Imagine a mid-sized construction company based in Meerut, securing a prestigious ₹150 crore residential project in the heart of the Delhi-NCR region. Six months into the project, a severe, unseasonal monsoon event causes a structural collapse of the basement shoring, while simultaneously, a tragic site accident leads to worker fatalities and falling debris damages a fleet of luxury cars on an adjacent property. Without a tailored portfolio that includes construction all risk insurance, this firm faces more than just repair costs; it faces total insolvency, legal debarment, and personal liability for its directors. In the high-stakes Indian infrastructure landscape of 2026, such scenarios are not just worst-case—they are statistically probable risks that every builder must mitigate.

Construction projects involve numerous inherent risks, including natural calamities, theft of expensive materials like steel, site fires, and third-party liability claims. Construction all risk insurance (commonly known as CAR insurance) is a comprehensive “all-risk” policy designed to protect your project. It covers sudden and unforeseen physical loss or damage to the contract works, construction materials, and third-party liability during both the construction and maintenance phases. Also known as a contractors all risk policy, it is essential for risk management, tender compliance, securing bank financing from institutions like SBI or HDFC, and ensuring accurate project costing. This guide provides a detailed breakdown of CAR insurance in India 2026, explaining its coverage, exclusions, and how to integrate it into your Bill of Quantities (BOQ).

What is Construction All Risk Insurance?

Construction all risk insurance is recognized as the “gold standard” for civil engineering projects, ranging from residential villas in Meerut to massive flyovers in Noida. It is a specialized “all-risk” policy, meaning it covers all sudden and unforeseen physical loss or damage to the property except for what is specifically excluded. Unlike “named peril” policies that only cover listed events, a CAR policy provides a broad shield for the “work-in-progress”.

This policy protects the “physical anatomy” of the project from the moment of groundbreaking until the final handover or the issuance of a completion certificate. It typically includes two main sections: Section I for physical damage to the works (including materials on-site) and Section II for third-party liability. For construction companies today, this insurance ensures that a single site catastrophe does not drain the reserves of the entire organization, providing financial liquidity to resume work immediately after a disaster.

Why Every Contractor Needs Construction All Risk Insurance?

In the 2026 infrastructure boom, the risks you face are layered and complex. Whether you are a general contractor in Noida or an independent builder in Meerut, your liability is total.

- High Environmental Risks: North India, particularly the Delhi-NCR region, sits in a high seismic zone (Zone IV/V). Unpredictable monsoons, flash floods, and extreme weather events in Uttar Pradesh can cause sudden structural collapses or damage to expensive materials like TMT bars and cement.

- Statutory and Legal Compliance: You have legal obligations under the BOCW Act (Building and Other Construction Workers Act) and RERA to ensure site safety and financial protection.

- Lender and Tender Mandates: Banks almost always mandate a comprehensive contractors all risk policy before releasing project finance. Furthermore, having a robust general contractor insurance India portfolio is often a prerequisite for winning government tenders.

- Financial Protection against Theft: Theft of high-value materials like copper wiring and steel is a rising concern in tier-2 cities. CAR insurance specifically covers burglary and vandalism on-site.

- Professional Reputation: Insurance signals to clients that you are a professional partner capable of handling unforeseen disasters without halting the project permanently.

What Does Construction All Risk Insurance Cover?

The core value of CAR insurance coverage lies in its exhaustive list of protected risks. In the context of 2026 Indian construction, these covers are indispensable for protecting your hard work from groundbreaking to handover.

Physical Material Damage

This section covers the actual permanent structure (walls, slabs, foundations), temporary works (scaffolding, site offices), and construction materials (bricks, steel, premium tiles) stored on-site or in transit.

- Fire and Natural Perils: Protection against fire, lightning, explosions, and gas cylinder mishaps. It also shields against “Special Perils” like floods, cyclones, inundation during monsoons, and earthquakes.

- Theft and Burglary: Covers the theft of raw materials and small equipment on-site, provided there is evidence of forceful entry.

- Structural Failures: Protection against sudden collapse, subsidence, or impact damage from vehicles or falling trees.

Third-Party Liability

CAR insurance includes a critical section that pays for legal costs and compensation if your site activities accidentally cause bodily injury to a passerby or damage to a neighbor’s property. This is essential in crowded urban areas like Meerut or Noida.

Maintenance Period Coverage

The policy typically includes a “maintenance period” (usually 12 months) to cover defects discovered shortly after the project is handed over to the client.

Common Add-on Covers

In 2026, estimators should consider several vital riders:

- Debris Removal: Covers the cost of clearing the site after a major accident.

- Escalation: Increases the sum insured (usually by 10-20%) to account for rising material costs during the build.

- Architect’s and Surveyor’s Fees: Covers professional costs for redesigning after a loss.

- Advance Loss of Profits (ALOP): Also known as Delay in Start-up (DSU), this covers loss of revenue if a project’s completion is delayed by an insured event.

What is NOT Covered under CAR Insurance (Major Exclusions)?

While comprehensive, a contractors all risk policy does not cover everything. You must be aware of the “fine print” to avoid claim rejections.

- Faulty Design and Poor Workmanship: Damage resulting from incorrect engineering designs or substandard construction methods is generally excluded.

- Willful Negligence: Intentional damage caused by the insured or their management.

- Gradual Deterioration: Normal wear and tear, rust, or lack of maintenance over time is not covered.

- War and Nuclear Risks: Universal exclusions for losses arising from war or nuclear radiation.

- Penalties for Delay: Standard CAR policies do not cover liquidated damages or fines for missing project deadlines unless specific ALOP riders are added.

- Inventory Shortages: Claims based solely on inventory or stock-taking discrepancies without evidence of theft.

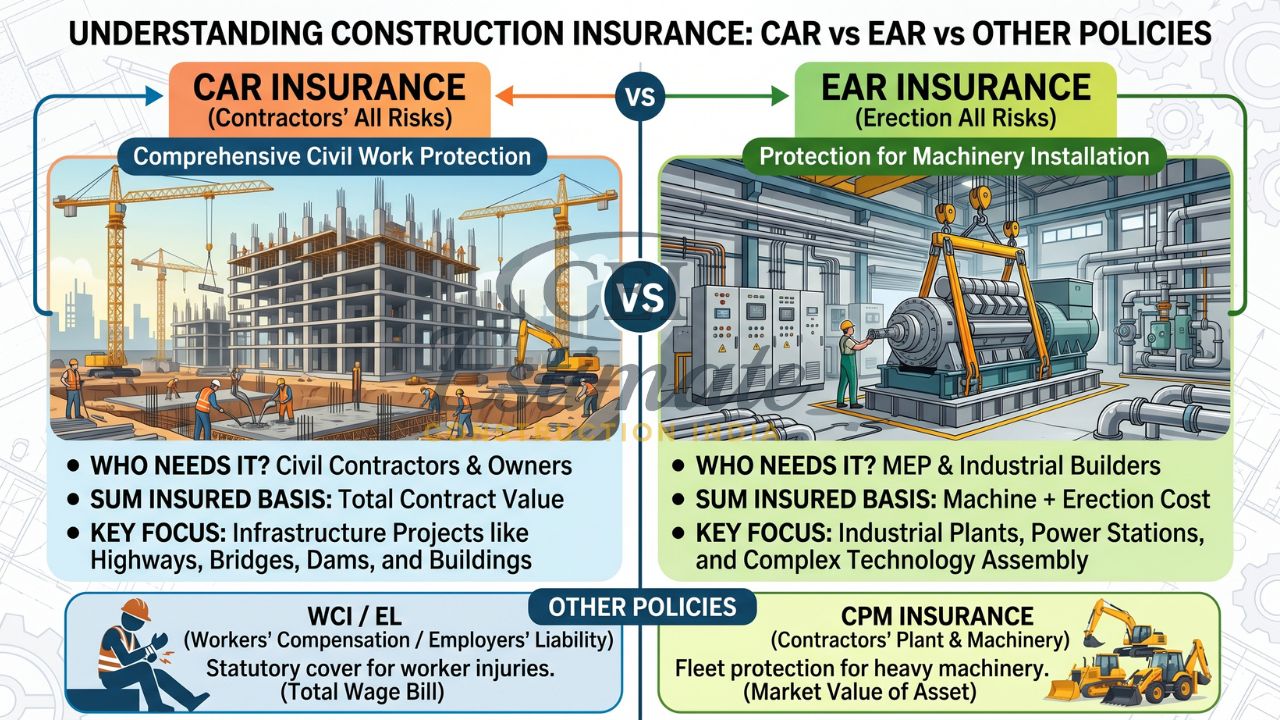

CAR Insurance vs EAR Insurance vs Other Policies

Selecting the right policy depends on whether your project is primarily civil work or involves heavy machinery installation.

| Policy Type | Primary Purpose | Who Needs It? | Sum Insured Basis |

|---|---|---|---|

| CAR Insurance | Comprehensive civil work protection. | Civil Contractors & Owners. | Total Contract Value. |

| EAR Insurance | Protection for machinery installation. | MEP & Industrial Builders. | Machine + Erection Cost. |

| WCI / EL | Statutory cover for worker injuries. | All Labor Employers. | Total Wage Bill. |

| CPM Insurance | Fleet protection for heavy machinery. | Equipment Owners. | Market Value of Asset. |

How Much Does Construction All Risk Insurance Cost in India?

The cost of construction all risk insurance in 2026 typically ranges from 0.5% to 1.5% of the total project value. For a residential villa project in Meerut worth ₹1 crore, the premium would likely fall between ₹50,000 and ₹1,50,000 depending on the add-ons.

Several factors drive these premiums:

- Project Location: Sites in high seismic zones like Delhi-NCR or flood-prone areas in UP attract higher rates.

- Project Duration: A 12-month build is cheaper to insure than a 36-month high-rise project.

- Type of Construction: RCC frame structures are seen as lower risk than those involving deep basement excavations.

- Contractor Track Record: Builders with zero previous claims and strict safety protocols can negotiate more competitive rates.

Step-by-Step Guide to Buying Construction All Risk Insurance

- Define Sum Insured: Use the 2026 “reinstatement value” (total cost to rebuild, including materials, labor, and professional fees) rather than historical costs.

- Gather Project Documents: Prepare the site address, building plans, sanctioned schedule, and contractor details.

- Compare Quotes: Obtain at least three quotes from top insurers like New India Assurance, ICICI Lombard, or HDFC Ergo.

- Finalize Add-ons: Ensure you include critical riders like escalation, debris removal, and third-party liability.

- Policy in Joint Names: For bank-financed projects, the policy must usually be in the joint names of the project owner, contractor, and the bank.

Claims Process under Construction All Risk Insurance

If an accident happens, your speed determines the payout.

- Immediate Intimation: Notify the insurer within 24-48 hours.

- Documentation: Take extensive photos/videos before moving debris.

- Surveyor Visit: Do not start repairs until an official surveyor has visited the site.

- Police Report: Obtain a First Information Report (FIR) immediately in cases of theft or vandalism.

- Maintain Records: Keep all material and labor invoices as proof of original construction costs.

How Estimators Should Include CAR Insurance in BOQ?

As a professional estimator, you should never treat insurance as a “lump sum” guess. It should be listed as a distinct line item in your Bill of Quantities (BOQ) under “Preliminaries” or “Statutory Compliance”. By itemizing the CAR and WCI premiums, you demonstrate professionalism to the client and prevent these “soft costs” from eroding your profit margins. At Construction Estimator India, we recommend using actual quotes based on the total contract value to ensure your bid is both competitive and secure.

Conclusion

Mastering the complexities of construction all risk insurance is what separates a stable, long-term industry leader from a firm vulnerable to the next monsoon storm. From protecting your massive civil projects to satisfying stringent bank requirements, these policies are the invisible foundation of your growth in the Indian landscape of 2026. Don’t let a single unforeseen site accident derail your corporate vision or drain your hard-earned profit margins.

Ensure your next project is built on a foundation of total financial security. Secure your proper CAR coverage today and contact Construction Estimator India for professional BOQ and construction cost estimation services that accurately factor in all necessary insurance costs.

FAQ Section

What is construction all risk insurance?

It is a comprehensive “all-risk” policy covering physical damage to works, materials on-site, and third-party liability during the construction period.

What is covered under CAR insurance in India?

Coverage includes damage from fire, flood, earthquake, theft, burglary, collapse, and third-party bodily injury or property damage.

What is the difference between CAR and EAR insurance?

CAR is for civil works (buildings, roads), whereas EAR focuses on the installation and testing of mechanical and electrical machinery.

How much does construction all risk insurance cost?

In 2026, premiums typically range from 0.5% to 1.5% of the total project value, depending on location and risk.

Is CAR insurance mandatory for construction projects?

While not always legally mandated for all private builds, it is almost always required by banks for financing and is standard for government tenders and RERA-registered projects.

What is not covered in a CAR policy?

Major exclusions include faulty design, poor workmanship, willful negligence, war, and normal wear and tear.

How is the sum insured calculated for CAR insurance?

It is based on the total contract value, including materials, labor, and professional fees, plus an optional escalation factor for rising costs.

Can small contractors buy CAR insurance?

Yes, many insurers offer “Single Project” policies specifically tailored for small residential renovations and independent builds.

How do I include CAR insurance in my BOQ?

List it as a specific line item under “Project Overheads” or “Preliminaries” based on actual market quotes.

Which companies offer good CAR insurance in India?

Top-rated providers for 2026 include New India Assurance, ICICI Lombard, HDFC Ergo, and Bajaj Allianz.