Imagine you are a real estate developer in Noida or a general contractor in Meerut, finally securing the green light for a multi-crore shopping mall or a high-tech office plaza. You have the blueprints, the labor, and the funding lined up. However, just as construction is about to begin, your lending bank halts the first disbursement because your policy fails to meet the specific commercial construction insurance in India requirements. Suddenly, your project is paralyzed, not by a lack of materials, but by a missing line item in your risk management strategy.

This scenario is a frequent reality in the 2026 infrastructure boom, where the scale and public nature of commercial builds demand far stricter compliance than any residential villa. Commercial projects involve higher capital exposure, extensive third-party risks, and complex regulatory frameworks like the BOCW Act and the Employees’ Compensation Act. Protecting your commercial investment today ensures your project remains as safe as it is profitable. Understanding the nuances of different insurers and the mandatory legal landscape is no longer optional—it is a prerequisite for professional success in the Indian construction sector.

Commercial Construction Insurance Requirements in India

Navigating the legal and financial landscape of a commercial project requires a clear understanding of commercial construction insurance requirements in India. In 2026, several policies are absolute “must-haves” for any commercial site to satisfy institutional lenders like SBI or HDFC and comply with government regulations.

The “gold standard” for project protection is Contractors’ All Risk (CAR) Insurance. This policy acts as a comprehensive shield for the physical anatomy of your project, covering civil works, materials stored on-site—such as high-value steel and premium glass—and temporary structures. Given the public nature of malls and hotels, Public Liability or Commercial General Liability (CGL) is also vital, covering accidental bodily injury or property damage caused to third parties during construction.

Furthermore, providing Workmen Compensation Insurance (WCI) is a statutory requirement under the Employees’ Compensation Act 1923 and the BOCW Act 1996. Commercial sites are inherently riskier due to the use of heavy machinery and working at great heights; WCI ensures the insurer handles medical costs and legally mandated compensation for injured workers.

| Insurance Type | Legal Status in 2026 | Primary Coverage |

|---|---|---|

| Contractors’ All Risk (CAR) | Mandatory for Bank Finance/Tenders | Physical civil structure & site materials |

| Workmen Compensation (WCI) | Mandatory (Statutory Law) | Labor injury, disability, or death |

| Public Liability (CGL) | Mandatory for Commercial Zones | Third-party bodily injury & property damage |

| Erection All Risk (EAR) | Mandatory for MEP-Heavy Projects | Mechanical & electrical installations |

| BOCW Cess | Mandatory Tax (1%) | Social security for building workers |

Key Benefits of Insurance for Construction Projects

Beyond mere legal compliance, the benefits of insurance for construction projects in India are multifaceted, serving as a strategic business tool for risk management.

- Financial Protection and Liquidity: Insurance prevents catastrophic losses from fire, theft, or natural disasters (common in seismic zones like Delhi-NCR) that could otherwise bankrupt mid-sized firms. It allows companies to maintain operational continuity even when unforeseen accidents occur.

- Enhanced Professional Credibility: Maintaining a robust insurance portfolio makes it significantly easier to secure bank loans and win prestigious government tenders. It signals to clients that you are a responsible partner who has secured the project’s financial foundation.

- Risk Transfer and Peace of Mind: By shifting the financial burden of high-value risks to an insurer, developers can focus on execution rather than worrying about potential lawsuits or repair costs from accidental site damage.

- Legal and Humanitarian Safeguards: Comprehensive coverage ensures that injured workers receive immediate medical support and protects contractors from potential criminal charges or project shutdowns due to non-compliance with labor laws.

For a professional estimator, these premiums should be included as distinct line items under “Preliminaries” in the Bill of Quantities (BOQ) to ensure project protection from the first brick.

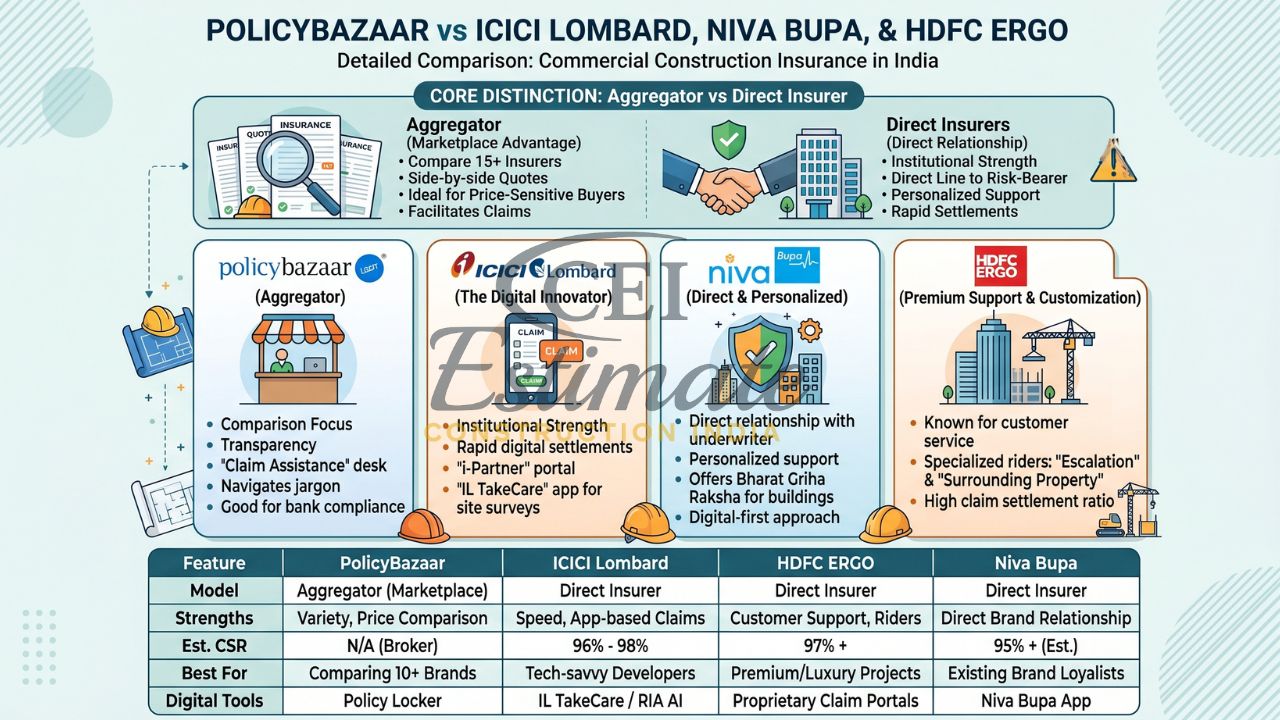

PolicyBazaar vs ICICI Lombard, Niva Bupa & HDFC Ergo – Detailed Comparison

Choosing the best platform or partner for commercial construction insurance in India involves weighing the variety of an aggregator against the direct relationship of a specialist insurer.

PolicyBazaar: The Aggregator Advantage

PolicyBazaar vs ICICI Lombard comparison often highlights transparency. As a digital marketplace, PolicyBazaar allows you to compare quotes from over 15 insurers side-by-side, which is ideal for price-sensitive buyers or first-time contractors seeking the most competitive rates for bank compliance. Their “Claim Assistance” desk acts as a facilitator, helping users navigate jargon and mediate with insurers.

ICICI Lombard: The Digital Innovator

Buying directly from ICICI Lombard offers institutional strength and rapid digital settlements. They are widely regarded for their “i-Partner” portal and “IL TakeCare” app, allowing for instant policy issuance and site surveys. With a claim settlement ratio (CSR) often ranging from 96% to 98%, they are a top choice for developers who prioritize speed and a direct line to the risk-bearer.

Niva Bupa: Direct and Personalized

When looking at PolicyBazaar vs Niva Bupa, the latter provides a direct relationship with the underwriter. While traditionally known for health insurance, Niva Bupa offers the IRDAI-mandated Bharat Griha Raksha for buildings, focusing on a digital-first approach and personalized support. It is particularly suited for builders who already have a brand relationship with them and value direct accountability during claims.

HDFC Ergo: Premium Support and Customization

The PolicyBazaar vs HDFC Ergo debate often centers on customer service and specialized riders. HDFC ERGO is known for its “Escalation” and “Surrounding Property” riders, which are essential for high-value commercial builds where material costs (like steel and cement) are volatile. Their CSR often exceeds 97%, making them a favorite for luxury residential-commercial plazas.

| Feature | PolicyBazaar | ICICI Lombard | HDFC ERGO | Niva Bupa |

|---|---|---|---|---|

| Model | Aggregator (Marketplace) | Direct Insurer | Direct Insurer | Direct Insurer |

| Strengths | Variety, Price Comparison | Speed, App-based Claims | Customer Support, Riders | Direct Brand Relationship |

| Est. CSR | N/A (Broker) | 96% – 98% | 97% + | 95% + (Est.) |

| Best For | Comparing 10+ Brands | Tech-savvy Developers | Premium/Luxury Projects | Existing Brand Loyalists |

| Digital Tools | Policy Locker | IL TakeCare / RIA AI | Proprietary Claim Portals | Niva Bupa App |

How to Choose the Best Insurance for Your Commercial Construction Project?

Selecting the best insurance for commercial construction in India requires more than just looking at the premium. In 2026, you must analyze your specific project profile. A high-rise mall in a seismic zone like Delhi-NCR (Zone IV) requires robust natural peril cover and high-limit Public Liability due to the proximity of the general public.

First, accurately calculate the Reinstatement Value. Do not use the market price; instead, multiply your built-up area by the current reconstruction cost (typically ₹2,500 to ₹3,500 per sq. ft. in 2026). Second, ensure your policy includes an Escalation Clause to protect against the rising costs of construction materials during the multi-year duration of a commercial build. Finally, verify the local surveyor presence; you need an insurer who can visit a site in Meerut or Ghaziabad quickly after an incident to prevent work stoppages.

Builders should consult the General Insurance Council or the IRDAI for the latest circulars on project insurance mandates.

Frequently Asked Questions (FAQs)

- Is CAR insurance compulsory for commercial projects?

While not always a legal mandate for private, self-funded builds, it is almost always compulsory for bank-financed projects, government tenders, and RERA-registered developments. - What is the typical cost of commercial construction insurance?

In 2026, total insurance costs generally range from 1% to 2.5% of the total project value, depending on location and risk class. - Does a commercial project need public liability insurance?

Yes. Due to the proximity of commercial sites to other businesses and the general public, high-limit public liability (CGL) is essential to protect against third-party claims. - Who is responsible for buying the insurance — the contractor or the owner?

Usually, the contract (like CPWD or FIDIC) specifies this. Often, the contractor buys the policy, but the cost is reimbursed by the owner as a BOQ line item. - What happens if insurance requirements are not met in a tender?

Your bid may be disqualified immediately, or you may face severe penalties and project delays if the lapse is discovered after the contract award. - Can subcontractors be covered under the main CAR policy?

Yes, most CAR and WCI policies for commercial sites can be extended to include subcontractors, provided they are listed as “Insured” or under the supervision of the main contractor. - What is an ‘Escalation Clause’ in building insurance?

It is a rider that automatically increases your sum insured annually (usually by 10%) to account for rising construction material costs like steel and cement. - Which insurer has the fastest claim settlement for construction?

In 2026, ICICI Lombard and Go Digit are recognized for their digital-first approach and rapid processing of standard construction claims. - How do I include insurance costs in my commercial BOQ?

List it as a specific line item under “Preliminaries” or “Project Overheads,” using actual quotes to ensure your profit margin is not eroded.

Conclusion

Successfully navigating commercial construction insurance in India is the hallmark of a professional builder in 2026. From mandatory CAR and Workmen Compensation to specialized ALOP and EAR covers, these policies form the invisible foundation of your company’s growth. Whether you choose the comparative variety of PolicyBazaar or the institutional reliability of giants like ICICI Lombard or HDFC ERGO, your priority must be ensuring the structure is insured for its true reinstatement value.In the competitive landscape of North India, comprehensive risk management is not just about safety—it is your greatest competitive advantage. Don’t let a single unforeseen accident derail your corporate vision. For professional BOQ services and construction cost estimation that accurately factors in all insurance requirements, contact Person at Construction Estimator India today