In the evolving landscape of Indian real estate, the dream of owning a home is shifting from buying pre-built apartments to “self-construction.” Self-construction refers to the process where you already own a plot of land and intend to build a customized house on it according to your specific needs, aesthetics, and family requirements. This approach offers unparalleled control over the quality of materials, the architectural layout, and the long-term scalability of the property. Whether it is a G+1 independent villa in a Tier-2 city or a modern multi-story residence in a metropolitan suburb, building your own home is a deeply personal and significant financial venture. Engaging with experienced building contractors ensures your visual goals translate flawlessly on the ground.

👉 Planning a Self-Construction Loan? Get Expert Guidance Before You Apply.

However, the financial mechanism for building on your own plot is distinctly different from purchasing a ready-to-move-in flat. While a standard home loan for an apartment involves a single disbursement to a builder, a loan for self-construction in India is a phased financial product. The bank does not give you the entire money upfront; instead, funds are released in stages as the walls rise and the roof is cast. This requires meticulous planning, a sanctioned building plan, and a very clear understanding of your construction budget. Understanding how to plan home construction in India from day one prevents unnecessary administrative friction.

Many Indian families and NRIs face hurdles because they approach banks without a professional cost estimate, leading to loan amounts that are either too low to finish the house or too high for their eligibility. This is where Construction Estimator India plays a pivotal role. They assist future homeowners by providing forensic-level cost breakdowns, ensuring you know exactly how much the project will cost before you even step into a bank.

If you want to understand how much money you will need to build on your plot before talking to banks, you can contact Construction Estimator India on WhatsApp / Call +91 8630676890 for construction cost estimation services. Getting a professional estimate early prevents “budget creep” and ensures your loan application is backed by data.

Understand What a Self-construction Loan Is

Difference Between Self-construction Loan and Normal Home Loan

A self-construction loan is a specific category of home finance designed for individuals who own a plot of land and want to construct a residential unit. In a normal home loan for a flat, the bank evaluates the builder’s credibility and the project’s overall progress. The transaction is often between the bank and the builder. In contrast, for a self-construction loan, the transaction is between the bank and you. The bank treats you as the “project manager.”

The primary difference lies in the disbursement. For a ready flat, the bank pays 80-90% of the value at once. For self-construction, the bank monitors the site. They will release 10-15% for the foundation, another 20% for the ground floor slab, and so on. This matters because you must manage your cash flow carefully. If the bank’s inspector is not satisfied with the construction quality or progress, the next installment could be delayed, potentially stopping work on-site. Knowing your expected house construction per sq ft rate establishes a key baseline prior to this evaluation.

Common Mistake: Many borrowers assume they will receive the entire sanctioned amount in their bank account immediately after the loan is approved. This never happens. To avoid work stoppages, use Construction Estimator India to plan your cash flow according to these bank stages.

👉 Improve Your Loan Approval Chances with Accurate BOQs and Cost Estimates.

When a Self-construction Loan Is Typically Used

This loan is the ideal choice if you already have a plot registered in your name or if you are inheriting family land and wish to build a new structure. It is also used when you have an existing small structure on a plot and want to demolish it to build a larger, modern home.

For many NRIs, this is the most common route to building a “home base” in India. Since they already own ancestral land, a self-construction loan allows them to fund the build without liquidating their international savings. It provides a structured way to monitor the project’s financial health from abroad, as the bank acts as a secondary auditor of the construction progress.

Basic Features of Self-construction Loans in India

Self-construction loans typically offer the same interest rates as standard home loans, but the “Tenure” usually begins after a moratorium period (the time during construction when you might only pay interest, known as Pre-EMI).

- LTV (Loan-to-Value): Banks usually fund 70% to 80% of the construction cost.

- Sanctioned Plan: You cannot get this loan without a building plan approved by the local Municipal Corporation or Gram Panchayat.

- Tenure: Generally ranges from 15 to 30 years.

- Disbursement: Linked to physical milestones on-site.

Before you apply for a self-construction loan, Construction Estimator India can help you estimate your total construction budget so you know what loan amount to request. Reach out on WhatsApp / Call +91 8630676890.

Check Your Eligibility for a Self-construction Loan

Income, Age, and Credit Score Requirements

To secure a loan for self-construction in India, your personal financial health is the first gatekeeper. Banks operating under guidelines from the Reserve Bank of India (RBI) look deeply at your “Repayment Capacity.“

- Income: If you are salaried, your monthly take-home pay should ideally be at least 3 to 4 times the expected EMI. For self-employed individuals, 3 years of audited ITR (Income Tax Returns) are mandatory.

- Age: Typically, you should be between 21 and 60 (for salaried) or 65 (for self-employed) years old.

- Credit Score (CIBIL): A score of 750 or above is the “Gold Standard.” A lower score might not result in rejection, but it will certainly lead to higher interest rates or a lower loan amount.

Common Mistake: Applying for a loan right after changing jobs or during a period of high existing debt (like multiple car or personal loans). It is better to clear small debts to improve your “Debt-to-Income” ratio before applying.

👉 Get Expert Support for Self-Construction Loan Applications and Cost Estimation.

Land Ownership and Title Clarity

The bank is technically lending against the security of your land. Therefore, the “Title” must be clear and marketable.

- Search Report: The bank’s legal team will conduct a search for the last 13 to 30 years to ensure there are no legal disputes or unpaid taxes on the land.

- Ownership Pattern: If the land is jointly owned (e.g., by you and your father), both must be co-applicants for the loan.

- Agricultural Land: You cannot get a residential construction loan on land that is still classified as “Agricultural” in government records. You must first undergo a “Change of Land Use” (CLU) or NA (Non-Agricultural) conversion.

Practical Action: Ensure you have the original Sale Deed, Mother Deed (previous ownership records), and the latest Land Tax receipts ready.

Sanctioned Building Plan and Approvals

You cannot build whatever you want if you are using bank finance. The bank requires a “Sanctioned Plan” from the local authority (BDA, LDA, DDA, or the local Municipal Council).

- Technical Verification: The bank will send a technical officer to verify that the plan you submitted is what is actually being built.

- Deviations: If your plan is for 1,000 sq. ft. but you build 1,500 sq. ft., the bank may stop disbursements.

Common Mistake: Starting construction before the plan is formally approved. Banks often refuse to fund “regularized” structures or projects that started without a “Commencement Certificate.”

Estimate Your Construction Cost Before Applying

Why You Should Know Your Construction Budget First?

Knowing your budget is the most critical “pre-construction” step. The bank will only fund a percentage of the estimated cost. If your estimate is poorly prepared and you realize midway that you need 12 Lakhs more, getting a “top-up” loan during construction is extremely difficult and expensive.

A professional estimate helps you define your “Own Contribution.” If the total cost is 60 Lakhs and the bank funds 80% (48 Lakhs), you must ensure you have 12 Lakhs in your savings. Without a clear budget, you are building in the dark.

Basic Factors That Affect Construction Cost in India

Several variables influence the final price tag:

- Soil Condition: Hard rock or loose clay can dictate your selection of foundation types for house construction in India, potentially swinging foundation costs by 20%.

- Built-up Area: Every square foot added increases material and labor needs.

- Structural Selection: Evaluating the structural differences between RCC vs brick construction in India changes your structural outlays entirely.

- Location: Labor and material transport costs vary significantly between a metro city and a rural town.

Practical Action: You can share your plot size, city, and basic house plan with Construction Estimator India to get a rough idea of construction cost and loan requirement. This prevents you from asking the bank for too little or too much.

How Construction Estimator India Helps With Budget Planning?

Construction Estimator India acts as your financial consultant. They provide a detailed Bill of Quantities (BOQ). A BOQ is a document that lists every single item required—from the number of cement bags and tons of steel to the number of switchboards and liters of paint.

With this forensic-level data, you can:

- Negotiate better with contractors.

- Present a professional cost certificate to the bank, which increases the speed of loan approval.

- Track expenditures to ensure your “Own Contribution” is being spent wisely.

For house construction budget planning support, contacting the team at Construction Estimator India on WhatsApp / Call +91 8630676890 is a vital first step for any serious builder.

Prepare the Required Documents

Personal and Income Documents

The bank needs to know who you are and if you can pay them back.

- Identity & Address: Aadhaar Card, PAN Card, and Passport.

- Salaried: Last 3-6 months’ salary slips, Form 16, and 6 months’ bank statements showing salary credits.

- Self-Employed: 3 years of ITR with computation of income, P&L statements, and balance sheets certified by a CA.

Common Mistake: Providing bank statements with “unexplained” large cash deposits, which can raise red flags during the credit assessment.

Property and Land Documents

These prove you own the land you want to build on.

- Registered Sale Deed: The primary ownership document.

- Encumbrance Certificate (EC): Usually required for the last 13 to 30 years to show the land is free from any legal liability.

- Possession Certificate & Land Tax Receipts: Proof that you are in physical possession of the plot and have paid all dues to the government.

Construction-related Documents

This is what sets the loan for self-construction in India apart.

- Sanctioned Plan: The blue-print with the “Approved” stamp from the local body.

- Detailed Estimate: A cost estimate signed by a registered professional from top architects and architecture firms.

- Construction Agreement: If you have hired a contractor, the bank might ask for the signed agreement between you and the builder.

Step-by-step Action: Create a “Loan Folder” and keep three copies of every document. Banks often lose papers during the multi-level approval process.

Approach Banks or Housing Finance Companies

Comparing Different Lenders and Schemes

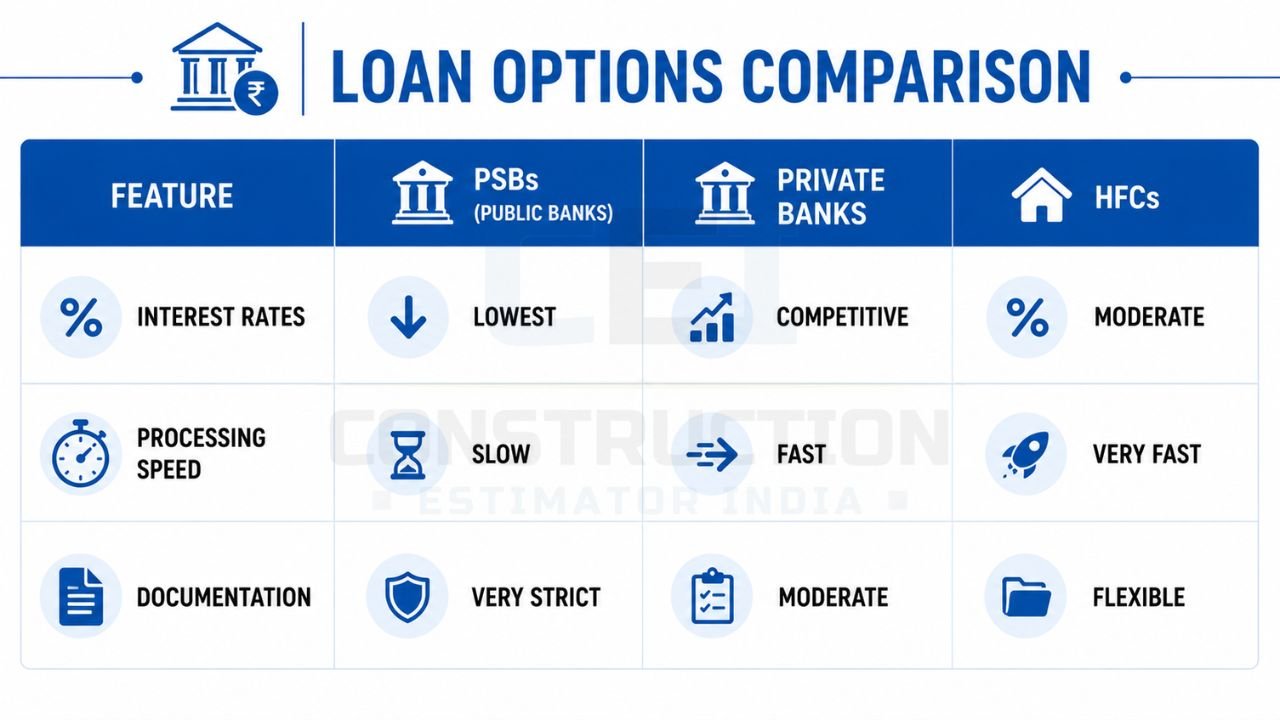

In India, you can approach three types of lenders, including major financial institutions like the State Bank of India (SBI) and HDFC Bank:

- Public Sector Banks (SBI, PNB, BOB): Often offer the lowest interest rates but have very strict documentation and slower processing times.

- Private Banks (ICICI, HDFC, Axis): Faster processing and better digital interfaces, but sometimes slightly higher rates or stricter credit score requirements.

- Technical Verification: An engineer visits the plot to see if it exists, measures it, and checks if the proposed structural system (such as an exact understanding of what is RCC construction) is safe and compliant.

| Feature | PSBs (Public Banks) | Private Banks | HFCs |

|---|---|---|---|

| Interest Rates | Lowest | Competitive | Moderate |

| Processing Speed | Slow | Fast | Very Fast |

| Documentation | Very Strict | Moderate | Flexible |

👉 Build with Confidence Using Accurate Construction Estimates for Bank Approval.

Online vs Offline Application

While most banks offer online applications, self-construction loans are “high-touch” products. You will likely need to visit the branch at least twice. The online portal is great for uploading income documents, but the original land deeds must usually be submitted in person for “Safe Custody.”

What Happens After You Submit Your Application?

Once submitted, the bank initiates a three-pronged verification:

- Credit Check: Verifying your income and CIBIL.

- Legal Verification: A lawyer checks the land title.

- Technical Verification: An engineer visits the plot to see if it exists, measures it, and checks if the proposed plan is feasible.

If you already own a plot and want to know how much loan you might need for construction, you can contact Construction Estimator India on WhatsApp / Call +91 8630676890 for practical cost estimation support.

Understand Loan Sanction, LTV, and Own Contribution

What “Sanction Letter” Means?

A “Sanction Letter” is not a guarantee of money in your hand; it is an offer. It states the maximum amount the bank is willing to lend you, the interest rate, the tenure, and the conditions you must meet before the first disbursement.

Common Mistake: Ignoring the “Conditions Precedent” in the sanction letter. These might include requirements like “Closing an existing credit card” or “Providing a life insurance policy assigned to the bank.”

Loan-to-Value (LTV) and How Much the Bank Will Fund

LTV is the percentage of the project cost the bank covers.

- If your land is worth 60 Lakhs and construction cost is 60 Lakhs (Total 1.2 Crore), the bank doesn’t lend 80% of 1.2 Crore.

- Usually, for self-construction, they lend 75-80% of the construction cost only, provided the land value is high enough to act as security.

- Formula: If Construction Cost = ₹48 Lakhs, Bank Loan (80%) = ₹38.4 Lakhs. You must provide the remaining ₹9.6 Lakhs.

Planning Your Own Contribution

The bank typically follows a “First In, Last Out” or “Pro-rata” rule. They want to see that you have spent your portion (the 20-25%) before they release the bulk of their funds. You should have your savings ready in a liquid form to cover the initial stages like excavation and foundation.

Practical Tip: Never use your entire savings for the land purchase if you plan to build immediately. Save enough to cover the initial 20% of construction and a 10% contingency fund.

How Construction Loan Disbursement in Stages Works?

Stage-based Disbursement Linked to Construction Progress

The bank will release the loan for self-construction in India in roughly 4 to 6 installments. A typical schedule looks like this:

- Plinth Level: After the foundation and ground-level beams are done.

- Lintel/Slab Level: Once the walls are up and the first-floor roof is ready to be cast.

- Brickwork & Plastering: After the shell of the house is complete. Knowing which grade cement is best for plastering in India ensures you allocate material funds efficiently during this phase.

- Finishing: Flooring, plumbing, and electrical works. Keeping close tabs on your plaster cost per square foot with material in India prevents final-stage budget slippage.

- Final Release: After the completion certificate or “Occupancy Certificate” is shown.

Bank Inspections and Valuation Visits

Before every installment, the bank’s empanelled technical person will visit your site. They will take photos and verify that the concrete, masonry, and safety parameters match standards regulated by the Bureau of Indian Standards (BIS).

Construction Estimator India offers support for planning phased construction and understanding money flow (own contribution + bank disbursement), ensuring you never run out of cash mid-stage.

Managing Cash Flow During Construction

Construction is notorious for delays. If your contractor demands money for the roof, but the bank inspector hasn’t visited yet, work might stop.

- Tip: Always keep a “bridge fund” (at least 1-2 months of expenses) to keep the labor on-site while the bank processes the next disbursement.

Common Mistakes People Make When Taking a Self-construction Loan

Applying Without Clear Cost Estimate

This is the number one reason for project failure. People “guess” the cost is 36 Lakhs, take a loan for 28.8 Lakhs, and then find out mid-way that the actual cost is 54 Lakhs. They are left with a half-finished house that they cannot live in but must still pay EMIs for.

How to avoid: Get a detailed home construction quantity takeoff from Construction Estimator India before applying.

👉 Start Your Dream Home Project with the Right Financial Planning and Expert Support.

Ignoring Land Title Issues and Approvals

Many people build on “Power of Attorney” land or land without a clear “NOC” from the local development authority. Banks will reject these applications flatly.

- How to avoid: Get a “Legal Scrutiny Report” (LSR) from a bank-empanelled lawyer even before you finish your house plans.

Overestimating or Underestimating Project Cost

Underestimating leads to a funding gap. Overestimating leads to higher processing fees and higher “Pre-EMI” interest payments on money you might not even need yet.

Not Understanding Stage-wise Disbursement

Assuming the bank will pay the contractor directly or will pay based on “bills” rather than “physical progress” is a common trap. Banks pay for work done, not for materials bought.

Construction Estimator India can help you align your contractor’s payment schedule with the bank’s disbursement stages to ensure smooth progress. Reach out on WhatsApp / Call +91 8630676890.

Practical Tips to Make the Process Smooth

Keeping Documents Complete and Organised

Keep a digital folder (Google Drive) with scanned copies of every receipt, every letter from the bank, and every bill from your contractor. You will need these for the final loan closure and for income tax benefits.

Coordinating Between Architect, Contractor, and Bank

You are the bridge. Ensure your architect provides the “Completion Certificate” for each stage promptly so the bank inspector can do their job. Communication gaps here are the biggest cause of disbursement delays.

Planning for Delays, Cost Changes, and Safety Margins

In India, material prices for cement and steel can fluctuate by 10-15% in a single quarter.

- The 15% Rule: Always have a buffer of 15% over the bank’s estimate. If the estimate is 60 Lakhs, plan for 69 Lakhs.

FAQs: Self-construction Loan in India

Can I get a self-construction loan if the plot is jointly owned?

Yes, but all owners of the plot must be co-applicants or guarantors for the loan. This is non-negotiable for most Indian banks.

Do I need an approved plan before applying for a construction loan?

Absolutely. No formal bank or HFC will sanction a construction loan without a sanctioned plan from the local Municipal or Gram Panchayat authority.

How is the loan disbursed as construction progresses?

It is released in stages (Foundation, Slab, Finishing, etc.). After you finish a stage using your own funds or the previous installment, the bank inspects the site and releases the next portion.

What happens if my construction cost increases during the project?

You will likely have to fund the increase from your own pocket. Banks rarely increase the “Sanctioned Amount” once the project has started. This is why professional estimation from Construction Estimator India is so vital.

When should I contact an estimator like Construction Estimator India in the process?

The best time is before you apply for the loan but after you have a basic architectural floor plan. This allows you to go to the bank with an exact, professional figure.

Can NRIs get self-construction loans for property in India?

Yes, most major banks like SBI, HDFC, and ICICI have specific “NRI Home Loan” products for self-construction on owned plots.

Conclusion: Plan Your Construction and Loan Together

Securing a loan for self-construction in India is a journey that requires more than just a good credit score; it requires technical precision and financial foresight. By moving through the steps—from checking your land title to understanding stage-wise disbursements—you transform a complex banking process into a manageable project plan. The most successful homeowners are those who treat their house construction as a business project, where every rupee is accounted for and every stage is timed.

Remember, the bank is your partner, but they rely on the data you provide. A vague estimate leads to a vague loan, which leads to a stressful construction experience. Using professional tools like a Bill of Quantities and a forensic cost breakdown ensures that your dream home doesn’t become a financial burden.

If you own a plot and are planning to build your home through a self-construction loan, and want help estimating the total construction cost and planning your loan requirement, you can contact Construction Estimator India team on WhatsApp / Call +91 8630676890 before you submit your loan application.