Imagine you are a flooring contractor in Meerut, working on a premium luxury villa project in Noida. You’ve just finished installing expensive Italian marble in the master bedroom when a helper accidentally knocks over a heavy tile-cutting machine, gouging the client’s custom mahogany wall paneling or shattering a nearby glass fixture. Or worse, a hidden water leak from an improperly sealed wet-room tile joint causes massive seepage in the flat below, leading to a structural repair bill of over ₹2 lakhs. Without the right insurance for flooring company operations, these common site disasters could wipe out your entire year’s profit in a single afternoon.

Flooring companies in 2026 face a unique set of daily risks that range from material wastage and tool theft to serious worker injuries and faulty workmanship claims. Whether you specialize in tiles, engineered wood, vinyl, or high-end marble, the nature of your work involves handling heavy, brittle materials and using specialized machinery in occupied or high-value environments. Many Indian flooring contractors under-insure themselves, wrongly assuming their client’s home insurance or their own vehicle policy covers their business activities. In reality, you need a specific portfolio of protection to safeguard your business, your team, and your reputation. This guide explores the essential types of insurance every flooring company needs, the realistic cost of insurance for flooring company 2026, and how to professionally factor these premiums into your job quotations and Bill of Quantities (BOQ).

Why Flooring Companies Need Specialized Insurance?

A flooring business is significantly different from general civil work because your activities are often the “finishing touch” in a high-value space. The risks are granular: a single slip-and-fall accident on a freshly polished floor can lead to a third-party liability claim. Using heavy-duty grinders and chemical adhesives presents fire and health hazards. Furthermore, high-end materials like TMT bars, imported wood, or granite are prime targets for site theft if left unsecured.

Beyond physical accidents, you are also at risk for “errors and omissions”. If your advice on sub-floor preparation is incorrect and the floor begins to buckle or lift six months later, the client can sue for financial losses. In cities like Ghaziabad or Gurgaon, where consumer awareness is high, legal recourse for perceived negligence is becoming a standard business challenge. Insurance acts as your financial safety harness, ensuring that an unforeseen site mishap doesn’t lead to personal bankruptcy.

1. Public Liability Insurance (Most Important for Flooring Companies)

If there is one policy that defines a professional trade business, it is public liability insurance for flooring company owners. This insurance is designed to protect you if your work causes accidental bodily injury or property damage to a third party—someone other than your employees.

For a flooring contractor, this covers scenarios like:

- Damaging a client’s furniture or plumbing while moving materials.

- A visitor tripping over your extension cords or tools on a busy site.

- Dust or chemical fumes from your polishing work causing damage to a neighbor’s expensive electronics.

In India, coverage limits for small contractors typically start at ₹5 lakhs and can go much higher for commercial projects. Reputable builders in the Delhi-NCR region often mandate a valid public liability certificate before allowing you to begin work on-site.

2. Professional Indemnity Insurance

While public liability covers physical damage, professional indemnity for flooring installers covers your “advice” and technical expertise. As flooring systems become more complex—incorporating underfloor heating, soundproofing, and epoxy resins—the risk of a design or advice error increases.

If you provide a technical recommendation for a specific adhesive for a factory floor in Meerut and the floor fails due to high-temperature exposure, leading to production downtime, the business can sue for financial loss. Professional indemnity protects you against claims of negligence, faulty workmanship, or professional errors that result in a client’s financial damage even without physical injury. It is essential for contractors offering design-build services or high-spec industrial flooring.

3. Workmen Compensation Insurance

If you employ helpers, junior installers, or daily-wage laborers, you have a statutory obligation under the Employees’ Compensation Act, 1923. Providing workmen compensation for flooring workers is a legal requirement in India. You are liable to pay for medical treatment and provide compensation if a worker suffers an injury, disability, or death while on duty.

Flooring work often involves risks like lifting heavy stone slabs (causing spinal issues), working on ladders for stair installations, and exposure to silica dust. Premium rates for Workmen Compensation Insurance (WCI) typically range from 0.5% to 2% of your total wage bill. For solo contractors, facilitating government-backed schemes like the Pradhan Mantri Suraksha Bima Yojana (PMSBY), which provides ₹2 lakh accidental cover for just ₹20 per year, is a great supplementary step.

4. Tools, Plant & Machinery Insurance

Your tools are your livelihood. Expensive equipment like heavy-duty floor polishers, laser levels, bridge saws, and industrial vacuums are major investments. Tools and equipment insurance for flooring company assets (often part of a Contractors Plant & Machinery or CPM policy) protects these items against theft, fire, and accidental damage on-site or during transit.

In North India, where site security varies, having your polishing kits and testing equipment insured ensures you can replace them quickly without a massive financial hit. Most policies require an updated inventory with purchase values to ensure a smooth claims process.

5. Other Important Insurance for Flooring Companies

To build a truly resilient flooring business insurance portfolio, consider these additional covers:

- CAR Insurance for Flooring Works: For larger projects, a Contractors All Risk policy covers the materials (tiles, wood) and the work-in-progress against natural disasters and accidents.

- Group Personal Accident: Provides 24/7 protection for your core team, covering accidents even outside of work hours.

- Vehicle Insurance: If you use a pickup or van for material delivery, ensure it has “commercial use” coverage.

- Stock Insurance: If you maintain a warehouse in Meerut or Delhi, this protects your inventory of stored tiles and marble against fire or water damage.

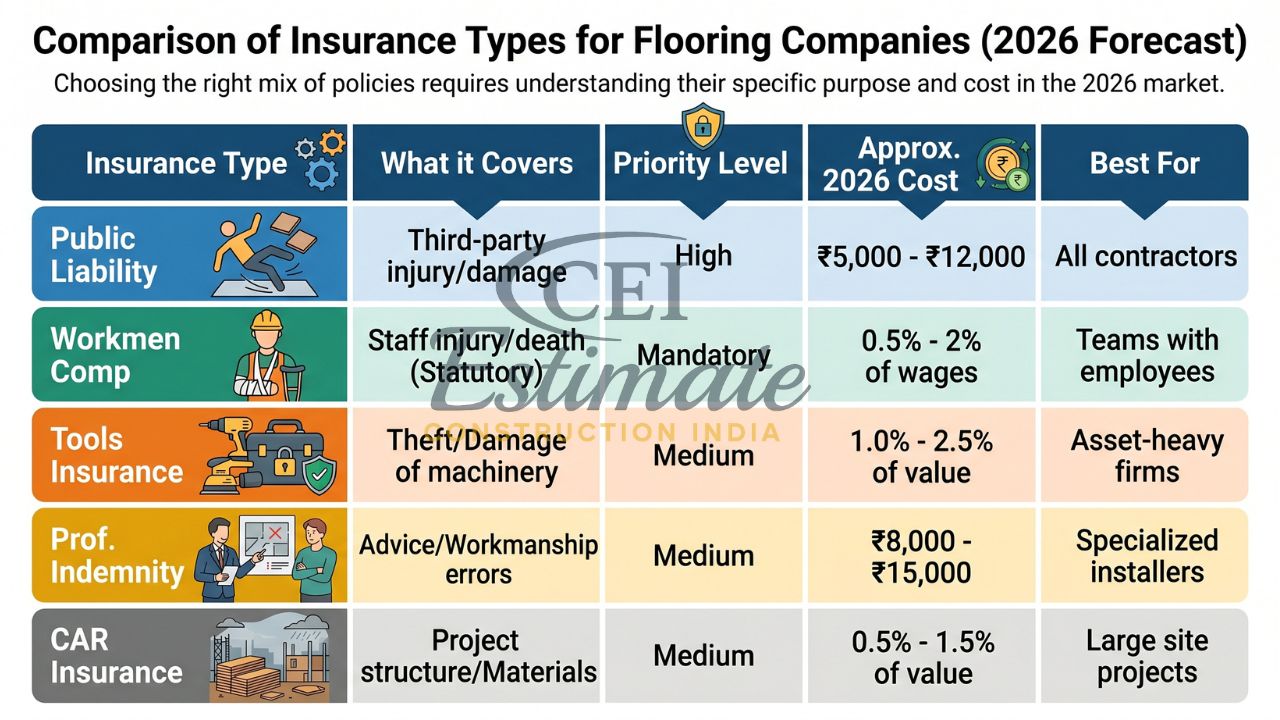

Comparison of Insurance Types for Flooring Companies

Choosing the right mix of policies requires understanding their specific purpose and cost in the 2026 market.

| Insurance Type | What it Covers | Priority Level | Approx. 2026 Cost | Best For |

|---|---|---|---|---|

| Public Liability | Third-party injury/damage | High | ₹5,000 – ₹12,000 | All contractors |

| Workmen Comp | Staff injury/death (Statutory) | Mandatory | 0.5% – 2% of wages | Teams with employees |

| Tools Insurance | Theft/Damage of machinery | Medium | 1.0% – 2.5% of value | Asset-heavy firms |

| Prof. Indemnity | Advice/Workmanship errors | Medium | ₹8,000 – ₹15,000 | Specialized installers |

| CAR Insurance | Project structure/Materials | Medium | 0.5% – 1.5% of value | Large site projects |

How Much Does Insurance Cost for a Flooring Company in 2026?

In 2026, basic insurance for a flooring business remains affordable if purchased correctly. For a solo freelancer or a small team of 2-3 workers, a combined package of public liability and personal accident cover often starts around ₹6,000 to ₹10,000 per year. Medium-sized companies with higher turnovers and more equipment may pay between ₹30,000 and ₹75,000 annually.

Factors affecting the cost of insurance for flooring company 2026 include:

- Project Location: Working in high-seismic zones like Delhi-NCR (Zone IV/V) or flood-prone areas in UP can slightly increase premiums.

- Type of Flooring: Industrial epoxy or marble polishing carries more risk than vinyl click-lock installation.

- Safety Record: Contractors with zero past claims and proper PPE (Safety shoes, masks) usage often negotiate better rates.

Step-by-Step Guide to Buying Insurance for Your Flooring Company

Navigating the insurance market in 2026 is faster thanks to digital platforms. Follow these steps to secure your business:

- Assess Your Risk: Count your workers, list your expensive tools, and determine your typical project value.

- Define Coverage Limits: For residential work, a ₹5-10 lakh liability limit is standard; commercial projects may require ₹50 lakhs+.

- Compare Quotes: Use digital portals from leading Indian insurers like ICICI Lombard, HDFC Ergo, New India Assurance, or Go Digit to find trade-specific policies.

- Gather Documents: You will typically need your Aadhaar/PAN, GSTIN (if applicable), and an equipment inventory.

- Review the Fine Print: Ensure “monsoon damage” and “third-party property damage” are explicitly covered.

How to Include Insurance Costs in Your Flooring Quotations?

A common mistake is treating insurance as a “hidden cost” that eats into your profit. At Construction Estimator India, we recommend adding insurance as a specific line item in your Bill of Quantities (BOQ) or quotation. Label it as “Insurance & Site Safety Compliance”.

Typically, you should calculate this as 1% to 2% of the total project value. When you explain to your client in Meerut or Noida that this small fee ensures their property is protected against accidental damage and that your workers are legally covered, most clients view it as a sign of professionalism and are happy to pay.

Conclusion

Securing the right insurance for flooring company operations is not just about avoiding legal fines; it is about building a professional and sustainable business in the competitive 2026 market. From public liability that shields you against property damage to workmen compensation that protects your team, these policies form the invisible foundation of your company’s growth.

Being “insured and assured” separates a top-tier contractor from a risky freelancer. Don’t wait for a site tragedy to realize the value of protection. Get properly insured today to ensure your flooring career remains as solid as the surfaces you install. For professional assistance with job costing, BOQ preparation, and accurate quotations that include insurance expenses, contact Construction Estimator India today.

FAQ Section

What insurance does a flooring company need in India?

The most essential policies are Public Liability Insurance (for property damage), Workmen Compensation (for worker injuries), and Tools/Equipment insurance.

Is public liability insurance mandatory for flooring contractors?

While not always a legal mandate for small private homes, it is almost always contractually mandatory for commercial projects and work in RERA-registered buildings in India.

How much does insurance cost for a flooring business?

In 2026, basic cover for a small team starts around ₹6,000–₹12,000 per year, while larger firms may pay ₹30,000+ depending on their assets and turnover.

What is professional indemnity insurance for flooring installers?

It covers you if a client sues for financial losses caused by your technical errors, such as using the wrong adhesive or providing faulty design advice.

How can I insure my flooring tools and equipment?

You can buy a “Contractors Plant & Machinery” (CPM) or a “Portable Equipment” policy. You must provide an inventory of tools with their current market value.

Does workmen compensation cover my installation team?

Yes, a WCI policy specifically covers medical costs and compensation for any laborer, helper, or technician injured while working under your supervision.

What happens if I damage a client’s property during flooring work?

If you have Public Liability insurance, the insurer handles the legal claim and pays for the repairs (up to your policy limit), protecting your personal savings.

How do I add insurance cost to my flooring quotations?

Add a separate line item labeled “Insurance & Safety Compliance” in your BOQ, typically calculated as 1-2% of the total labor and material cost.

Can a small flooring company afford comprehensive insurance?

Yes. Most Indian insurers now offer micro-policies for small tradespeople that are very affordable and far cheaper than the cost of one major site accident.

Which insurance company is good for flooring contractors in India?

Top providers for 2026 include ICICI Lombard, HDFC Ergo, New India Assurance, and Go Digit, known for quick digital claims and specialized trade covers.