Imagine you are a contractor in Meerut, Uttar Pradesh, nearing the final phase of a residential villa project. You have invested months of labor and lakhs in premium materials like TMT bars and teak wood frames. One evening, an unseasonal monsoon cloudburst triggers a localized flash flood that ruins your cement inventory and causes a retaining wall to collapse onto a neighbor’s vehicle. When you reach out to your insurer, you realize your standard home policy doesn’t cover “work-in-progress”. This financial nightmare is common for builders who fail to distinguish between specialized construction policies.

Navigating the landscape of Indian construction insurance requires more than just picking the cheapest plan. Builders Risk Insurance, often obtained as part of a Contractors All Risk (CAR) policy, is the bedrock of project safety. However, for total project solvency, you must understand how its cost and coverage compare with other mandatory protections like Workmen Compensation or Subcontractor Insurance. This guide will break down the 2026 market realities, helping you build a robust financial shield from groundbreaking to final handover.

What is Builders Risk Insurance and Why Do You Need It?

Builders Risk Insurance is a specialized financial product designed to protect “property in course of construction”. In India, it is typically marketed as a component of a Contractors All Risk (CAR) policy or Erection All Risk (EAR) policy, depending on whether the project is civil-heavy or machinery-heavy.

Unlike a finished home policy (such as Bharat Griha Raksha), which requires a completion certificate to be effective, Builders Risk covers the site while it is at its most vulnerable—unfenced, exposed to weather, and filled with loose raw materials. It provides a comprehensive “all-risk” shield against:

- Physical Damage: Damage to the permanent structure (foundations, walls, slabs) from fire, lightning, or natural calamities.

- Material Theft: Theft of expensive raw materials like steel, copper wiring, and high-end fittings, provided there is evidence of housebreaking.

- Temporary Works: Coverage for scaffolding, shuttering, and site offices that are essential for construction but not part of the final building.

- Third-Party Liability: Protection against legal claims if your site activities accidentally injure a visitor or damage a neighbor’s property.

For self-building homeowners and independent contractors in high-risk seismic zones like the Delhi-NCR, this insurance is not a luxury—it is a prerequisite for project survival and a mandatory requirement for most construction-linked bank loans.

Builders Risk Insurance Cost in India 2026 – Realistic Pricing

As we navigate the 2026 construction market, transparency in budgeting is vital. You should never treat insurance as a hidden “lump sum” in your contingency fund. Instead, it should be a precise line item in your Bill of Quantities (BOQ).

Generally, the how much does builders risk insurance cost in India ranges between 0.5% and 1.5% of the total project value. This premium usually covers the entire project duration with a one-time payment. For professional estimators, the “cost per crore” is a standard benchmark, typically ranging from ₹60,000 to ₹1,20,000 per crore of construction value.

Table 1: Estimated 2026 Builders Risk Insurance Costs by Project Size

| Project Type | Project Value | Estimated Premium Range (Basic CAR) | Percentage of Project Value |

|---|---|---|---|

| Small Independent Floor | ₹30 Lakhs | ₹15,000 – ₹25,000 | 0.5% – 0.8% |

| Mid-size Residential Villa | ₹1 Crore | ₹60,000 – ₹1,20,000 | 0.6% – 1.2% |

| Small Apartment Complex | ₹3 Crores | ₹1,80,000 – ₹3,50,000 | 0.6% – 1.1% |

| Large Housing Project | ₹5 Crores+ | ₹2,50,000 – ₹6,50,000 | 0.5% – 0.8% |

Several factors influence these rates, including the geographic location (projects in seismic Zone IV/V like Noida face higher premiums), project duration, and the contractor’s safety track record. High-quality external resources like the General Insurance Council can provide further insights into standardized risk assessments used by Indian insurers.

Builders Risk Insurance vs Other Construction Insurance Policies – Detailed Comparison

To manage a project effectively, you must distinguish between protecting the property, the people, and the legal liabilities. While Builders Risk is the “hero” policy for structure and materials, it is often insufficient on its own.

1. Builders Risk vs. Contractors’ All Risk (CAR) Insurance

In the Indian context, these terms are often used interchangeably, but there is a nuance. Builders Risk focuses primarily on the property value. CAR is a broader “package” that includes Builders Risk plus Third-Party Liability (TPL) and sometimes even Cross Liability for subcontractors. Most reputable insurers like New India Assurance or ICICI Lombard bundle these together for convenience.

2. Builders Risk vs. Workers Compensation Insurance

While Builders Risk protects your bricks and mortar, Workmen Compensation Insurance (WCI) protects your human capital. This is a non-negotiable legal requirement under the Employees’ Compensation Act 1923 and the BOCW Act 1996. If a worker falls from a scaffold, Builders Risk will not pay for their medical bills—only a WCI policy will. For a deeper dive into these mandates, see our guide on workers comp requirements for construction businesses in India.

3. Builders Risk vs. Subcontractor Insurance

As a main contractor, you are often the “Principal Employer”. If a plumbing subcontractor’s mistake causes a fire, your Builders Risk policy might cover the damage, but the insurer could then “subrogate” (sue) the subcontractor to recover costs. To avoid internal legal battles, it is essential to know how to get insurance for subcontractors in India—either by naming them as “Joint Insured” on your master policy or mandating they have their own cover.

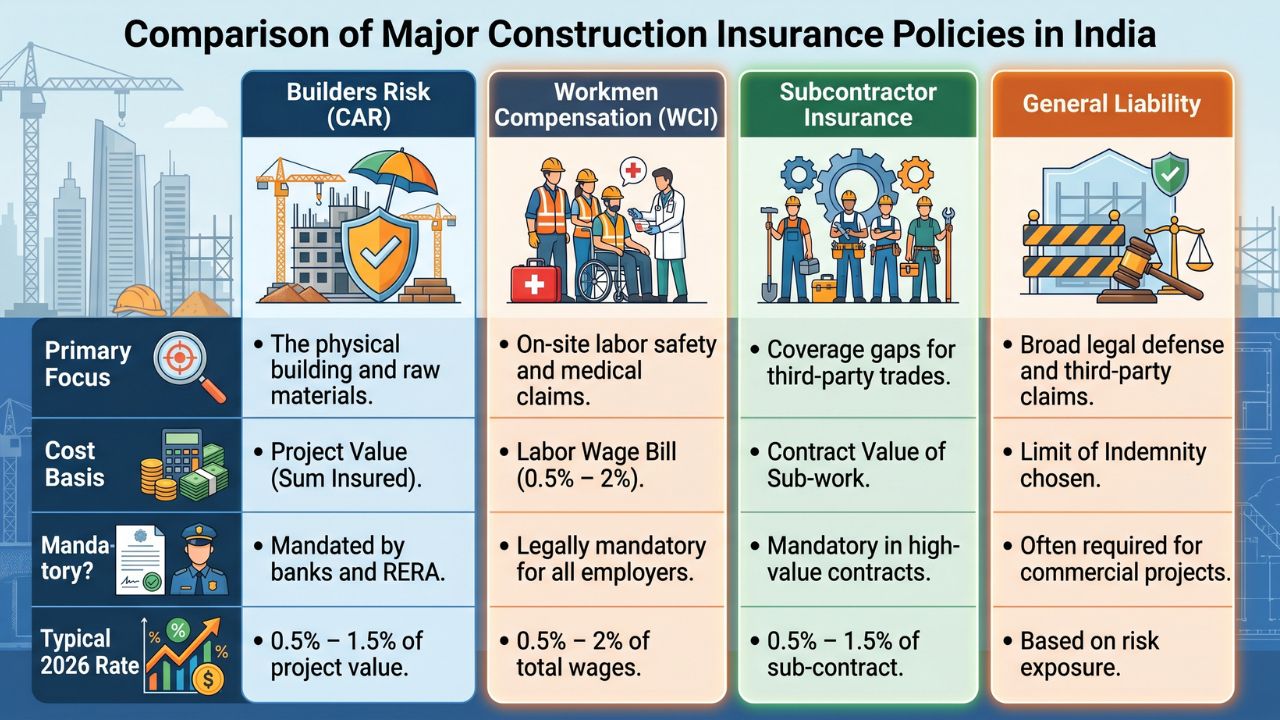

Table 2: Comparison of Major Construction Insurance Policies in India

| Feature | Builders Risk (CAR) | Workmen Compensation (WCI) | Subcontractor Insurance | General Liability |

|---|---|---|---|---|

| Primary Focus | The physical building and raw materials. | On-site labor safety and medical claims. | Coverage gaps for third-party trades. | Broad legal defense and third-party claims. |

| Cost Basis | Project Value (Sum Insured). | Labor Wage Bill (0.5% – 2%). | Contract Value of Sub-work. | Limit of Indemnity chosen. |

| Mandatory? | Mandated by banks and RERA. | Legally mandatory for all employers. | Mandatory in high-value contracts. | Often required for commercial projects. |

| Typical 2026 Rate | 0.5% – 1.5% of project value. | 0.5% – 2% of total wages. | 0.5% – 1.5% of sub-contract. | Based on risk exposure. |

Best Insurance for Small Construction Business in India

For small builders in Meerut or Noida, cash flow is king. You cannot afford to be over-insured, but a single uninsured accident can end your business. The best insurance for small construction business in India is typically a bundled package.

For a small residential contractor, we recommend a “Balanced Protection” package consisting of CAR Insurance + WCI. This ensures that if a monsoon destroys your site (CAR) and injures a worker (WCI), you are protected on both fronts. Leading private insurers such as HDFC Ergo offer digital-first portals where small builders can get quotes instantly based on their project value and worker count.

Small Business Pro-Tips:

- Include “Escalation Clauses”: Given the volatility of material prices in 2026, add a 10-20% buffer to your sum insured so your payout matches future rebuilding costs.

- Bundle to Save: Many Indian insurers offer 10-15% discounts if you purchase CAR and WCI together.

How to Get Certificate of Insurance and Insurance for Subcontractors?

A Certificate of Insurance (COI) is a one-page summary that acts as a “gatekeeper” for high-stakes projects. Banks and developers will not release funds or allow you to start work without one. You must know how to get a certificate of insurance for contractors in India—usually a 24 to 48-hour process after premium payment.

When it comes to specialized trades, the main contractor bears the ultimate site responsibility. If your electrical sub-contractor causes a short circuit, you could be held liable. Therefore, knowing how to get insurance for subcontractors in India is critical. You should either:

- Add them as Joint Insured: List them on your master CAR policy to ensure the insurer cannot sue them for accidental damages.

- Verify Independent COIs: If they have their own policy, verify the expiry date and ensure your firm is named as an “Additional Insured”.

Workers Compensation Requirements for Construction Businesses?

In India, ignoring labor safety isn’t just a risk; it’s a legal violation. The workers comp requirements for construction businesses in India mandate that every employer provide coverage for death, permanent disability, and medical expenses resulting from site accidents.

In 2026, the Code on Social Security has further tightened these rules. Contractors must maintain digital muster rolls and accident logs. Beyond the private WCI policy, builders must also pay a 1% Labor Welfare Cess under the BOCW Act, which is separate from your insurance premium. Failing to comply can lead to “Stop Work” orders from labor commissioners and hefty legal penalties.

How to Choose the Right Construction Insurance Package?

Selecting the right insurance isn’t just about the lowest premium; it’s about risk alignment. Follow these steps to ensure you’re not leaving your financial foundation to chance:

- Assess Geographic Risks: If your project is in a flood-prone area of Uttar Pradesh or a high-seismic zone in Delhi-NCR, prioritize “Special Perils” coverages.

- Evaluate Project Duration: It is often cheaper to buy an 18-month policy upfront than to buy a 12-month policy and pay for expensive extensions later.

- Check Claim Settlement Ratios: For small businesses, cash flow depends on fast payouts. Research insurers through the IRDAI website to compare their track records in engineering claims.

- Audit Your BOQ: Ensure your estimator has listed insurance as a separate line item under “Preliminaries”. Using a 1% to 1.5% placeholder of the total civil cost is a safe way to protect your profit margins.

Frequently Asked Questions (FAQs)

- Is Builders Risk Insurance mandatory in India?

While not always a federal law for private builds, it is almost always mandated by RERA, banks for construction-linked loans, and government tender authorities. - Does standard home insurance cover construction?

No. Policies like Bharat Griha Raksha are for finished buildings. Under-construction sites require a CAR or Builders Risk policy. - How is the Builders Risk premium calculated?

It is typically 0.5% to 1.5% of the reinstatement value (cost to rebuild), not the land value or market value. - Does it cover theft of materials?

Yes, Builders Risk policies generally cover the theft of raw materials like steel and cement, provided there is evidence of housebreaking. - Can a small contractor afford proper insurance?

Absolutely. For a ₹10 Lakh renovation, a basic policy can cost as little as ₹5,000 to ₹10,000—much cheaper than the cost of a single major accident. - What is the difference between WCI and CAR?

CAR covers the property and third-party property damage; WCI covers injuries and medical costs for your own workers. - Should I include land value in my insurance sum?

No. Never insure the land value, as land doesn’t “burn down” or get stolen. Insuring only the reconstruction cost saves significantly on premiums. - What happens if a project is delayed?

You must notify your insurer before the policy expires to purchase a pro-rata extension. Failing to do so leaves the site uninsured during the most critical finishing stages.

Conclusion

Understanding the builders risk insurance cost in India relative to other policies is the difference between a sustainable construction business and one that is a single monsoon storm away from insolvency. In 2026, with average costs ranging from 0.5% to 1.5% of your project value, insurance remains one of the most affordable ways to protect 100% of your capital investment.

Whether you are an independent builder in Meerut or a developer in the Delhi-NCR, accurate insurance costing in your BOQ is your greatest competitive advantage. Don’t leave your project’s financial foundation to chance. Get proper quotes early, prioritize mandatory WCI compliance, and ensure every subcontractor on your site is protected.

For professional BOQ services and construction cost estimation that accurately factors in all necessary insurance and statutory compliance costs for 2026, contact Construction Estimator India today. Let us help you build a secure, profitable, and worry-free future.