Imagine you have just completed your dream home in Meerut, Uttar Pradesh, after months of meticulous planning and a significant financial investment. As you sit down to protect this massive asset, you find yourself staring at various policy options and confusing technical terms. You might hear insurance experts or global property advisors discuss DP1, DP2, and DP3 forms, leaving you wondering which one offers better protection for your new house or apartment. Understanding what is DP1, DP2, and DP3 in insurance is critical for any homeowner, landlord, or construction estimator who wants to ensure their property isn’t just a structure, but a financially secure haven.

In the world of dwelling property insurance India, these three categories—DP1, DP2, and DP3—define the scope of risk your insurer is willing to take on. “DP” stands for Dwelling Property, and the numbers represent the “form” or level of coverage. DP1 is the Basic Form, offering very limited named peril protection. DP2 is the Broad Form, which expands the list of covered risks. DP3 is the Special Form, often considered the gold standard as it provides “open peril” or all-risk protection for the building structure.

While the Indian market has largely moved toward the standardized Bharat Griha Raksha (BGR) policy, the concepts of DP1, DP2, and DP3 remain the foundation of how dwelling insurance is structured globally and how custom commercial or high-value residential policies are still designed in 2026. This guide will break down these terms, compare their features, and help you integrate these protection levels into your construction cost estimates or Bill of Quantities (BOQ).

What Do DP1, DP2, and DP3 Mean in Insurance?

When you ask what is DP1, DP2, and DP3 in insurance, you are essentially asking about the “menu” of risks your policy covers. These are standardized forms used to determine the breadth of a dwelling property insurance policy. Unlike traditional homeowners’ insurance which often bundles structure and liability, dwelling property (DP) forms focus primarily on the physical structure itself—making them ideal for rental property investors or landlords in growing tier-2 cities.

The primary difference between these forms lies in whether they are “Named Peril” or “Open Peril” policies. A named peril policy only covers events specifically listed in the document (like fire or wind). If a risk isn’t listed, it isn’t covered. An open peril policy, conversely, covers everything except what is explicitly excluded. DP1 and DP2 are named peril forms, while DP3 is an open peril form for the structure. Understanding these distinctions is the first step toward accurate risk assessment for any construction project or existing asset.

DP1 Insurance – Basic Form (Named Perils)

DP1 insurance is the most fundamental and restrictive type of dwelling property insurance India. As a “Basic Form,” it operates strictly on a named peril basis. This means the policy will only pay out if your home is damaged by a small, specific list of events. Typically, a standard DP1 policy covers:

- Fire and Lightning

- Internal Explosion

Many homeowners choose to add “Extended Coverage” to a DP1 policy, which might then include windstorms, civil unrest, or smoke. However, its biggest limitation is how it pays out. Most DP1 policies use “Actual Cash Value” (ACV) for claims. This means the insurer subtracts depreciation from your payout. If your 15-year-old roof in Meerut is destroyed, you won’t get enough money to buy a brand-new one; you’ll get the value of a 15-year-old roof.

DP1 is best suited for vacant properties, storage buildings, or budget-conscious landlords who are willing to self-insure against minor risks. For a new build in Delhi-NCR, DP1 is generally considered inadequate because it leaves the owner exposed to too many common hazards, such as pipe bursts or falling objects.

DP2 Insurance – Broad Form (Expanded Named Perils)

DP2 is known as the “Broad Form” because it significantly expands the list of named perils compared to DP1. It is a middle-ground solution for those who want better protection than a basic policy but aren’t ready for the premium of an all-risk plan. In addition to everything covered in DP1, a DP2 policy typically includes:

- Falling Objects: Damage from trees or debris.

- Weight of Ice or Snow: Relevant for colder climates or high-altitude regions.

- Accidental Discharge of Water: Coverage for sudden plumbing leaks (though often excluding the repair of the pipe itself).

- Cracking or Bulging: Structural damage to pipes or steam systems.

- Freezing: Damage to plumbing caused by extreme cold.

A major advantage of DP2 over DP1 is the “Replacement Cost” feature for the dwelling. If your property is damaged by a covered peril, the insurer pays to rebuild it at current material and labor rates without deducting depreciation, provided you are properly insured. For construction estimators, this level of coverage is easier to align with a modern BOQ, as it mirrors the actual reinstatement value of the building.

DP3 Insurance – Special Form (Open Perils / All-Risk)

When people ask what is DP1, DP2, and DP3 in insurance to find the “best” option, the answer is almost always DP3. DP3 is the “Special Form” and is the most comprehensive dwelling insurance available. It is an “Open Peril” policy for the structure, meaning it covers every possible source of damage unless it is specifically listed as an exclusion (like war, nuclear hazard, or intentional neglect).

Key features that make DP3 the preferred choice for premium villas and high-end apartments include:

- Comprehensive Coverage: It protects against “unknown” risks that a named peril policy would miss.

- Replacement Cost Basis: Like DP2, it pays the full cost to repair or replace the structure based on current 2026 construction rates.

- Landlord-Friendly: DP3 often includes “Loss of Rent” coverage, which compensates the owner if the property becomes uninhabitable due to a covered loss.

In the Indian context, the Bharat Griha Raksha (BGR) policy shares many characteristics with DP3, particularly its inclusion of natural calamities like earthquakes and floods as standard features. For a serious property investor in Noida or a homeowner building a luxury residence, DP3-level protection is the only way to truly safeguard the massive capital investment.

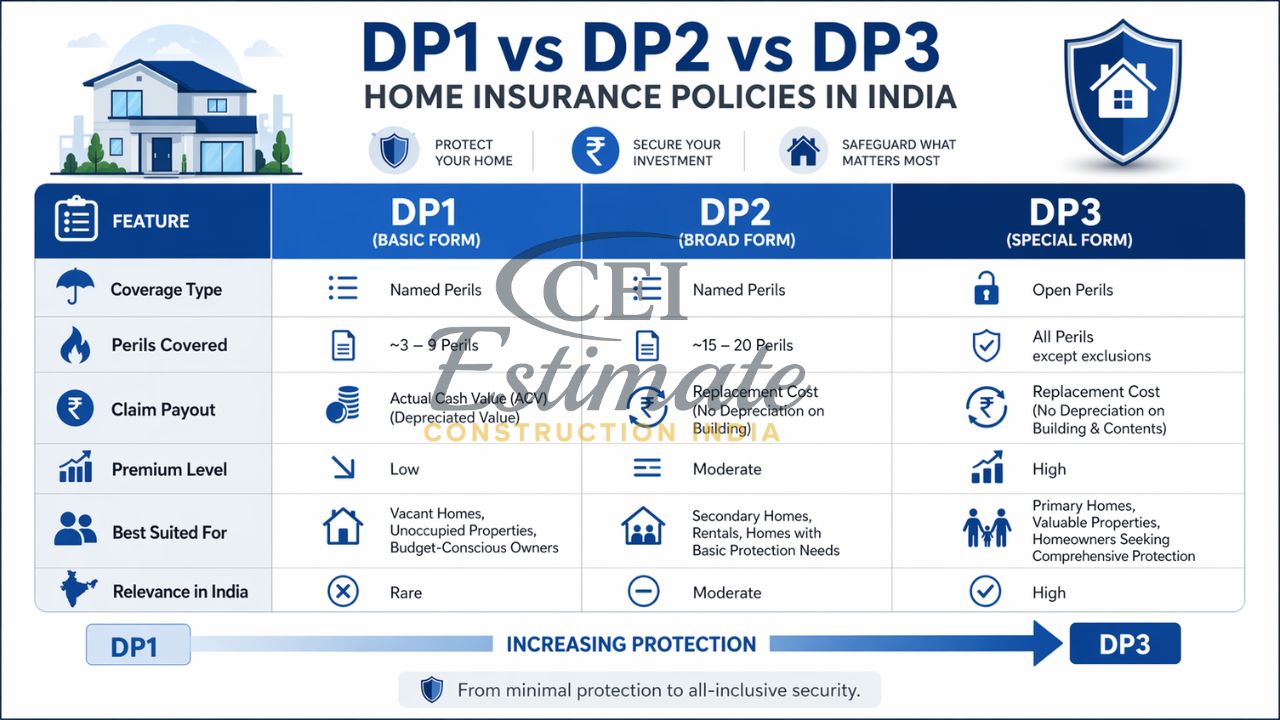

DP1 vs DP2 vs DP3 – Detailed Comparison

To choose the right home insurance coverage types India, you need to see how these forms stack up side-by-side.

| Feature | DP1 (Basic Form) | DP2 (Broad Form) | DP3 (Special Form) |

|---|---|---|---|

| Coverage Type | Named Perils | Named Perils | Open Perils (All-Risk) |

| Perils Covered | ~3 to 9 (Limited) | ~15 to 20 (Broad) | All except Exclusions |

| Claim Payout | Actual Cash Value (ACV) | Replacement Cost | Replacement Cost |

| Premium Level | Lowest | Moderate | Highest |

| Best Suited For | Vacant/Low-value homes | Budget-conscious owners | Primary homes & Rentals |

| Relevance in India | Rare (Specialty only) | Moderate (Standard) | High (BGR Benchmark) |

As shown, the transition from DP1 to DP3 represents a shift from “minimalist” protection to “all-inclusive” security. While DP1 might save you a few thousand rupees in annual premiums, the potential out-of-pocket cost for a non-covered event could be catastrophic.

How DP1, DP2, DP3 Relate to Home Insurance in India?

In 2026, the Indian insurance landscape is dominated by the Bharat Griha Raksha (BGR) policy, mandated by the IRDAI. If you are looking for DP1 DP2 DP3 insurance India, you won’t usually find these exact labels on a policy from ICICI Lombard or HDFC ERGO. Instead, you will find BGR, which acts as a “hybrid” that leans heavily toward the DP3 philosophy.

BGR provides standardized, comprehensive coverage for building structures, including automatic contents cover up to ₹10 lakh. It covers fire, natural disasters, and malicious damage, much like a Broad or Special form policy. However, for specialized commercial dwellings or high-value estates that exceed the standard BGR limits, insurers may still offer tailored policies that use the DP1/DP2/DP3 framework to define specific risk appetites. For construction estimators in cities like Meerut, understanding these global forms helps in explaining risk to international clients or those seeking “all-risk” project insurance.

Which One Should You Choose – DP1, DP2, or DP3?

The choice depends on your role and the property’s purpose:

- For Primary Homeowners: Always aim for DP3-level protection (or a robust BGR policy). Your home is likely your biggest asset; saving on premiums by choosing DP1 is a high-risk gamble.

- For Rental Investors/Landlords: DP3 is ideal because it covers the “open perils” and often includes loss of rent, ensuring your cash flow isn’t interrupted by a disaster.

- For Construction Estimators: When preparing a BOQ for a new build in Delhi-NCR, factor in the cost of a DP3-equivalent policy. This ensures the client understands the true cost of protecting their investment from day one.

- For Budget Properties: If the building is old, low-value, or slated for renovation, a DP1 or DP2 policy might suffice as a temporary financial stop-gap.

Cost Comparison and Impact on Your Budget

The cost of insurance in India is relatively affordable. For a structure with a reinstatement value of ₹50 Lakhs in 2026, the annual premiums might look like this:

- DP1 Equivalent: ₹1,500 – ₹2,500 (Basic fire/limited perils).

- DP2 Equivalent: ₹2,500 – ₹4,500 (Standard broad coverage).

- DP3 / BGR Equivalent: ₹4,500 – ₹7,500 (Comprehensive protection).

When building a new home, including these premiums in your construction estimate is a sign of professionalism. It shows the client that you are thinking about the “life-cycle” of the building, not just the handover. A small increase in the annual budget can prevent a total loss of the construction capital.

Step-by-Step Guide to Choosing the Right Home Insurance

- Calculate Reinstatement Value: Do not use market value. Multiply your built-up area by current construction rates (e.g., ₹2,200/sq. ft. in Meerut).

- Identify Local Risks: If you are in a seismic zone like Delhi-NCR, ensure earthquake cover is robust.

- Compare “Forms”: Check if the policy is “Named Peril” (DP1/DP2) or “Open Peril” (DP3).

- Review Exclusions: Even a DP3 policy has limits. Look for exclusions like “illegal construction” or “wear and tear”.

- Check Claim Settlement Ratios: Choose insurers like HDFC ERGO or ICICI Lombard with strong digital track records for 2026.

Conclusion

Understanding what is DP1, DP2, and DP3 in insurance is the key to moving beyond “basic” protection and securing your financial future. While DP1 offers a low-cost entry point, it often leaves you under-insured when you need help the most. For most homeowners in India today, the DP3-level coverage offered by the Bharat Griha Raksha framework is the most reliable way to ensure that fire, floods, or unforeseen calamities don’t turn your dream home into a financial liability.

Don’t leave your biggest investment to chance. Whether you are building a new villa in Noida or managing a rental portfolio in Meerut, choose a policy that reflects the true value of your structure. For professional help in determining your property’s reconstruction value or creating a detailed BOQ that accounts for essential insurance protections, contact Construction Estimator India today.

FAQ Section

What is the difference between DP1, DP2, and DP3 insurance?

The main difference is the breadth of coverage. DP1 covers only basic named perils (fire/lightning) and pays actual cash value. DP2 adds more named perils and pays replacement cost. DP3 is “open peril,” covering everything except specific exclusions, and is the most comprehensive.

Which is better — DP1, DP2, or DP3?

DP3 is generally considered better for homeowners and landlords because it offers the widest protection and pays claims on a replacement cost basis, meaning no deduction for depreciation.

Is DP3 available in India?

While the specific “DP3” label isn’t common, the Bharat Griha Raksha (BGR) policy in India provides very similar “all-risk” style protection for residential structures.

How does Bharat Griha Raksha compare to DP3?

BGR is similar to a DP3 policy because it covers a wide range of perils, including natural calamities, and automatically includes contents cover and escalation features.

What perils are covered under DP1 insurance?

Standard DP1 usually covers fire, lightning, and internal explosion. You can often add “Extended Coverage” for wind, hail, and civil unrest.

Why is DP3 more expensive than DP1 or DP2?

DP3 is more expensive because the insurer takes on significantly more risk by covering all perils except those specifically excluded. It also offers replacement cost payouts rather than depreciated values.

Can I buy DP3 for my apartment or rental property?

Yes, DP3-style coverage (like BGR) is highly recommended for rental properties because it provides the best structural protection and often includes “Loss of Rent” benefits.

Does a home loan require DP3 level insurance?

Most Indian banks like SBI or HDFC require at least a standard BGR or “Fire and Special Perils” policy, which typically meets DP2 or DP3 standards, to protect the collateral.

How does DP insurance affect my construction cost estimate?

A construction estimator should include the premium for DP3-level insurance in the BOQ to ensure the owner’s capital is protected against site disasters or structural failures after completion.