?

Yes, individual homeowners building their own villas can purchase “Single Project” CAR policies from most major Indian insurers, which are specifically designed for independent builds.

How does builders risk insurance cost compare with completed building insurance?

Builders risk insurance is more expensive because an active site is much riskier. Once construction is complete, the premium for a standard “Bharat Griha Raksha” policy drops significantly, often to about 0.2% of the value.

Where can I get the best quotes for builders risk insurance?

You can obtain quotes from major Indian insurers such as New India Assurance, ICICI Lombard, HDFC ERGO, and SBI General, or use digital platforms like Policybazaar to compare.