Imagine you are a committee member of a vibrant Resident Welfare Association (RWA) in Greater Noida or Meerut. Your society has just completed its annual maintenance drive, and the lush gardens and freshly painted lobbies look spectacular. One evening, an unusually severe short circuit in the common electrical panel room triggers a fire that ravages the primary lift shafts and causes structural cracking in the stairwell. As the repair estimates cross ₹50 lakhs, the realization hits: the society has no comprehensive building insurance for housing society policy. The RWA is forced to ask already stretched residents for a massive “emergency levy,” leading to internal conflict and delayed repairs. This scenario is a frequent nightmare for thousands of societies across North India that neglect collective structural protection.

In a housing society or multi-story apartment complex, the building structure and common areas are shared assets. While you own the air space within your flat, the foundation, external walls, and facilities like the gym, lobby, and transformer rooms are jointly held. Therefore, the responsibility for protection shifts from the individual to the collective body. Building insurance for housing society—often called a society master policy—is a specialized financial shield that covers the entire physical framework of the complex against catastrophic risks like fire, flood, earthquake, and storm.

This guide explores the vital importance of building insurance for housing society in the 2026 Indian real estate market. We will delve into why individual policies aren’t enough, how to calculate the correct sum insured, and the step-by-step process for RWAs to secure their residents’ multi-crore investments. Whether you are an office bearer in Noida or a developer in Ghaziabad, understanding this protection is the first step toward total financial peace of mind.

What is Building Insurance for Housing Society?

In the Indian context, building insurance for housing society refers to a “Master Policy” taken out by the RWA or the building’s cooperative society to protect the entire physical asset. Unlike a personal home insurance policy that covers only your internal belongings, this policy focuses on the “immovable” skeleton of the development. It treats the entire residential complex—including all individual flats, common corridors, and utility infrastructure—as a single unit of risk.

The concept of a master policy is rooted in the “reinstatement” principle. If a catastrophe were to level a wing of the society, the policy provides the funds to rebuild the structure to its original state using current material and labor rates. This is fundamentally different from individual flat policies, where a “coverage gap” often exists between what one owner insures and what the neighbor does. By taking a collective building insurance for housing society, the RWA ensures that the entire shell, from the foundation to the terrace, is protected under a unified contract.

Why Housing Societies Need Dedicated Building Insurance?

As we navigate 2026, the complexity of urban living in India has escalated. Shared risks are no longer theoretical; they are daily realities. Here is why a dedicated policy is non-negotiable for any housing society:

- Collective Risk Management: In high-density apartments, your safety is inextricably linked to your neighbor’s. A kitchen fire in Flat 201 can cause structural damage to the slab of Flat 301. Without a master policy, disputes over liability can halt repairs for years. A society-wide policy ensures the structure is restored regardless of where the peril originated.

- Protection Against Natural Calamities: Cities like Meerut, Ghaziabad, and Noida sit in High-Seismic Zones (Zone IV and V). The frequency of erratic monsoons leading to localized flooding is also rising. Building insurance for housing society provides the immense capital required to retrofit or rebuild after an earthquake or flood—funds that an RWA cannot generate through monthly maintenance alone.

- Legal and RERA Obligations: Under the Real Estate (Regulation and Development) Act (RERA), builders are responsible for structural defects and must maintain insurance for the project until it is officially handed over. Post-handover, the RWA assumes the legal stewardship of the asset. Failing to insure common property can be seen as a breach of fiduciary duty by society office bearers.

- Bank and Mortgage Requirements: Most banks (SBI, HDFC, ICICI) require structural insurance for home loans. Often, lenders will accept the RWA’s master policy as proof of coverage for individual units, making it more cost-effective for flat owners while ensuring the bank’s collateral is secure.

What Does Building Insurance for Housing Society Cover?

The modern building insurance for housing society in 2026, typically governed by the IRDAI-mandated Bharat Griha Raksha for housing society framework, offers comprehensive protection. It is designed to cover the “bricks and mortar” and everything permanently fixed to them.

Core Covered Areas

- The Main Structure: The foundation, load-bearing walls, floors, roofs, and balconies of all blocks within the society.

- Common Infrastructure: Lifts, escalators, staircases, lobbies, and the external facade.

- Utility Systems: Transformer rooms, diesel generators (DG sets), common water pumps, and concealed plumbing/electrical networks.

- Shared Amenities: The clubhouse, swimming pool structure, gym facilities, and compound walls.

Insured Perils

- Natural Disasters: Full coverage for earthquakes, floods, inundation, storms, cyclones, and landslides.

- Fire and Accidental Hazards: Protection against accidental fires, lightning, and domestic gas cylinder explosions.

- Impact and Man-Made Damage: Damage caused by vehicles crashing into boundary walls, falling trees, or riots and malicious acts.

- Water Damage: Bursting of common overhead water tanks or overflowing pipes (covering the resulting structural damage).

Essential Add-ons for 2026

- Debris Removal: Covers the cost of clearing the site after a disaster (usually up to 2% of the claim).

- Professional Fees: Pays for architects and surveyors required for reconstruction (up to 5%).

- Public Liability: Protects the RWA against legal claims if a visitor is injured on the society premises due to structural failure.

RWA Master Policy vs Individual Flat Owner Insurance

One of the biggest points of confusion is whether an individual owner still needs insurance if the RWA has a master policy. The answer lies in the distinction between “Structure” and “Contents.”

| Feature | RWA Master Building Insurance | Individual Flat Owner Insurance |

|---|---|---|

| Primary Responsibility | RWA / Society Management | Individual Apartment Owner |

| Primary Scope | Building skeleton, facade, common areas, and shell of flats | Furniture, electronics, jewelry, and internal renovations |

| Sum Insured Basis | Reinstatement value of the entire complex | Market value or replacement cost of belongings |

| Coverage Focus | Structural integrity and shared utilities | Personal property and third-party liability inside the flat |

| Cost Sharing | Paid via maintenance dues or society funds | Paid individually by the owner |

| Mandatory Status | Often required by RERA/Banks/Bylaws | Highly recommended but strictly voluntary |

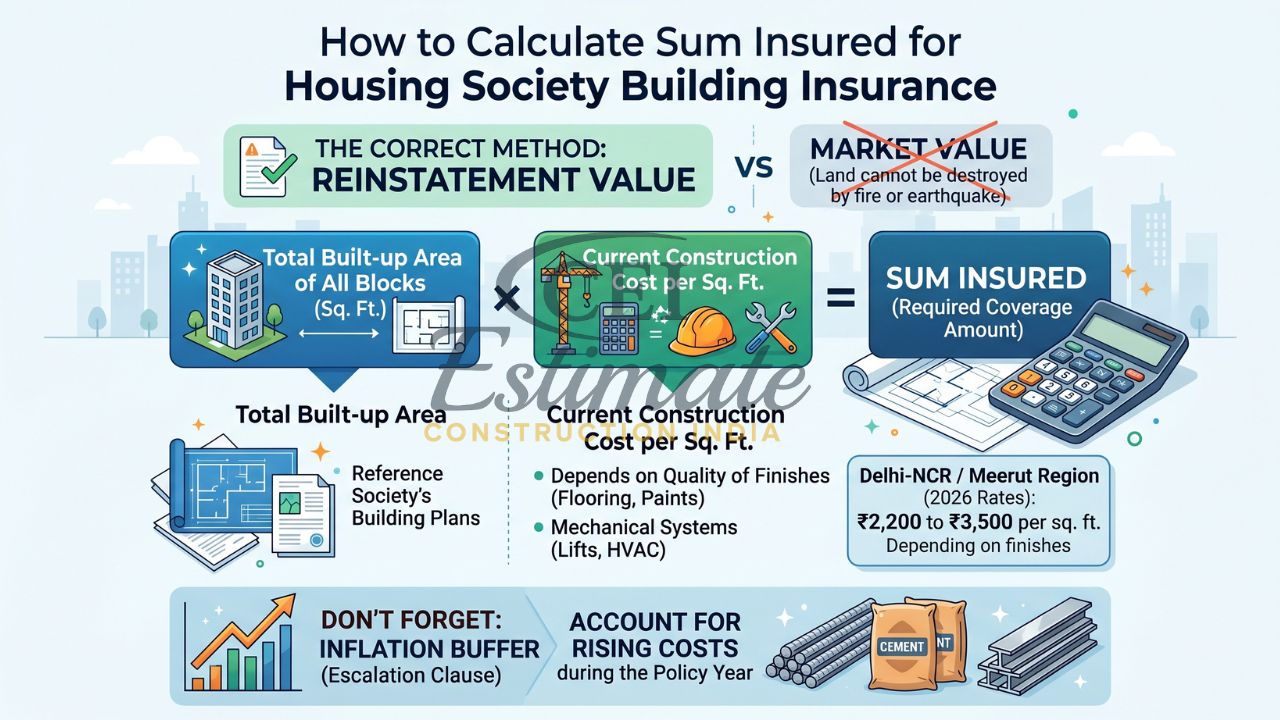

How to Calculate Sum Insured for Housing Society Building Insurance?

Calculating the “Sum Insured” is the most critical step for an RWA. A common mistake is using the “Market Value” of the property. For insurance, the land value is irrelevant because land cannot be destroyed by fire or earthquake.

Instead, societies must use the Reinstatement Value method. This is the estimated cost to rebuild the entire complex from scratch at today’s rates.

- Formula: (Total Built-up Area of All Blocks in Sq. Ft.) × (Current Construction Cost per Sq. Ft.).

- 2026 Rates: In the Delhi-NCR or Meerut region, standard high-rise construction costs range from ₹2,200 to ₹3,500 per sq. ft., depending on the quality of finishes and mechanical systems (lifts, HVAC).

- Inflation Buffer: Ensure the sum insured includes an “escalation clause” to account for the rising cost of TMT bars and cement during the policy year.

Cost of Building Insurance for Housing Society in India 2026

The cost of building insurance for housing society is remarkably low when distributed across all members. In 2026, annual premiums for a standard RCC residential complex typically range from 0.15% to 0.45% of the total reinstatement value.

- Small Society (e.g., 50 flats): If the total reconstruction value is ₹25 Crores, the annual premium might range from ₹40,000 to ₹90,000. This translates to roughly ₹800 to ₹1,800 per flat owner per year—a tiny price for total security.

- Large Township (e.g., 500 flats): For a project valued at ₹200 Crores, the premium may range from ₹3 Lakhs to ₹7 Lakhs annually, often resulting in even lower per-unit costs due to bulk discounts.

Costs are usually shared among members based on their flat’s square footage, integrated into the quarterly maintenance bill. To get competitive quotes, RWAs should approach national insurers like ICICI Lombard, HDFC ERGO, or SBI General, specifically requesting the Bharat Griha Raksha for housing society wording.

Step-by-Step Guide for RWAs to Buy Building Insurance

- Obtain General Body Approval: Discuss the need for a master policy in the Annual General Meeting (AGM) and pass a formal resolution to secure the society’s assets.

- Professional Valuation: Contact a firm like Construction Estimator India to determine the accurate reinstatement value based on current market rates for materials and labor.

- Compare Multiple Quotes: Don’t just look at the premium. Compare the “exclusions” and the speed of the claims process.

- Select Relevant Add-ons: Ensure you include “Terrorism Cover,” “Escalation Cover,” and “Debris Removal”.

- Documentation: Keep the sanctioned building plans, Occupancy Certificate (OC), and RWA registration documents ready for the underwriting process.

Claims Process for Housing Society Building Insurance

When a disaster affects common areas or the structure, the RWA must act as the primary point of contact.

- Immediate Notification: Inform the insurer within 24 hours of the incident.

- Evidence Collection: Take high-quality photographs and videos of the damage to common areas and affected flats.

- Surveyor Coordination: A licensed surveyor will visit. Provide them with the original construction BOQ and repair estimates prepared by a qualified engineer.

- Settlement: The claim amount is usually paid to the RWA’s bank account (or jointly with the lender if there is a mortgage) to facilitate repairs for the entire building.

Why Estimators and Developers Must Include It in New Housing Projects?

At Construction Estimator India, we believe that insurance is a foundational component of project risk management. For developers, including the first three years of RWA building insurance premiums in the project’s “soft costs” builds immense trust with buyers and ensures seamless RERA compliance.

For construction estimators, adding insurance as a specific line item in the Bill of Quantities (BOQ) allows the future RWA to understand the “Total Cost of Ownership.” It prevents “budget shocks” when a new society finds it must suddenly pay for structural protection without an existing fund. Accurate estimation ensures the sum insured reflects the actual cost of TMT bars, cement, and labor in the 2026 market.

Conclusion

Securing a building insurance for housing society policy is the single most responsible action an RWA or builder can take in 2026. In the dense urban landscapes of Uttar Pradesh and the Delhi-NCR, structural risks are shared, and a master policy is the only way to ensure collective financial survival. By focusing on the reinstatement value and adopting the standardized Bharat Griha Raksha framework, communities can safeguard their multi-crore investments against the unpredictable perils of nature and man.

Don’t leave your society’s safety to chance. Whether you are an owner in Meerut or a developer in Noida, make insurance a priority today. For professional BOQ preparation, accurate construction cost estimation, and insurance-inclusive project planning, contact Construction Estimator India today. Let us help you protect the foundation of your community.

FAQ Section

What is building insurance for housing society?

It is a master insurance policy taken by an RWA to cover the entire structure of the building, including all flats and common areas, against risks like fire and natural disasters.

Who should buy the master building insurance — RWA or individual owners?

The RWA should purchase the master policy for the structure and common areas. Individual owners should focus on “contents insurance” for their personal belongings.

How is sum insured calculated for apartment societies?

It is calculated as the total built-up area multiplied by the current cost of construction per square foot (Reinstatement Value). It excludes land cost.

How much does building insurance cost for a housing society?

Annual premiums typically range from 0.15% to 0.45% of the total reconstruction cost. For a medium-sized society, this often amounts to less than ₹2,000 per flat owner per year.

Is building insurance mandatory for housing societies?

While not a universal law, it is often required by banks for home loans, mandated by RERA for developers, and required by many society bylaws.

What add-ons are recommended for RWA building insurance?

Recommended add-ons include Terrorism Cover, Escalation Cover (to handle rising material costs), and Public Liability (to cover visitor injuries).

Does Bharat Griha Raksha work for housing societies?

Yes, Bharat Griha Raksha is the standard IRDAI policy designed for residential structures, including multi-story apartment complexes managed by RWAs.

How are insurance premiums shared among flat owners?

The total premium is usually divided among owners based on their flat’s carpet area and collected as part of the periodic maintenance dues.

What is covered in common areas of the society?

Coverage includes lifts, lobbies, staircases, gymnasiums, clubhouses, swimming pools, boundary walls, and shared utility systems like transformers.

How to include building insurance cost in new housing society estimates?

Estimators should include it as a “Soft Cost” or “Operating Expense” line item in the BOQ, based on a 1-year or 5-year premium projection using current market rates.