Imagine Suresh, a hardworking mason from Meerut, Uttar Pradesh, who has spent over a decade perfecting his craft. During a high-stakes residential project in the peak of the 2026 monsoon, a sudden gust of wind caused a temporary scaffolding structure to buckle. Suresh fell twelve feet, sustaining severe spinal injuries that left him unable to walk. For Suresh, this meant the end of his livelihood; for his family, it meant immediate financial ruin. For his contractor, who had neglected proper coverage, it meant a barrage of legal notices, a ₹15 lakh compensation demand, and a complete freeze on the project by local authorities. This tragic scenario illustrates exactly why need insurance for construction workers in India is a question that every professional must answer with action before a shovel hits the dirt.

The construction industry in India is famously high-risk, characterized by daily exposure to falls from height, electrocution, heavy machinery mishaps, and erratic weather patterns. With millions of workers—mostly unorganized and migrant—forming the backbone of our infrastructure, the potential for accidents is ever-present. As a contractor or project owner, you must realize that providing insurance for construction workers is not merely a legal formality; it is a fundamental pillar of ethical construction management. Key legislations, specifically the Employees’ Compensation Act 1923 and the Building and Other Construction Workers (BOCW) Act 1996, mandate these protections to ensure worker welfare and employer security. This guide will explore the critical reasons—legal, financial, humanitarian, and business-related—why you must prioritize worker insurance and how to include these costs accurately in your project estimates.

For a broader view of all project protections, read our complete guide on types of construction insurance in India.

The High-Risk Nature of Construction Work in India

Construction sites in India, particularly for residential and small-scale projects in growing cities like Meerut or Noida, are minefields of potential hazards. Workers often navigate unfinished slabs, precarious scaffolding, and live electrical conduits under extreme pressure to meet deadlines. Recent industry statistics indicate that the construction sector consistently reports some of the highest fatal accident rates in the country, with thousands of deaths and permanent disabilities recorded annually due to falls, material collapses, and equipment failure.

These risks are amplified because the workforce is frequently composed of migrant laborers who may lack formal safety training or a social safety net in their host city. When you operate a site, you are managing a dynamic environment where a single mistake or a natural calamity—like the seismic tremors common in Delhi-NCR’s Zone IV/V—can result in catastrophic injury. Understanding this inherent danger is the first step in recognizing why insurance for construction workers is important in India; it acknowledges the reality that safety protocols, while essential, cannot eliminate risk entirely.

Legal Requirements – Why Insurance is Mandatory

One of the most compelling reasons for insurance for construction workers is the strict legal framework governing the industry. The Employees’ Compensation Act 1923 establishes that you, as an employer, are legally liable to pay compensation for any injury, disability, or death arising “out of and in the course of employment”. This liability exists regardless of whether the worker was directly at fault. Furthermore, the Building and Other Construction Workers (BOCW) Act 1996 mandates welfare measures, including the registration of workers and the payment of a labor welfare cess (usually 1-2% of project cost) to fund state-level accident relief.

Compliance with these laws is a non-negotiable legal requirement for worker insurance in construction. If an accident occurs and you are found to be uninsured or unregistered, the penalties are severe. Courts can impose fines exceeding ₹50,000, order the immediate payment of full compensation with heavy interest, and even pursue criminal charges or imprisonment for the principal contractor. In many cases, the principal contractor is held responsible for the lapses of their subcontractors, making it vital to ensure that every individual on your muster roll is covered.

For detailed statutory obligations, refer to our guide on workers comp requirements for construction businesses in India.

Financial Protection for Employers and Contractors

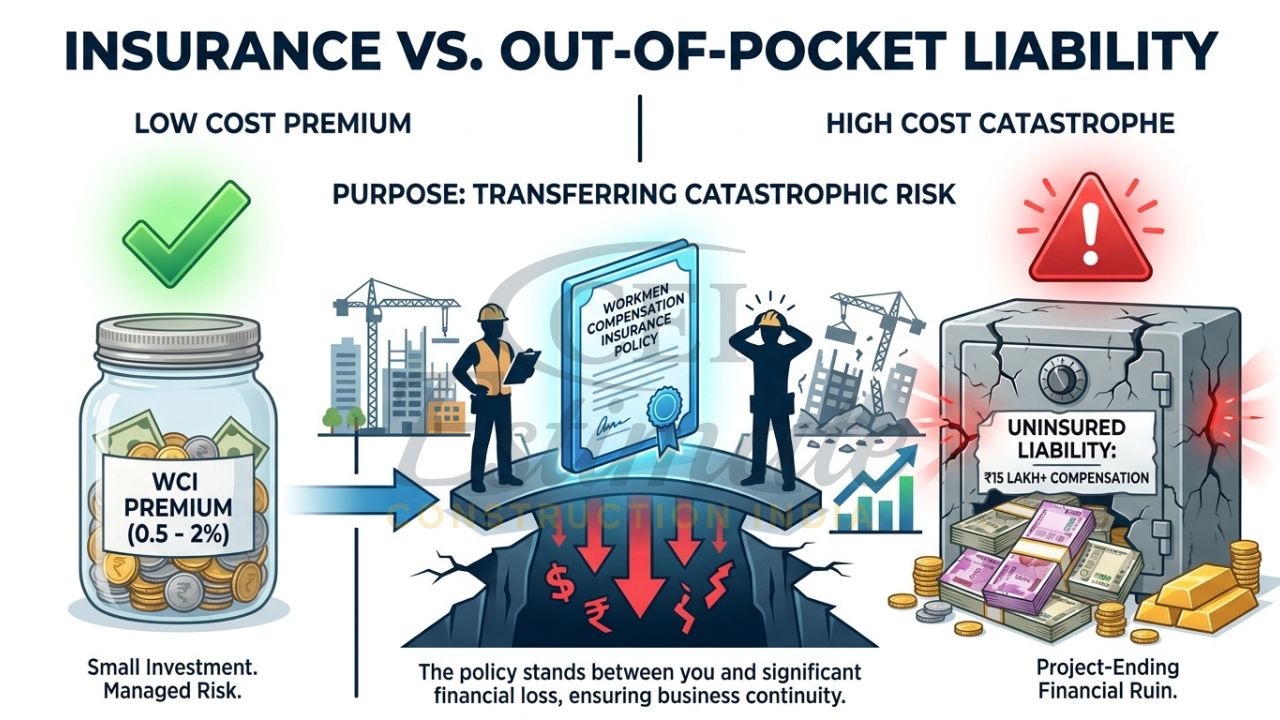

Without insurance, the financial burden of a site accident falls squarely on your shoulders. A single construction worker accident compensation India payout for a death or permanent disability can range from ₹8 lakh to ₹15 lakh or more, depending on the worker’s age and wages. For a small builder or independent contractor, such a sudden out-of-pocket expense can lead to immediate bankruptcy or the forced liquidation of personal assets.

By securing a Workmen Compensation Insurance (WCI) policy, you transfer this massive financial risk to the insurer. The policy covers not just the compensation amount, but often the medical expenses and legal defense costs associated with the claim. This protection ensures your project’s cash flow remains stable and your business continues to operate even in the face of a tragedy. In the 2026 market, where material costs are volatile, avoiding these “unforeseen soft costs” is essential for maintaining project solvency.

To understand full project risk budgeting, explore our detailed analysis on how much is insurance for construction in India.

Humanitarian and Social Welfare Benefits

Beyond the balance sheet, there is a profound social responsibility attached to construction management. Most laborers in India live hand-to-mouth, and an injury to the primary breadwinner can push a family into generational poverty. Insurance provides a critical safety net, ensuring that workers receive immediate, high-quality medical care and that their dependents are not left destitute in the event of a fatality.

Welfare-oriented contractors often integrate private insurance with government schemes like the Pradhan Mantri Suraksha Bima Yojana (PMSBY), which offers ₹2 lakh accidental cover for just ₹20 per year. Additionally, registration with state BOCW welfare boards gives workers access to pensions, maternity benefits, and educational scholarships for their children. This holistic approach to worker well-being fosters a more loyal, confident, and productive workforce on your site.

Business and Project Benefits

From a business perspective, being a “fully insured” contractor is a significant competitive advantage. In 2026, most government departments and large-scale real estate developers mandate proof of worker insurance before awarding tenders or releasing project funds. Lenders and banks also require these policies to protect their investment during the construction phase.

Furthermore, having a robust insurance portfolio builds immense trust with clients. When a self-constructing homeowner in Meerut sees that you have protected the workers on their site, it reflects your professionalism and attention to detail. It also prevents project delays; a site where an accident occurs without insurance is often shut down by labor commissioners for months, leading to massive reputational damage and lost opportunities.

For larger or commercial-scale operations, specific compliance is essential. Read our guide on commercial construction insurance requirements in India.

What Happens If You Don’t Have Insurance – Real Risks and Penalties?

The cost of not having insurance for construction workers far outweighs the relatively low premium costs. If an accident occurs on an uninsured site, you face:

- Direct Financial Liability: You must pay the full compensation amount determined by the Labor Commissioner immediately.

- Interest and Penalties: Late payments often attract interest rates of 12% or more, along with additional statutory penalties.

- Legal Battles: You may be embroiled in lengthy litigation that drains your time and resources.

- Project Stoppage: Authorities can issue “Stop Work” notices, leading to missed deadlines and contractual penalties.

- Blacklisting: Your firm may be barred from bidding on future government or high-profile private contracts.

Types of Insurance Needed for Construction Workers

To build a complete safety net, you should consider a mix of mandatory and recommended policies:

| Insurance Type | Coverage Focus | Mandatory Status |

|---|---|---|

| Workmen Compensation (WCI) | Legal liability for injury, death, and occupational disease. | Mandatory |

| BOCW Registration | State-funded health, education, and accident relief. | Mandatory |

| Group Personal Accident (GPA) | 24/7 accidental death and disability cover for staff. | Recommended |

| PMSBY | Affordable government accidental death cover (₹2 lakh). | Recommended |

| CAR Integration | Third-party liability and site-specific worker riders. | Recommended |

For small and growing contractors, explore affordable options in our article on best insurance for small construction business in India.

How to Include Insurance Costs in Your BOQ and Project Estimates?

For construction estimators and contractors, worker insurance should never be a “hidden cost.” In the 2026 market, WCI premiums typically range from 0.5% to 2% of the total labor wage bill. To ensure your project remains profitable, you must:

- Calculate the Wage Bill: Estimate the total labor cost for the project duration.

- Add a Specific Line Item: List “Worker Insurance & Compliance” as a separate row in your Bill of Quantities (BOQ).

- Factor in Cess: Include the 1% labor welfare cess required under the BOCW Act.

- Use Risk Multipliers: If the work involves high-rise structures or heavy machinery, increase the allocated percentage to account for higher premiums.

When hiring external labor, proper arrangements are essential. Learn more in our guide on how to get insurance for subcontractors in India.

Step-by-Step Guide to Arranging Insurance for Your Workers

- Register Your Workers: Ensure every laborer is registered with the state BOCW Board to access government benefits.

- Assess Total Liability: Determine the number of workers and their average monthly wages to find the required sum insured for WCI.

- Obtain Quotes: Compare offerings from reputable Indian insurers like New India Assurance, HDFC Ergo, or ICICI Lombard.

- Verify Subcontractors: If you hire labor through a contractor, verify their WCI policy or cover their workers under your own master policy.

- Maintain Muster Rolls: Keep meticulous records of attendance and wages; these are essential for a smooth claims process.

Conclusion

Understanding why need insurance for construction workers in India is fundamental to your success as a modern builder. It is the bridge between a high-risk gamble and a professional, sustainable business. By prioritizing Workmen Compensation and BOCW compliance, you protect your workers from financial ruin, your project from legal shutdowns, and your company from bankruptcy. In 2026, safety is not just an expense; it is your ultimate competitive advantage.

Don’t leave your site’s future to chance. Ensure your workforce is protected and your project costs are accurately calculated from the start. For expert assistance, contact Person at Construction Estimator India for professional BOQ and construction cost estimation services that properly account for every insurance and compliance cost.

FAQ Section

Why do we need insurance for construction workers in India?

It is needed for three main reasons: to comply with mandatory laws like the Employees’ Compensation Act, to protect contractors from massive financial liability in case of accidents, and to provide a social safety net for vulnerable workers and their families.

Is Workmen Compensation Insurance mandatory for construction sites?

Yes. Under the Employees’ Compensation Act 1923, any employer in a hazardous industry like construction is legally liable to compensate workers for employment-related injuries or death.

What are the benefits under the BOCW Act for construction workers?

Registered workers can access state-funded accident relief, medical assistance, pensions, maternity benefits, and educational support for their children.

What happens if a contractor does not provide insurance to workers?

The contractor becomes personally liable for the full compensation amount, faces heavy legal penalties/fines, and risk their project being shut down by the labor department.

How much compensation is paid in case of worker death or injury?

Compensation is calculated based on the worker’s age and monthly wages. For death, it is often a lump sum ranging from ₹8 lakh to ₹15 lakh or more.

Does insurance cover subcontractors’ workers?

While subcontractors should have their own, the “Principal Employer” (main contractor/owner) is often held legally liable for all workers on site. It is best to cover everyone under a single master policy.

How can small contractors arrange insurance affordably?

Small contractors can combine a basic WCI policy with affordable government schemes like PMSBY (₹20/year) and ensure all workers are registered under the BOCW Board for state benefits.

How do I include worker insurance cost in my BOQ?

List it as a separate line item under “Preliminaries” or “Project Overheads,” usually calculated as 0.5% to 2% of the total labor wage bill plus the 1% labor cess.

Is personal accident insurance enough or do I need full Workmen Compensation?

Personal accident insurance is voluntary and doesn’t fulfill your legal obligations. You must have WCI to satisfy the statutory requirements of the Employees’ Compensation Act.

Suggested Related Guides: