Imagine you are a first-time homebuyer in Meerut or a high-rise apartment investor in Noida. You have spent months finalizing the perfect property, negotiating the price, and meticulously planning your finances. Your home loan from a leading bank like SBI or HDFC is finally approved, and you are ready for the keys. However, just before the final disbursement, the bank representative asks for a copy of the building insurance for mortgage. For many Indian borrowers, this is a moment of surprise and confusion. You might wonder why you need to insure a building you haven’t even fully paid for yet, or perhaps you worry that this is just another hidden cost in an already expensive process.

In reality, securing building insurance for mortgage is a non-negotiable step in the Indian home loan journey 2026. Most banks and housing finance companies (HFCs) in India make this insurance mandatory because the property itself serves as the collateral for the loan. This policy is a specialized financial safeguard designed to protect the physical shell of your house—the “bricks and mortar”—from catastrophic risks like fire, floods, earthquakes, and storms. From the bank’s perspective, if a natural disaster were to compromise the structural integrity of your home, the value of their collateral vanishes. This insurance ensures that funds are available to rebuild or repair the asset, safeguarding both your investment and the bank’s interest.

Understanding these requirements is crucial for accurate construction cost estimation and home buying budgets. Failing to account for this can lead to last-minute delays in loan disbursement or, worse, leave you unprotected during a claim. This comprehensive guide will navigate the nuances of building insurance for home loan India, comparing costs, coverage, and the IRDAI-mandated Bharat Griha Raksha policies to ensure your property remains a secure asset.

What is Building Insurance for Mortgage?

At its core, building insurance for mortgage is a structural insurance policy taken out on a property that has been financed through a loan. It is fundamentally different from a standard “home insurance” package that covers both the building and your personal belongings. When you have a mortgage, the primary focus is the “dwelling coverage” or the physical anatomy of the property. This includes the foundation, load-bearing walls, roof, floors, and permanent fixtures like concealed wiring and plumbing.

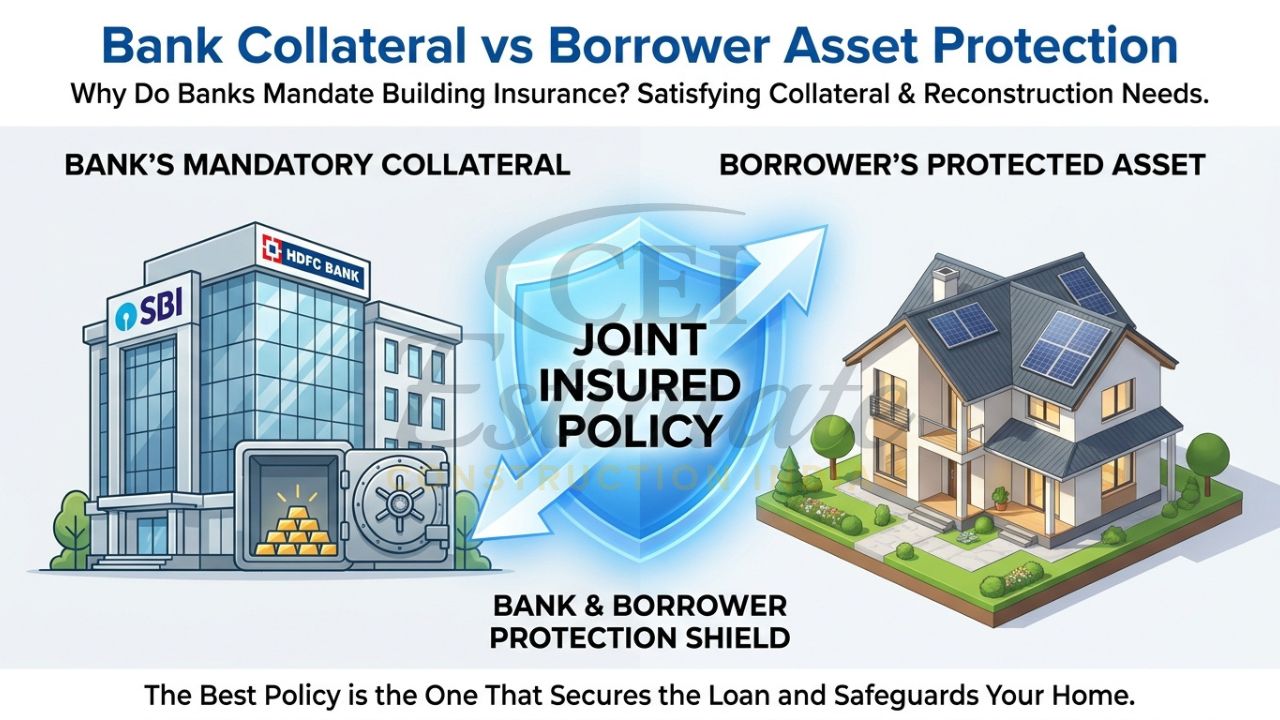

The most critical feature of a policy for building insurance for mortgage is the Loss Payee Clause. The policy is typically taken in the joint name of the borrower (you) and the lending institution (the bank). In the insurance world, this is known as an “agreed bank clause.” It signifies that the bank has a financial interest in the property. In the event of a total loss, the insurance payout is primarily used to settle the outstanding loan amount with the bank, with any remaining balance going to the homeowner. It is a policy designed to protect the “shell” of the building, ensuring that if the structure were to be leveled by a catastrophe, the capital investment is recovered.

Why Do Banks Mandate Building Insurance for Mortgage?

You might ask, “Why is the bank so concerned about my house being insured?” The answer lies in risk management and collateral security. When a bank lends you lakhs or crores of rupees to buy or build a home, they don’t actually own the money; they are investing it into your property as a secured asset.

- Protecting the Collateral: The property is the security against which the loan is granted. If an earthquake in Delhi-NCR or a flood in Uttar Pradesh destroys the structure, the bank’s security effectively disappears. Building insurance for mortgage ensures that the value of this collateral is preserved.

- Asset Preservation: Banks want to ensure that the funds are available to restore the home to its original state if damaged. This keeps the property’s market value intact, which is essential for the bank if they ever need to recover the loan through a sale.

- Legal and Regulatory Compliance: Under the Real Estate (Regulation and Development) Act (RERA) and various internal banking guidelines, lenders are encouraged to mitigate risk. In disaster-prone regions like North India, which sits on active seismic zones, having mortgage insurance for building is a prerequisite for financial stability.

- Borrower Protection: While it protects the bank, it also prevents you from being in a situation where you owe a massive loan for a house that no longer exists or is uninhabitable.

What Does Building Insurance for Mortgage Cover?

In 2026, the IRDAI has simplified the landscape through the Bharat Griha Raksha (BGR) policy. This is the standard product that every general insurance company in India must offer for residential properties. When you purchase building insurance for mortgage, the coverage typically includes:

- Fire and Explosion: Protection against accidental fires, gas cylinder explosions, and lightning strikes—a major risk in high-density Indian urban areas.

- Natural Calamities (Acts of God): This is vital for North India. It covers damage from floods, storms, cyclones, earthquakes, landslides, and rockslides.

- Man-Made Perils: Coverage against physical damage caused by riots, strikes, or acts of terrorism.

- Impact Damage: Damage caused by a vehicle crashing into the compound wall or a falling tree.

- Utility Infrastructure: Bursting or overflowing of water tanks, apparatus, and pipes, which can cause significant structural soil subsidence or wall damage.

- Additional Costs: Most BGR policies automatically include “Escalation” (increasing the sum insured by 10% annually to handle inflation) and coverage for architect/surveyor fees and debris removal costs (up to specified limits).

It is important to note that this policy covers permanent fixtures. For instance, in a modern Meerut villa, your built-in modular kitchen, bathroom fittings, and concealed electrical wiring are all covered as part of the “structure” because they cannot be removed without damaging the building.

Building Insurance vs Home Loan Life Insurance (Mortgage Protection Plan)

One of the most common points of confusion for Indian borrowers is the difference between “Building Insurance” and “Home Loan Insurance” (often called a Mortgage Protection Plan or Term Life Insurance). While both are often requested by banks, they serve completely different purposes.

| Feature | Building Insurance (Structure) | Home Loan Life Insurance (Mortgage Protection) |

|---|---|---|

| What it Protects | The physical structure and permanent fixtures of the property. | The life of the borrower to cover the loan liability. |

| Purpose | To rebuild/repair the house after physical damage. | To pay off the outstanding loan if the borrower passes away. |

| Primary Risk | Fire, Flood, Earthquake, Storms. | Death or critical illness of the primary borrower. |

| Mandatory Status | Almost always mandatory for the property structure. | Often requested but legally voluntary (though highly recommended). |

| Claim Payout | Used for reconstruction or repair costs. | Used to settle the outstanding bank debt. |

Understanding this distinction is vital for your project estimate. While building insurance for mortgage protects the asset, the life insurance policy protects your family from the debt.

Is Building Insurance Mandatory for All Home Loans in India?

From a strictly legal standpoint, there is no central “law” that makes building insurance mandatory for every citizen. However, the home loan insurance requirement India is dictated by the internal policies of lending institutions like SBI, HDFC, PNB, and LIC Housing Finance.

For these banks, insurance is a condition of the loan agreement. If you refuse to provide a building insurance policy, the bank has the right to withhold the loan or even purchase a policy on your behalf and debit the premium from your account.

For under-construction properties, the requirement shifts. Banks usually require a “Contractor’s All Risk” (CAR) or “Builder’s Risk” policy during the construction phase. This protects the materials and the unfinished structure. Once the construction is complete and you receive a completion certificate, the bank will require you to switch to a standard building insurance policy like Bharat Griha Raksha.

How Much Does Building Insurance for Mortgage Cost?

In 2026, building insurance remains one of the most affordable components of home ownership in India. The cost of building insurance for mortgaged property is calculated based on the “Reinstatement Value”—the cost to rebuild the structure at current material and labor rates—not the market value of the property (which includes land cost).

Typically, premiums range from 0.15% to 0.50% of the sum insured annually.

Sample Calculations for 2026:

- ₹40 Lakh Construction Cost: If you have a loan for a property where the reconstruction value is ₹40 lakhs, your annual premium would likely be between ₹6,000 and ₹12,000.

- ₹80 Lakh Construction Cost: For a larger home in a city like Meerut, the premium might range from ₹12,000 to ₹24,000 per year.

Factors affecting the cost include the location (high-risk seismic zones like Delhi-NCR attract slightly higher rates), the type of construction (RCC frames are cheaper to insure), and the policy tenure. Many banks allow you to pay a one-time premium for a long-term policy (e.g., 10–15 years) that aligns with your loan tenure, often at a discounted rate.

Step-by-Step Guide to Buying Building Insurance for Your Mortgage

Securing the right policy in 2026 is a streamlined process:

- Calculate the Reinstatement Value: Do not use the loan amount alone. Use the total carpet area multiplied by the current construction rate in your city (e.g., ₹2,500/sq. ft. in Noida).

- Verify Bank Requirements: Ask your lender for their specific “Agreed Bank Clause” wording.

- Compare Quotes: Use digital platforms like Policybazaar or go directly to insurers like ICICI Lombard or SBI General to find a BGR policy.

- Add the Bank as Loss Payee: Ensure the policy clearly mentions: “Lien in favor of [Bank Name]”.

- Submit the Policy: Provide the digital copy to your bank to finalize the loan disbursement.

Claims Process When You Have a Mortgaged Property

If your property suffers damage, the claims process involves three parties: you, the insurer, and the bank.

- Immediate Intimation: Inform the insurer within 24–48 hours.

- The Surveyor: An IRDAI-licensed surveyor will assess the damage. You must provide a defensible repair estimate (BOQ).

- The Bank’s Role: Because the bank is the loss payee, the claim check is often issued in the joint names of the borrower and the bank. For small repairs, the bank may “No Objection Certificate” (NOC) the funds to you. For major losses, the bank uses the funds to settle the loan first.

Why Construction Estimators and Home Buyers Must Plan for It?

As an expert at Construction Estimator India, I cannot stress enough that insurance is a vital “soft cost” in any project. For a construction estimator, including building insurance for mortgage as a line item in your Bill of Quantities (BOQ) ensures that the client is prepared for the total cost of ownership.

Whether you are building a new villa in Meerut or buying a flat in Delhi, factoring in these premiums prevents last-minute budget shocks. Accurate cost estimation isn’t just about cement and steel; it’s about the financial shell that protects them. For professional BOQ services that integrate all insurance and risk management costs, visit our website at Place Construction Estimator India.

Conclusion

In 2026, building insurance for mortgage is far more than a bank requirement; it is a fundamental pillar of financial security for every Indian homeowner. Whether you are navigating the high-seismic zones of Delhi-NCR or the flood-prone plains of Uttar Pradesh, this insurance ensures that your “dream home” doesn’t become a financial nightmare after a disaster. By understanding that banks require this to protect their collateral, and by choosing a standardized Bharat Griha Raksha policy, you can move forward with your home loan with confidence.

Don’t treat insurance as an afterthought. Arrange your building insurance early in the home loan process to ensure smooth disbursement. For accurate BOQ and construction cost estimation services that include detailed insurance projections, contact Construction Estimator India today. Let us help you build a future that is both beautiful and protected.

FAQ Section

What is building insurance for mortgage in India?

It is a structural insurance policy that covers the physical framework of a house (walls, roof, foundation) and is required by lenders to protect the collateral for a home loan.

Is building insurance mandatory for home loans?

Yes, most Indian banks and housing finance companies make it a mandatory condition for loan approval and disbursement.

What does building insurance for mortgage cover?

It typically covers fire, lightning, earthquake, floods, storms, and impact damage to the building structure.

How much does building insurance cost for a mortgaged property?

Premiums usually range from 0.15% to 0.50% of the reconstruction cost, costing approximately ₹3,000–₹8,000 annually for a ₹20 lakh structure.

Who is the loss payee in building insurance for mortgage?

The lending bank is the loss payee, meaning they have the first right to the insurance payout to settle the outstanding loan.

Can I use my existing policy for the mortgage?

Yes, provided it covers the structure adequately and you add the bank as a joint insured party with a proper “loss payee” clause.

What is the difference between building insurance and home loan protection plan?

Building insurance protects the physical house, while a home loan protection plan (life insurance) pays off the loan if the borrower dies.

How is sum insured decided for mortgage building insurance?

It should be based on the “Reinstatement Value” (construction cost per sq. ft. × area), though banks often accept the loan amount as a minimum.

What happens to insurance after the home loan is fully repaid?

Once the loan is settled, the bank’s name is removed from the policy. You can then continue the insurance in your own name or convert it into a comprehensive home insurance policy.

How to include building insurance cost in home construction estimates?

It should be listed as a “Fixed Soft Cost” or “Risk Management” line item in your BOQ, based on the projected reconstruction value of the project.

Learn more about related topics: