Imagine you are a resident in a high-rise luxury complex in Meerut or Greater Noida. After years of saving, you finally moved into your dream flat in 2026. One evening, an unusually heavy monsoon downpour causes a major structural leak in the common overhead water tank, leading to a short circuit that damages the entire lift system and the premium wooden flooring in the lobby. As an individual owner, you assume your “home insurance” covers it, but you soon realize your policy only covers your personal belongings. The Resident Welfare Association (RWA) is now faced with a 40-lakh repair bill because they neglected a comprehensive building insurance for apartment policy. This scenario is a frequent financial nightmare for thousands of flat owners across North India.

Understanding building insurance for apartment (also known as apartment building insurance or dwelling insurance) is uniquely complex compared to independent houses. In a multi-story setup, the building structure is a shared asset. While you own the air space inside your flat, the foundation, columns, external walls, and common facilities like gyms and lobbies are jointly held. Therefore, protecting these “immovable” parts requires a collective approach, typically managed by the RWA or the builder during the maintenance phase. In India, the IRDAI-mandated Bharat Griha Raksha for apartment has become the gold standard for such protection, offering a simplified and transparent way to secure your investment.

This guide explores the vital nuances of apartment building insurance India 2026, from coverage perils to the critical role of construction estimators in factoring these costs into new projects. Whether you are an RWA member looking to safeguard your society or a builder ensuring RERA compliance, this article provides the professional clarity needed to protect your residential assets.

What is Building Insurance for an Apartment?

In the Indian real estate context, building insurance for apartment refers to a specialized policy that covers the physical framework of the entire residential complex. This is strictly a “structure-only” or “structure plus common fixtures” policy. Unlike an individual home insurance plan that you might buy for your belongings, this insurance looks at the skeleton of the building. It focuses on the foundation, load-bearing walls, roof, floors, staircases, and the external facade.

A crucial distinction to understand is the “immovable” nature of the insured items. If you were to turn the entire apartment tower upside down and shake it, everything that stays attached—including the concealed plumbing, electrical wiring, lifts, transformer rooms, and built-in bathroom fittings—is what the building insurance protects. It treats the complex as a single unit of risk. While the RWA generally insures the common areas and the overall shell, the policy can be designed to include the structural elements of individual units as well. This prevents a situation where a fire in one flat causes structural damage to the neighbor’s floor, leaving a “coverage gap” between individual policies.

Why Apartment Owners and RWAs Need Building Insurance?

As construction costs in India soar in 2026, the financial stakes for apartment communities have never been higher. A single seismic event in the Delhi-NCR region or a localized fire can cause damage worth crores. Here is why securing building insurance for apartment in India is non-negotiable:

- Collective Risk Management: In an apartment, your safety is dependent on your neighbor’s. A kitchen fire in Flat 402 can compromise the structural slab of Flat 502. A master building policy ensures that the entire structure is restored regardless of where the damage originated.

- RERA and Legal Obligations: Under the Real Estate (Regulation and Development) Act, builders are often responsible for structural defects and must maintain insurance for the project until it is officially handed over to the RWA. Post-handover, the RWA assumes the legal duty to protect the shared assets of the members.

- Bank and Loan Requirements: If you are a flat buyer, your home loan provider (like SBI, HDFC, or ICICI) will insist on flat insurance for structure. Often, they accept the RWA’s master policy as proof of coverage, which is more cost-effective for you.

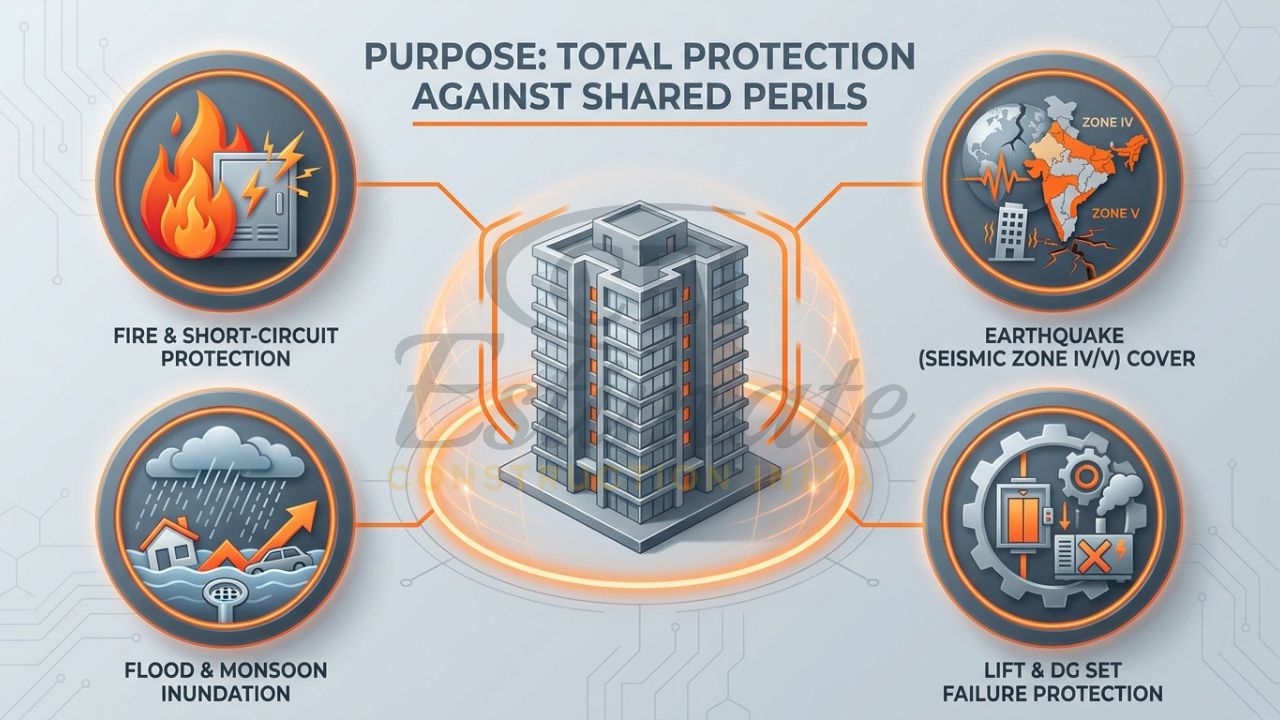

- Protection Against Natural Calamities: North India, particularly Uttar Pradesh and Delhi, sits in high-seismic zones (Zone IV and V). Apartment building insurance India 2026 provides the necessary funds for retrofitting or rebuilding after an earthquake or flood, which would be impossible for an RWA to fund via mere maintenance collections.

What Does Building Insurance for Apartment Cover?

The Bharat Griha Raksha for apartment framework provides a robust safety net. When you or your RWA purchases this policy, it typically covers a wide array of perils that could threaten the integrity of the building.

- Natural Disasters: Full protection against earthquakes, floods, inundation, storms, cyclones, typhoons, and landslides. This is vital for cities like Meerut that face erratic monsoon patterns.

- Fire and Accidental Hazards: Coverage for damage caused by accidental fires, lightning, or domestic gas cylinder explosions in common kitchens or individual units.

- Common Area Infrastructure: This is the most significant part of the policy. It covers the lifts, escalators, water pumps, transformers, diesel generators (DGs), swimming pool structures, and compound walls.

- Impact and Man-made Damage: If a vehicle crashes into the boundary wall or if damage occurs due to riots, strikes, or malicious acts by third parties.

- Bursting of Pipes: Covers the structural damage (though often not the pipe repair itself) caused by the bursting or overflowing of water tanks and common plumbing shafts.

- In-built Professional Fees: Most policies in 2026 automatically include coverage for architect fees (up to 5% of the claim) and debris removal (up to 2% of the claim), allowing the RWA to hire experts for reconstruction without extra levies on residents.

Building Insurance vs Contents Insurance in Apartments

One of the most common points of confusion for residents in India is the difference between apartment building and contents insurance. While they are often sold as a package, they serve two very different purposes.

| Feature | Building Insurance (Structure) | Contents Insurance (Possessions) |

|---|---|---|

| Primary Focus | The physical shell, foundation, and common areas. | Movable items inside the flat. |

| What is Covered? | Walls, roof, lifts, wiring, plumbing, and fixtures. | Furniture, TV, AC, clothes, jewelry, and laptops. |

| Who Typically Buys It? | The RWA or the Builder (Master Policy). | The Individual Flat Owner or Tenant. |

| Sum Insured Basis | Reinstatement Value (Current construction cost). | Market Value or Replacement Value. |

| Example Claim | Repairing a cracked pillar after an earthquake. | Replacing a sofa damaged by a leaking ceiling. |

| Policy Term | Long-term (up to 10-15 years) or Annual. | Usually renewed annually. |

In a professional setup, the RWA secures the “shell,” while you, as the owner, focus on the “lifestyle” items inside. At Construction Estimator India, we recommend that every flat owner confirms the existence of the RWA master policy before buying their individual contents cover.

Who Should Buy Building Insurance for Apartment – RWA or Individual Owner?

In the Indian residential landscape, the most efficient approach is the RWA building insurance model. Here, the association takes a “Master Policy” for the entire survey number or project. This is significantly cheaper than 100 individual owners buying separate structural policies.

- Why the RWA should buy: It ensures there are no gaps in coverage. If every owner buys their own structural insurance, a few might let their policies lapse. If a fire then weakens the building’s central core, the RWA would struggle to coordinate multiple insurers for a repair. A single master policy covers the “unity of the structure.”

- Why the Individual should buy: You should only buy structural insurance if your RWA does not have a master policy, or if you have made extensive structural modifications (with approval) that increase the value of your specific unit beyond the standard reconstruction cost. Generally, your focus should be on insurance for apartment owners in India that covers your internal renovations and belongings.

How Much Does Building Insurance for Apartment Cost in India?

The cost of building insurance for apartment complexes in 2026 is surprisingly low when shared among residents. Premiums are calculated based on the “Reinstatement Value”—the cost to rebuild the structure using current material and labor rates—excluding the land value.

- Premium Rates: Generally range from 0.15% to 0.45% of the total reconstruction cost.

- Factors: High-rise buildings (above 15 floors) may have slightly higher rates due to fire risk, while buildings with modern firefighting systems get discounts.

- Sample Cost for a 50-Flat Complex: If the reconstruction value of the entire building is ₹20 Crore, the annual premium might be approximately ₹40,000 to ₹60,000. When divided, each owner pays only ₹800 to ₹1,200 per year—less than the cost of a single dinner outing.

- Sample Cost for a 100-Flat Complex: For a ₹50 Crore valuation, the premium might be ₹1 Lakh to ₹1.5 Lakhs annually.

For estimators, these figures are critical line items in the Bill of Quantities (BOQ). Factoring these into the annual maintenance charges (AMC) projection during the project planning phase ensures the RWA remains solvent and the building remains protected from day one.

Step-by-Step Guide to Buying Building Insurance for Apartment

If you are a member of an RWA or a proactive owner, follow this process to secure your community:

- Determine Reinstatement Value: Do not use the market value. Use the total built-up area multiplied by the current construction rate (e.g., ₹2,500/sq. ft. in Meerut). Contact Construction Estimator India for a professional valuation.

- Pass an RWA Resolution: Ensure the majority of owners agree to the master policy as part of the society’s bylaws.

- Compare National Insurers: Get quotes from HDFC Ergo, ICICI Lombard, or SBI General. Look specifically for the “Bharat Griha Raksha” wording.

- Select Necessary Add-ons: Consider “Loss of Rent” for owners if the building becomes uninhabitable, or “Public Liability” to cover injuries to visitors on the premises.

- Review Documentation: Ensure the Occupancy Certificate (OC) and sanctioned building plans are ready, as these are required during the underwriting process.

Claims Process for Apartment Building Insurance

When a disaster strikes the structure, the RWA must act as the primary point of contact.

- Notification: Inform the insurer within 24 hours of the fire, flood, or earthquake.

- Surveyor Inspection: A licensed surveyor will visit to assess common areas and affected flats. It is vital to have the original construction BOQ and recent repair invoices ready.

- Role of Individual Owners: Owners must provide access to their flats for the surveyor but should coordinate their structural claims through the RWA to ensure the building is repaired as a whole.

- Documentation: Keep photographs of the damage, the FIR (if it’s a fire or riot), and a detailed repair estimate from a qualified civil engineer.

Why Estimators and Builders Must Include It in Apartment Projects?

At Construction Estimator India, we believe that building insurance for apartment is a foundational component of project risk management. For builders, including the first three to five years of insurance premiums in the project’s soft costs ensures RERA compliance and builds trust with buyers.

For construction estimators, adding insurance as a line item in the BOQ for a new apartment project allows the future RWA to understand the true “Total Cost of Ownership.” It prevents “budget shocks” where a new society finds itself unprotected because the insurance cost was never factored into the initial maintenance fund. Accurate estimation ensures that the sum insured reflects the actual cost of TMT bars, cement, and labor in the 2026 market, avoiding the “under-insurance” traps that lead to rejected claims.

Conclusion

Securing a building insurance for apartment policy is the most responsible action an RWA or a builder can take in 2026. In the dense urban landscapes of Uttar Pradesh and the Delhi-NCR, where structural risks are shared, a master policy is the only way to ensure total financial peace of mind. By focusing on the reinstatement value and choosing the standardized Bharat Griha Raksha framework, communities can safeguard their multi-crore investments against the unpredictable.

Don’t leave your structural safety to chance. Whether you are an owner in Meerut or a developer in Noida, make insurance a priority. For professional BOQ preparation, accurate construction cost estimation, and insurance-inclusive project planning, contact Construction Estimator India today. Let us help you build and protect a foundation that lasts.

FAQ Section

What is building insurance for apartment in India?

It is a policy that covers the physical structure of an apartment building, including common areas, lifts, and foundation, against perils like fire, earthquake, and flood.

Who should buy building insurance — RWA or individual flat owner?

The RWA should ideally buy a “Master Policy” for the entire building structure, while individual owners should focus on contents insurance for their personal belongings.

Does Bharat Griha Raksha cover apartments?

Yes, Bharat Griha Raksha is the standard IRDAI policy designed for residential properties, including multi-story apartment complexes and independent flats.

What is covered under apartment building insurance?

It covers fire, natural disasters (earthquake, flood), bursting of water tanks, impact damage, and common infrastructure like lobbies and lifts.

How much does building insurance cost for an apartment complex?

Annual premiums typically range from 0.15% to 0.45% of the total reconstruction cost, which usually amounts to a very small fee per flat owner.

Is building insurance mandatory for apartments?

While not legally mandatory for all, it is required by banks for home loans and often by RERA for developers during the maintenance period.

What is the difference between building insurance and contents insurance in flats?

Building insurance covers the immovable structure (walls, pipes, lifts), whereas contents insurance covers movable items (furniture, electronics, jewelry).

How is sum insured calculated for apartment buildings?

It is calculated as: Total Built-up Area × Current Cost of Construction per sq. ft. It excludes the market value of the land.

Can individual apartment owners buy separate building insurance?

Yes, but it is more expensive and less efficient than a collective RWA master policy. It is usually only done if the RWA fails to provide coverage.

How to include building insurance cost in new apartment project estimates?

Estimators should include it as a “Soft Cost” or “Preliminary” line item in the BOQ, based on a 1-year or 5-year premium projection using current market rates.

Suggested Related Article: