Imagine you are a landlord in Meerut, Uttar Pradesh, owning a beautiful three-story independent floor that you have rented out to a young family. Your investment of ₹80 lakhs feels secure until a particularly savage monsoon hits Western UP, triggering localized flooding and an electrical short-circuit in the building’s main panel. Within hours, the structural beams are damaged, and the foundation shows signs of soil subsidence. You suddenly realize that while your tenant has “renters insurance” for their furniture, you have no coverage for the structural shell of the building itself. This scenario is a financial nightmare that highlights why securing building insurance for a rental property is a non-negotiable step for every property owner in India today.

The Indian rental market is witnessing unprecedented growth in 2026, especially in tier-2 cities and the Delhi-NCR region. However, rental properties face unique risks including higher wear and tear, potential tenant negligence, and third-party liability claims. For a landlord, your primary concern is protecting the “bones” of the house—the walls, roof, foundation, and permanent fixtures like plumbing and electrical wiring. This specialized coverage, often referred to as landlord building insurance India, ensures that your capital investment remains protected against natural calamities and man-made perils.

Even if your property is currently occupied by a tenant, you must take the lead in securing building insurance for rental property in India. Under the standard Bharat Griha Raksha for rental property framework mandated by IRDAI, you can protect your structure regardless of who resides inside. This guide will explore everything from coverage details and costs to why construction estimators must include insurance as a line item in every Bill of Quantities (BOQ). Whether you are a seasoned investor or a first-time landlord, understanding these nuances is key to your long-term financial stability.

What is Building Insurance for a Rental Property?

In the Indian insurance landscape of 2026, building insurance for a rental property is defined as a specialized policy that protects the immovable and fixed components of a building on your land. It is fundamentally different from a standard “home insurance” package that homeowners buy for self-occupied properties because it focuses strictly on the landlord’s asset—the structure itself—rather than the personal belongings of the person living there.

If you were to take your rental house, turn it upside down, and shake it, everything that stays attached is covered by this policy. This includes:

- The foundation and plinth area.

- Load-bearing walls and the roofing system.

- Permanent internal wiring and concealed plumbing networks.

- Fixed installations such as built-in kitchen cabinets, bathroom sanitary ware, and tiled flooring.

It is crucial to understand the difference between building and contents insurance for rental units. While building insurance protects the “shell,” contents insurance covers movable items like electronics, furniture, and jewelry. For a rental property, the landlord should secure the building cover, whereas the tenant should ideally purchase their own contents cover to protect their personal possessions. This clear demarcation prevents disputes during the claims process and ensures that neither party is left financially vulnerable.

Why Landlords Need Building Insurance for Rental Properties?

As a property owner in India, you bear the ultimate financial responsibility for the structural integrity of your asset. Relying on a tenant to maintain the property or assuming “nothing will happen” is a dangerous gamble. Here are the primary reasons why landlord building insurance India is essential:

- Protection Against Natural Calamities: India is prone to diverse climatic risks. From the seismic tremors in Delhi-NCR (Zone IV/V) to the severe monsoons and flooding in Uttar Pradesh, your property’s structure is constantly at risk from “Acts of God.”

- Coverage for Tenant-Induced Perils: While a tenant may be careful, accidents like a gas cylinder explosion or a localized fire due to an unattended appliance can devastate the structural beams of your house.

- Mandatory Bank Requirements: If you have an active home loan on your rental property, banks like SBI, HDFC, or ICICI will mandate a building structure policy to protect their collateral.

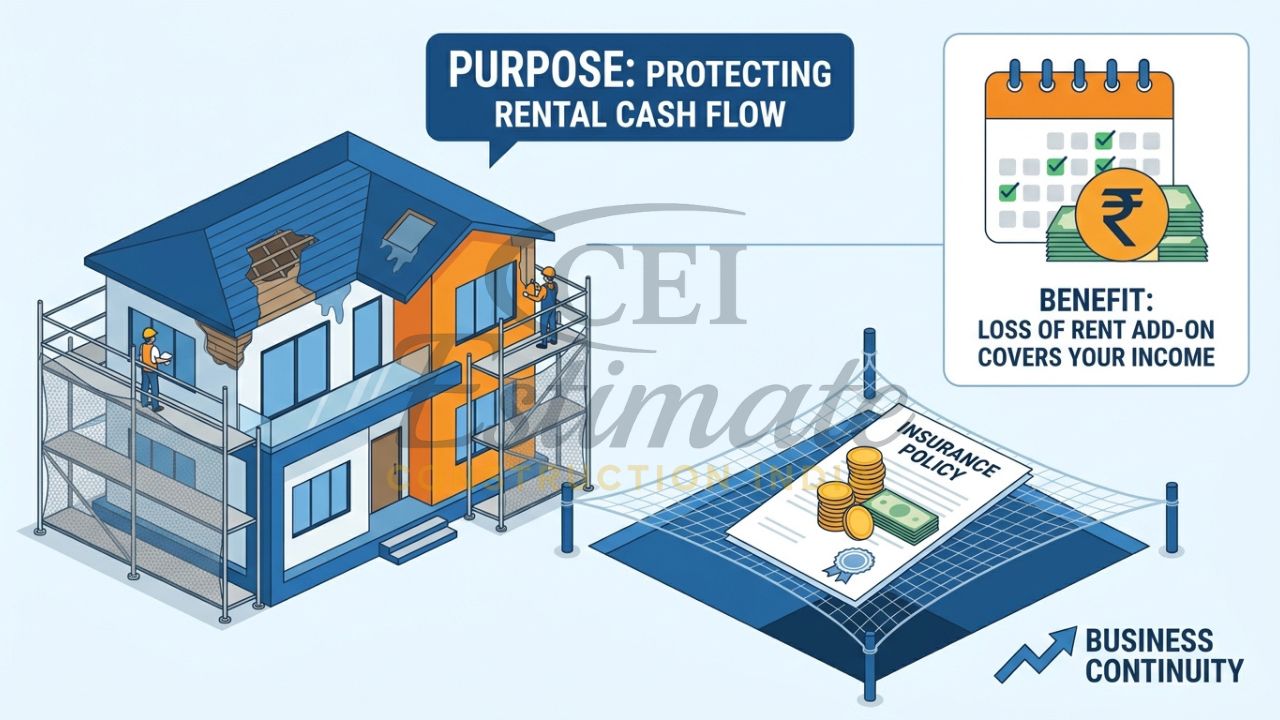

- Protection of Rental Income: Modern policies like the Bharat Griha Raksha offer a “Loss of Rent” add-on. If your property becomes uninhabitable due to a covered peril (like a major fire), the insurer compensates you for the lost rent during the repair period.

- Third-Party Liability: If a part of your building (like a balcony railing) collapses and injures a tenant or a visitor, a comprehensive landlord policy can cover the resulting legal and medical liabilities.

What Does Building Insurance for a Rental Property Cover?

Under the standardized Bharat Griha Raksha for rental property guidelines of 2026, landlords receive comprehensive protection against a wide array of “Insured Perils.” When you invest in home building insurance for rented house structures, you are typically covered for:

- Fire and Explosions: Includes accidental fire, lightning strikes, and domestic gas explosions.

- Climate-Related Hazards: Protection against floods, inundation, storms, cyclones, and tempests—critical for properties in low-lying areas of Meerut or Noida.

- Geological Risks: Coverage for damage caused by earthquakes, landslides, and rockslides.

- Man-Made Perils: Damage resulting from riots, strikes, malicious acts, or acts of terrorism.

- Impact Damage: If a vehicle crashes into your boundary wall or a falling tree damages the roof of your rental unit.

- Utility Failures: Damage caused by the bursting or overflowing of water tanks and pipes.

Furthermore, building insurance for a rental property provides automatic coverage for “Additional Structures” on the premises, such as compound walls, garages, servant quarters, and gates. In 2026, policies also include “In-built Benefits” like:

- Architect and Surveyor Fees: Up to 5% of the claim amount to hire professionals for reconstruction plans.

- Debris Removal: Up to 2% of the claim amount to clear the site after a disaster.

- Alternative Accommodation: If the tenant has to move out temporarily due to structural repairs, the insurer may cover the cost of their temporary stay or the lost rent for the landlord.

Building Insurance vs Contents Insurance for Rental Properties

To effectively manage your rental investment, you must understand who is responsible for what. The following table highlights the key distinctions between the two.

| Feature | Building Insurance (Landlord) | Contents Insurance (Tenant) |

|---|---|---|

| Primary Protection | Foundation, walls, roof, fixed wiring, and pipes. | Furniture, electronics, clothes, and appliances. |

| Who Buys It? | The Property Owner / Landlord. | The Tenant or Resident. |

| Sum Insured Basis | Reinstatement Value (Cost to rebuild). | Market Value (Depreciated value of items). |

| Typical Claim | Cracks in walls due to an earthquake. | Laptop stolen during a break-in. |

| Theft Coverage | Covers damage to doors/windows during a break-in. | Covers the value of the stolen items. |

| Add-ons | Loss of rent, debris removal. | Jewelry cover, breakdown of appliances. |

Landlords should always secure the building cover to protect their capital, while encouraging tenants to buy a contents-only policy for their movable possessions.

Is Building Insurance Mandatory for Rental Properties in India?

From a legal standpoint, the Indian government does not mandate that every landlord must have building insurance for a rental property. However, in the 2026 real estate market, it is considered a “de facto” requirement in several critical scenarios:

- Mortgaged Properties: If you have a home loan from a bank or NBFC, they will legally require you to maintain a building structure policy throughout the loan tenure to protect their interest in the property.

- RERA Compliance: Under the Real Estate (Regulation and Development) Act, developers and builders are often required to maintain insurance for the structure and title of the project until it is officially handed over to the residents’ association or owners.

- Lease Agreements: Many high-end corporate lease agreements in Delhi-NCR or Gurgaon now include clauses requiring the landlord to provide proof of structural insurance to ensure the tenant’s safety and business continuity.

Voluntarily purchasing insurance for landlord rental property 2026 is the hallmark of a professional investor. It prevents a single disaster from turning your profitable rental asset into a massive financial liability.

How Much Does Building Insurance for a Rental Property Cost in India?

The cost of building insurance for rental property is surprisingly affordable in 2026, often representing less than 0.1% of the property’s market value. Importantly, the premium is calculated based on the “Reinstatement Value”—the actual cost to rebuild the structure—rather than the market value (which includes land cost).

In 2026, the annual premium generally ranges from 0.15% to 0.50% of the reconstruction cost. Factors affecting the price include:

- Location: Properties in high-risk seismic zones (Delhi-NCR) or flood zones (Western UP) may attract slightly higher premiums.

- Construction Quality: RCC (Reinforced Cement Concrete) structures are cheaper to insure than older load-bearing brick buildings.

- Policy Tenure: Multi-year policies (up to 10 years) often come with significant discounts compared to annual renewals.

Examples of Insurance Costs (Estimated for 2026):

- ₹30 Lakh Rental Property: Annual premium approx. ₹1,800 to ₹4,500.

- ₹80 Lakh Rental Property: Annual premium approx. ₹4,800 to ₹12,000.

For accurate investment costing, you must link your sum insured to a professional Bill of Quantities (BOQ). If your construction estimator projects a reconstruction cost of ₹2,500 per sq. ft. for your 2,000 sq. ft. property, your sum insured should be at least ₹50 Lakhs to avoid “under-insurance.”

Step-by-Step Guide to Buying Building Insurance for Your Rental Property

Buying building insurance for a rental property in 2026 is a streamlined, digital process. Follow these steps for the best protection:

- Calculate the Reinstatement Value: Do not use the market price. Multiply your property’s carpet area by the current local construction rate (e.g., ₹2,200/sq. ft. in Meerut).

- Compare Quotes: Use portals like Policybazaar or visit direct insurer websites like ICICI Lombard, HDFC Ergo, or SBI General to compare Bharat Griha Raksha for rental property plans.

- Choose Essential Add-ons: Ensure you select “Loss of Rent” (to protect your income) and “Escalation Cover” (to account for rising material costs like cement and steel).

- Identify the Occupancy: Clearly state that the property is “Tenant-Occupied” to the insurer to avoid issues during a claim.

- Documentation: Keep your property tax receipts, sale deed, and the latest floor plan ready. Most 2026 policies do not require physical inspection for standard residential buildings.

Claims Process and Tips for Smooth Settlement

If your rental property suffers damage, you must act swiftly to protect your rights:

- Immediate Intimation: Call your insurer or use their mobile app within 24 hours of the incident.

- Document Everything: Take high-resolution photos and videos of the structural damage before any repairs begin.

- The Surveyor’s Visit: An IRDAI-licensed surveyor will visit the site. Provide them with a professional BOQ for repairs using current market rates.

- Avoid Repairs: Do not start permanent repairs (except for emergency mitigation) until the surveyor has inspected the damage.

Why Estimators and Property Owners Should Factor It In?

For professional construction estimators and rental property investors, insurance is not just an “extra”; it is a vital component of risk management. Including the cost of building insurance for a rental property in your property valuation or renovation estimates ensures that the project remains financially viable even if a disaster occurs.

At Construction Estimator India, we specialize in providing detailed BOQs and cost estimations that include integrated insurance premium analysis. This level of planning demonstrates professionalism and ensures that your rental asset is protected from the moment the foundation is poured to the day the first tenant moves in.

Conclusion

Securing building insurance for a rental property is the most cost-effective way to safeguard your real estate investment in India. From the unpredictable monsoons of Uttar Pradesh to the seismic risks of Delhi-NCR, a robust policy ensures that your “source of income” doesn’t become a “source of debt.” By focusing on the reinstatement value and choosing the right add-ons under the Bharat Griha Raksha framework, you can build and rent with total confidence.

Don’t leave your property’s future to chance. Review your current coverage today and ensure it reflects 2026’s construction rates. For expert construction cost estimation and professional BOQ services that protect your rental projects, contact Construction Estimator India.

FAQ Section

What is building insurance for a rental property?

It is a policy that covers the physical structure (walls, roof, foundation) and permanent fixtures of a property owned by a landlord and rented to a tenant.

Does building insurance cover damage caused by tenants?

It typically covers accidental damage (like a fire or explosion caused by a tenant), but intentional “malicious damage” by the tenant may require a specific add-on.

Is building insurance mandatory for rented houses in India?

It is not legally mandatory by law, but it is almost always required by banks if there is an active home loan on the property.

What is the difference between building insurance and contents insurance for rental property?

Building insurance covers the immovable structure (landlord’s asset), while contents insurance covers movable items like furniture and electronics (usually the tenant’s asset).

How much does building insurance cost for a rental property?

Annual premiums are very affordable, generally ranging from 0.15% to 0.50% of the reconstruction cost (approx. ₹2,000–₹6,000 for a ₹40L structure).

Can I buy building insurance if the property is rented out?

Yes. You simply need to inform the insurer that the property is “Tenant Occupied” during the purchase process.

Does Bharat Griha Raksha cover rental properties?

Yes, Bharat Griha Raksha is the standard IRDAI policy that covers residential structures in India, whether self-occupied or rented.

What add-ons are useful for landlords?

“Loss of Rent” (covers lost income), “Escalation Cover” (accounts for inflation in material costs), and “Debris Removal” are highly recommended for landlords.

Who should buy contents insurance — landlord or tenant?

The tenant should buy contents insurance to protect their own belongings, while the landlord buys building insurance for the structure.

How to include building insurance cost in property investment calculations?

It should be added as a “Fixed Soft Cost” or an annual overhead in your ROI calculations, based on the reconstruction value provided in your BOQ.

Learn more about related topics: