Imagine you are a real estate investor in Noida who has just finalized a high-yield deal for a three-story rental floor. You’ve calculated the cap rate, vetted the tenants, and planned for a 7% annual rent escalation. However, just six months into the lease, a severe monsoon triggers localized flooding and an electrical short circuit in the main panel, causing structural damage and rendering the ground floor uninhabitable. While your tenants are safe, they stop paying rent, and you are hit with a ₹12 lakh bill for structural repairs and debris removal. Without proper building insurance for investment property, your profitable asset suddenly becomes a massive liability.

As an investor in India’s booming real estate hubs like Meerut, Ghaziabad, or Delhi-NCR, you must recognize that rental units, buy-to-let flats, and commercial outlets carry significantly higher risks than self-occupied homes. Tenant usage often leads to higher wear and tear, and the lack of daily personal supervision increases the risk of undetected leaks or electrical hazards. Securing building insurance for investment property India 2026 is no longer just a “best practice”; it is a non-negotiable strategic move to safeguard your capital. This insurance covers the physical anatomy of the building—the foundation, walls, roof, and permanent fixtures—ensuring that your “source of wealth” remains protected against natural and man-made disasters.

In this guide, we will explore why dedicated landlord building insurance for rental investment is critical for your ROI, the nuances of the Bharat Griha Raksha framework, and how to factor insurance costs into your professional Bill of Quantities (BOQ). By the end of this article, you will have a practical roadmap to mitigating risk and maximizing your long-term property returns.

What is Building Insurance for Investment Property?

Building insurance for investment property is a specialized policy designed specifically for landlords and real estate investors. It focuses on protecting the “shell” of the building and its permanent fixtures. Unlike a standard homeowner’s policy, it is drafted with the understanding that you, the owner, do not reside on the premises.

This policy covers the immovable parts of the property. If you were to turn the building upside down and shake it, everything that stays attached is covered. This includes:

- The structural foundation, load-bearing walls, and the roofing system.

- Concealed electrical wiring, plumbing networks, and HVAC systems.

- Permanent installations like built-in wardrobes, modular kitchens (if provided by you), and bathroom fittings.

- Common areas in apartments and shared compound walls or gates.

It is distinct from contents insurance, which is typically the tenant’s responsibility. While you insure the walls, the tenant should insure their furniture and electronics. Furthermore, it is different from a general commercial package because it can be tailored specifically for “buy-to-let” residential units, offering essential add-ons like loss of rent cover for investment property.

Why Investment Property Owners Need Dedicated Building Insurance?

Relying on luck or a standard “Home Secure” policy is a dangerous gamble for an investor. Here is why dedicated coverage is essential for your portfolio:

- Protection of Capital Investment: Your property is likely one of your largest financial assets. In cities like Meerut or Noida, where construction costs are rising, a single fire or earthquake (Zone IV/V risks) could wipe out your entire equity if you are uninsured.

- Mitigating Tenant-Induced Risks: Tenants may not be as diligent as an owner-occupier. A gas cylinder explosion or a localized fire due to tenant negligence can devastate the building’s “bones.” Dedicated insurance provides a safety net against such accidents.

- Mandatory Bank Financing: If you have a home loan or a commercial property loan from HDFC, SBI, or ICICI, the lender will legally mandate insurance for buy-to-let property to protect their collateral.

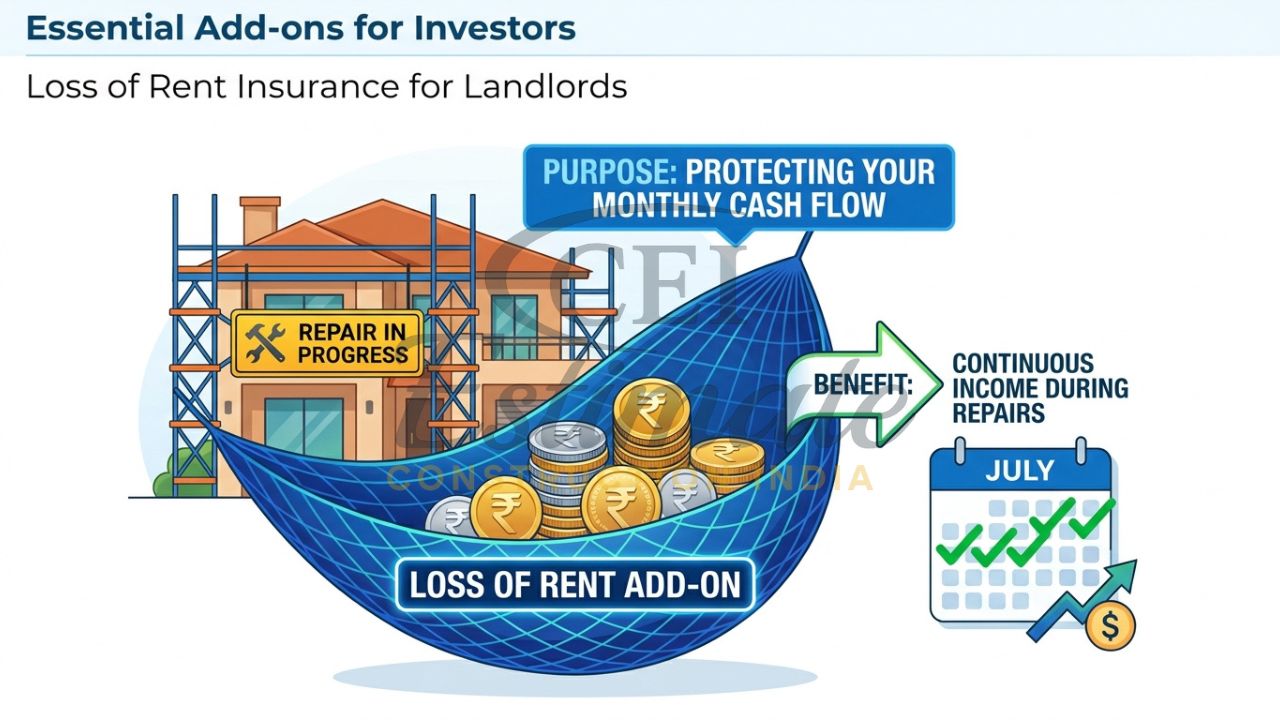

- Safeguarding Cash Flow: The “Loss of Rent” rider is the investor’s best friend. If a fire makes the building uninhabitable, the insurer pays you the rent you would have collected while the repairs are being carried out.

- Liability Protection: If a part of your structure (like a balcony railing) collapses and injures a tenant or a visitor, you could face massive legal and medical claims. Liability coverage within the building policy handles these costs.

What Does Building Insurance for Investment Property Cover?

Under the 2026 guidelines for the Bharat Griha Raksha for investment flats, you receive comprehensive protection against a wide array of “Insured Perils.” For investors in North India, where monsoons and seismic activities are frequent, the following coverage is critical:

- Natural Calamities: Covers damage from earthquakes, floods, inundation, storms, cyclones, and landslides.

- Fire and Explosions: Protects against accidental fire, lightning strikes, and domestic gas explosions.

- Man-Made Perils: Damage caused by riots, strikes, malicious acts, or acts of terrorism (usually a standard inclusion in 2026).

- Impact Damage: If a vehicle crashes into your boundary wall or a falling tree damages the roof of your rental villa.

- Plumbing Failures: Coverage for structural damage caused by the bursting or overflowing of water tanks and pipes.

Essential Add-ons for Investors

To truly optimize your building insurance for investment property, you must look beyond the basic structure. We recommend the following riders:

- Loss of Rent: Compensates you for the actual rental income lost if the property becomes unfit for habitation due to a covered peril.

- Alternative Accommodation: Covers the cost of moving your tenants to a temporary location, which can help you maintain your lease agreement and reputation.

- Debris Removal: Pays for the cost of clearing the site after a disaster, which can often run into several lakhs for large multi-story units.

- Escalation Cover: Given the inflation in cement and steel prices in 2026, this add-on automatically increases the sum insured to reflect current reconstruction costs.

Building Insurance vs Contents Insurance for Investment Properties

As a professional landlord, you must understand the demarcation of responsibility to avoid disputes and insurance “gaps.”

| Feature | Building Insurance (Landlord) | Contents Insurance (Tenant) |

|---|---|---|

| What is Protected | Walls, roof, foundation, pipes, wiring. | Furniture, electronics, clothes, jewelry. |

| Who is Responsible | The Real Estate Investor / Landlord. | The Tenant or Resident. |

| Sum Insured Basis | Reinstatement Value (cost to rebuild). | Market Value (depreciated value of items). |

| Primary Goal | Protect capital and structure. | Protect personal possessions. |

| Theft Coverage | Covers damage to doors/windows. | Covers the value of stolen items. |

By securing the building cover, you protect your core asset. You should explicitly mention in your rental agreement that the tenant is responsible for their own contents insurance to avoid legal friction during a claim.

Residential vs Commercial Investment Property Insurance

The risks associated with commercial vs residential investment property insurance vary significantly. Residential investments (flats, villas) are generally covered under the Bharat Griha Raksha framework, which is standardized and highly consumer-friendly. The focus here is on habitable safety and loss of rent.

Commercial investment properties (retail shops, warehouses, office spaces) require a more robust commercial property insurance policy. These buildings face higher risks due to public footfall, heavy machinery, and larger electrical loads. The liability limits for commercial units should be much higher, and the “Loss of Profits” (Advanced Loss of Profits) add-on is often used instead of a simple loss of rent cover to account for business interruption.

How Much Does Building Insurance for Investment Property Cost in India?

The cost of building insurance for investment property in 2026 is surprisingly affordable, usually representing less than 1% of the total annual rental income. However, the premium is calculated on the “Reinstatement Value”—the actual cost to rebuild—rather than the market value of the property.

In 2026, typical annual premium rates range from 0.15% to 0.60% of the reconstruction cost.

- Example 1 (Residential Flat): A 2-BHK investment flat in Ghaziabad with a reconstruction cost of ₹40 lakhs. The annual premium would likely range between ₹2,000 and ₹6,000.

- Example 2 (Small Commercial Shop): A retail outlet in Meerut with a reconstruction value of ₹15 lakhs. Due to higher commercial risks, the premium might be around ₹4,000 to ₹9,000.

Factors that increase the premium include being in a flood-prone area, the age of the building (older structures have higher risks), and the specific profile of the tenants (e.g., a restaurant tenant vs. a boutique store). It is vital to include this recurring cost in your cap rate and cash flow calculations to ensure an accurate ROI.

Step-by-Step Guide to Buying Building Insurance for Investment Property

- Calculate the Reinstatement Value: Do not use the price you paid for the property. Multiply the total built-up area by the current local construction rate (e.g., ₹2,200/sq. ft. in Meerut).

- Review Rental Agreements: Ensure your lease clearly states that you are responsible for the structure and the tenant for the contents.

- Compare Quotes: Visit portals like Policybazaar or contact direct insurers like ICICI Lombard, HDFC Ergo, or SBI General to compare BGR for investment flats.

- Declare Occupancy: It is critical to inform the insurer that the property is “Tenant Occupied.” Failure to disclose this can lead to claim rejection.

- Select Add-ons: Always include loss of rent cover for investment property and debris removal.

- Documentation: Keep your sale deed, property tax receipts, and latest photos of the property ready for the digital application process.

Claims Process for Investment Property

If your investment property suffers damage, efficiency is key to minimizing downtime.

- Immediate Intimation: Notify your insurer within 24 hours via their mobile app or toll-free number.

- Coordinate with Tenants: Instruct your tenants not to move debris or start repairs until the surveyor has visited. Take high-resolution photos and videos of the damage.

- Surveyor Visit: Provide the surveyor with your original construction BOQ and any repair estimates from a professional contractor.

- Rent Loss Documentation: If you are claiming for loss of rent, provide the valid rental agreement and proof of bank transfers for previous months to justify the payout.

Why Estimators and Investors Must Include It in Property Costing?

At Construction Estimator India, we believe that every financial model for a real estate project is incomplete without factoring in insurance. For developers and estimators, including the building insurance for investment property cost in the initial Bill of Quantities (BOQ) ensures that the property is protected from the moment it is handed over to the first tenant.

When we provide investment feasibility studies, we include insurance as a “Fixed Soft Cost.” This professional approach ensures that your projected net operating income (NOI) is realistic and that your capital is never exposed to an unhedged disaster.

Conclusion

Securing building insurance for investment property is the ultimate risk management tool for any serious real estate investor in India. Whether you are managing a portfolio of buy-to-let apartments in Noida or commercial shops in Meerut, a robust policy ensures that your hard-earned capital and your monthly cash flow remain secure against the unpredictable monsoons and seismic risks of North India. By focusing on the reinstatement value and choosing critical add-ons like loss of rent, you transform a vulnerable asset into a resilient investment.

Don’t let your wealth-building journey be derailed by a single accident. Review your current coverage today and ensure it reflects 2026’s construction rates. For professional BOQ services, construction cost estimation, or detailed investment property costing that includes realistic insurance projections, contact Construction Estimator India today. Let us help you build and protect your future.

FAQ Section

What is building insurance for investment property?

It is a specialized policy for landlords that protects the physical structure (walls, roof, foundation) and permanent fixtures of a rental property against perils like fire, flood, and earthquake.

Is building insurance mandatory for rental investment properties?

While not mandatory by law for all, it is almost always mandated by banks if the property is mortgaged. It is also a requirement for RERA-registered projects during the maintenance phase.

What add-ons are most useful for investment property owners?

The most critical add-ons are “Loss of Rent,” “Debris Removal,” “Escalation Cover,” and “Public Liability” to protect against tenant or visitor injuries.

How much does building insurance cost for a rental property in 2026?

Annual premiums typically range from 0.15% to 0.50% of the reconstruction cost. For a ₹50 lakh structure, this is roughly ₹7,500 to ₹15,000 per year.

Who pays for building insurance — landlord or tenant?

The landlord (investor) pays for building insurance to protect their structural asset. The tenant is responsible for buying their own contents insurance.

Does building insurance cover loss of rent if the property is damaged?

Yes, but only if you have specifically included the “Loss of Rent” add-on in your policy. Standard policies may not include this by default.

What is the difference between building insurance for investment vs self-occupied property?

The primary difference is the occupancy declaration and the availability of “Loss of Rent” and landlord-specific liability covers, which are not present in standard homeowner plans.

How is sum insured calculated for investment properties?

It is calculated based on the “Reinstatement Value”—the actual cost of materials and labor to rebuild the structure at current 2026 rates, excluding land cost.

Can I buy building insurance if the property is currently vacant?

Yes, but you must inform the insurer if the property is vacant for more than 30 or 60 days, as this changes the risk profile and may require a specific vacancy rider.

How to include building insurance in my real estate investment calculations?

Include the annual premium as a fixed operating expense when calculating your Net Operating Income (NOI) and Cap Rate to get a true picture of your returns.

Learn more about related topics: