Imagine you are standing in front of your newly completed three-story home in Meerut, Uttar Pradesh. After months of tracking cement prices and coordinating with contractors, the structure is finally ready. You know you need to protect this asset, but a dilemma strikes: should you use the building insurance policy bazar vs niva bupa route? You might be a homeowner in Noida comparing quotes for a high-rise apartment, or a rental property investor in Delhi-NCR seeking the best coverage for your portfolio. The choice between an aggregator like Policybazaar and a direct specialist insurer like Niva Bupa can feel overwhelming when your life savings are on the line.

In 2026, the Indian insurance landscape is more transparent yet complex. Policybazaar stands as India’s largest insurance aggregator, offering a bird’s-eye view of multiple insurers under one digital roof. On the other hand, Niva Bupa (formerly Max Bupa), traditionally a health insurance giant, has expanded its expertise into robust general insurance products, including the IRDAI-mandated Bharat Griha Raksha. This article provides an unbiased, detailed comparison to help you decide the best way to buy building insurance for new builds, apartments, rental properties, or mortgaged homes. We will evaluate ease of purchase, premium competitiveness, coverage nuances, and the claim experience to determine which path suits your specific property needs. Whether you prioritize a “Niva Bupa home insurance review” or a broad “building insurance comparison Policybazaar Niva Bupa 2026,” this guide ensures your construction investment remains financially secure.

Understanding Building Insurance in India

Before diving into the comparison, you must understand what you are actually buying. Building insurance, often referred to as “structure insurance,” is designed to protect the “bones” of your property. Unlike home contents insurance, which covers your TV and furniture, building insurance covers the foundation, walls, roof, floors, and permanent fixtures like plumbing and wiring. In the event of a fire, earthquake, or flood—risks that are particularly high in seismic zones like North India—this policy ensures you can rebuild the structure without depleting your savings.

The buying channel you choose—aggregator versus direct insurer—significantly impacts your experience. An aggregator acts as a marketplace, while a direct insurer provides the actual product and manages your claims. In 2026, both channels offer the standard Bharat Griha Raksha policy, but the service layers, add-on availability, and premium discounts differ. For a construction estimator, knowing these differences is vital for accurately calculating the “soft costs” in a project’s Bill of Quantities (BOQ).

Policybazaar for Building Insurance – How It Works

Policybazaar functions as the “Amazon of Insurance” in India. When you look for building insurance on their platform, you aren’t buying a “Policybazaar policy”; instead, you are using their engine to compare dozens of insurers like HDFC Ergo, ICICI Lombard, and SBI General. The primary advantage for you is transparency. You can enter your property details once and see a ranked list of premiums and coverage features side-by-side.

The platform is incredibly user-friendly, allowing you to filter by “Claim Settlement Ratio” or “Key Features.” Their customer support often acts as a mediator, helping you understand complex jargon before you commit. However, the limitation is that you are often dealing with a third-party interface. While the initial purchase is seamless, some users find that for highly specialized or high-value industrial-residential hybrid properties, the standardized forms on an aggregator might not capture the unique risks as precisely as a direct consultation with an insurer would. For most standard apartments and independent floors in cities like Meerut, Policybazaar provides an unmatched ease of comparison.

Niva Bupa Building Insurance – Direct Purchase

Niva Bupa has built a massive reputation in India for health insurance and has successfully transitioned that service-oriented DNA into the general insurance space. Buying building insurance directly from Niva Bupa means you are entering a one-on-one relationship with the underwriter. Their core product, the Bharat Griha Raksha on Policybazaar vs Niva Bupa comparison often highlights Niva’s focus on a “digital-first” but “human-supported” claim process.

When you buy directly, you often get access to specific loyalty discounts if you already hold a health policy with them. Their digital portal for building insurance is streamlined, focusing on clear documentation and quick policy issuance. As a direct insurer, Niva Bupa has total control over the claim settlement journey. You don’t have to go through a middleman to find out the status of your surveyor or your payout. This direct accountability is a major strength for homeowners who prefer a single point of contact for all their insurance needs, especially when dealing with the stress of a property damage claim.

Head-to-Head Comparison: Policybazaar vs Niva Bupa

Choosing the best building insurance Policybazaar or Niva Bupa depends on your priorities. Below is a detailed comparison of how these two channels perform in the 2026 market.

| Comparison Feature | Policybazaar (Aggregator) | Niva Bupa (Direct Insurer) |

|---|---|---|

| Premium Price | Often lower due to platform-exclusive deals and a wide range of insurers. | Competitive; offers loyalty discounts for existing health insurance customers. |

| Choice & Variety | High; you can compare 15+ insurers instantly. | Single-brand focus; you only see Niva Bupa’s specific products. |

| Buying Process | Fully digital; instant comparison and multi-policy checkout. | Digital and personalized; direct access to Niva’s specialized advisors. |

| Claim Experience | Acts as a facilitator/mediator between you and the insurer. | Direct accountability; you deal only with Niva Bupa’s internal claim team. |

| Customer Support | High-volume call centers; helpful for general queries. | Specialized support; focused on Niva Bupa’s specific policy wordings. |

| Suitability | Best for comparing prices and for first-time buyers. | Best for brand loyalists and those seeking a direct relationship. |

| Property Types | Excellent for standard residential homes and apartments. | Strong for high-end residential and integrated family insurance. |

| Pros | Transparent comparison; “Claim Assistance” desk. | Fast direct processing; no “middleman” confusion. |

| Cons | Can feel like a “sales-heavy” environment; high call volume. | Limited to one company’s risk appetite and pricing. |

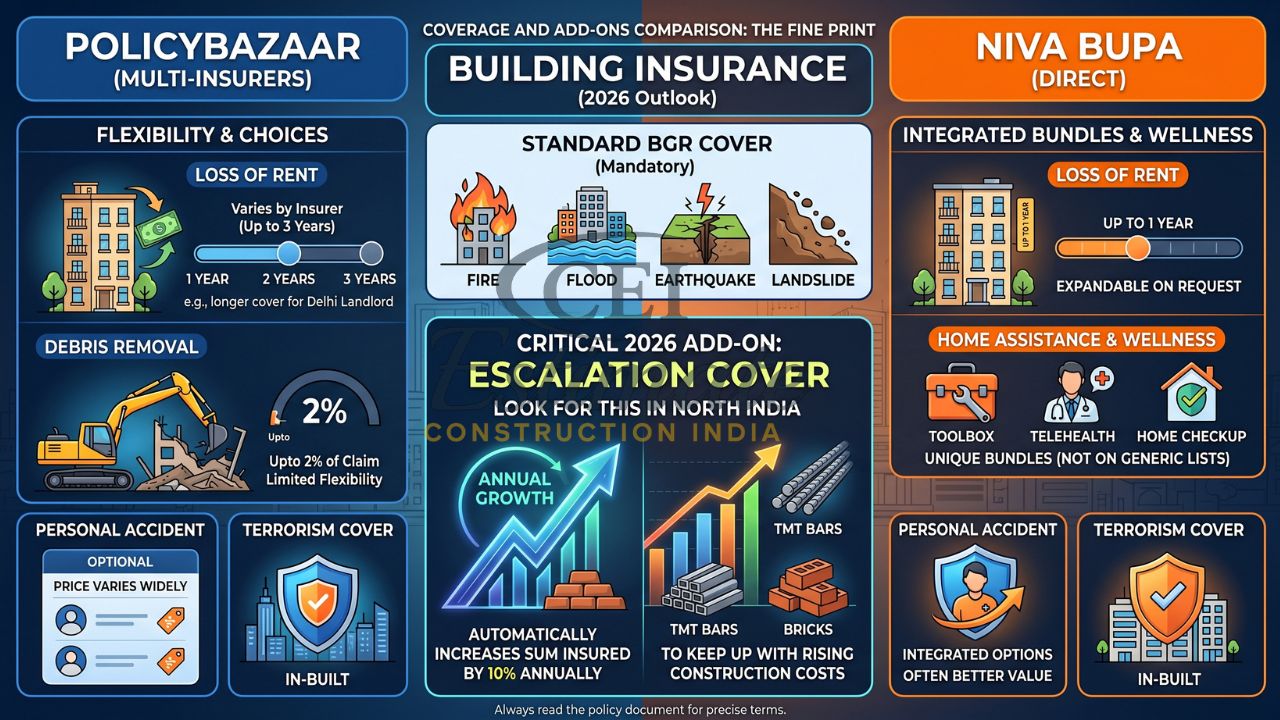

Coverage and Add-ons Comparison

When evaluating Policybazaar vs Niva Bupa building insurance, you must look at the “fine print” of coverage. Both offer the mandatory Bharat Griha Raksha, which covers fire, floods, earthquakes, and landslides. However, the flexibility of add-ons is where they diverge. Policybazaar allows you to see which insurer offers the best “Loss of Rent” or “Debris Removal” limits at the best price. For instance, if you are a landlord in Delhi, you might find an insurer on Policybazaar that offers 2 years of alternative accommodation cover versus Niva Bupa’s standard 1-year limit.

Niva Bupa, conversely, often bundles their building insurance with unique “wellness” or “home assistance” add-ons that might not be visible on a generic aggregator list. Their “Personal Accident” cover for homeowners is often more integrated. In 2026, you should look for “Escalation” add-ons—which automatically increase your sum insured by 10% annually to keep up with the rising cost of TMT bars and bricks in the North Indian market.

| Feature | Policybazaar (Multi-Insurers) | Niva Bupa (Direct) |

|---|---|---|

| Earthquake & Flood | Standard across all BGR plans. | Standard across all BGR plans. |

| Loss of Rent | Varies by insurer (up to 3 years). | Up to 1 year (expandable on request). |

| Debris Removal | Usually capped at 2% of claim. | Standard BGR limits (2%). |

| Personal Accident | Optional; price varies widely. | Integrated options; often better value. |

| Terrorism Cover | In-built in most listed BGR plans. | In-built in standard building plans. |

Cost and Value Comparison in 2026

Price is often the deciding factor for new home builders. In 2026, the premium for building insurance in India is remarkably affordable. For a structure with a reinstatement value of ₹50 Lakhs (the cost to rebuild, excluding land), a standard annual premium typically ranges from ₹2,000 to ₹4,500.

On Policybazaar, the value lies in the “search for the lowest.” You can often find a “budget” insurer that undercuts the market leaders by 10-15%. This is ideal for builders who need a policy primarily for bank mortgage compliance. However, a Niva Bupa home insurance review often highlights “value beyond the price.” By going direct, you might pay a slightly higher base premium but benefit from zero-commission structures or “Renewal Bonuses” that aren’t always passed through aggregators. For a rental property investor in Meerut, the value of a faster, direct claim settlement from Niva Bupa might far outweigh a ₹500 saving on the annual premium.

Which One Should You Choose – Policybazaar or Niva Bupa?

Your decision should be based on your specific profile as a property owner or professional.

- Choose Policybazaar if: You are a first-time home buyer or an apartment owner in a large society in Noida or Gurgaon. You want to see every available option in the market and choose the absolute lowest premium for mortgage requirements. You value having a third-party platform that can help escalate issues if the insurer delays your claim.

- Choose Niva Bupa if: You already have a health insurance policy with them and value the convenience of a single mobile app for all your needs. You are an individual villa builder in Meerut who prefers a direct relationship with the company that will eventually pay out your claim. You prioritize the “brand peace of mind” over saving a few hundred rupees.

For complex properties—like a residential building with a ground-floor commercial shop—going direct with Niva Bupa allows for a more “customized” underwriting approach that generic aggregator forms might struggle to categorize.

Step-by-Step Guide to Buying Building Insurance

Whether you choose the aggregator route or go direct, follow these steps to ensure you are properly protected:

- Calculate Reinstatement Value: Do not use the market price of your home. Multiply your built-up area (sq. ft.) by the current construction cost per sq. ft. (e.g., ₹2,200 to ₹3,500 in 2026).

- Gather Property Details: Keep your property tax receipts, carpet area measurements, and year of construction ready.

- Navigate to the Platform: Go to Policybazaar or the Niva Bupa website. Select “Home Insurance” or “Building Structure Insurance.”

- Compare Bharat Griha Raksha: Look for the “BGR” tag to ensure you are getting the IRDAI-standardized coverage.

- Declare Accurately: Never under-declare the area to save on premium. This leads to “Under-insurance” penalties during claims.

- Complete Payment: Use UPI or net banking for instant policy issuance. Your policy PDF should arrive in your email within minutes.

How to Include Building Insurance Cost in Your BOQ?

As an expert construction estimator, I always advise builders in Delhi-NCR to include the insurance premium as a fixed line item in the “Soft Costs” or “Project Overheads” section of the Bill of Quantities (BOQ). Including the cost of a building insurance policy—whether from building insurance policy bazar vs niva bupa—demonstrates a high level of professionalism to your client.

For a project in Meerut, a simple line item like “Insurance for Building Structure (Reinstatement Basis) – 1 Year: ₹4,500” ensures the client is aware of the protection from day one. It also protects you, the contractor, from liabilities if a natural disaster occurs shortly after handover but before the client has purchased their own policy.

Conclusion

The debate of building insurance policy bazar vs niva bupa ultimately comes down to your personal preference for “variety vs. relationship.” Policybazaar provides a powerful tool for comparison, ensuring you never overpay for your apartment or rental property insurance. Niva Bupa offers the stability and direct accountability of a reputed specialist, which can be invaluable during the high-stress period of a claim.

In 2026, as construction costs continue to rise across North India, having any form of building insurance is no longer optional—it is the foundation of your financial security. Make an informed choice based on your property type and service priorities. For homeowners and builders who need help calculating the exact reconstruction value of their assets, contact Construction Estimator India today. We provide professional BOQ and construction cost estimation services that integrate accurate building insurance costs, ensuring your project is protected from the first brick to the final handover.

FAQ Section

What is better for building insurance — Policybazaar or Niva Bupa?

It depends on your needs. Policybazaar is better for comparing multiple brands and prices. Niva Bupa is better if you want a direct relationship with the insurer and specialized service for their specific products.

Is buying on Policybazaar cheaper than Niva Bupa?

Policybazaar often shows the lowest prices in the market across many insurers. However, Niva Bupa may offer exclusive loyalty discounts to their existing health insurance customers that aren’t available on aggregators.

Does Policybazaar sell Niva Bupa building insurance?

Yes, Policybazaar typically lists Niva Bupa’s general insurance products alongside other competitors, allowing for a side-by-side comparison.

Which has better claim settlement for building insurance?

Both are regulated by IRDAI. Niva Bupa manages claims directly, while Policybazaar provides a “claims assistance” desk to help you navigate the process with the insurer you choose.

How do I compare building insurance quotes on Policybazaar?

Go to their website, select ‘Home Insurance’, enter your city (e.g., Meerut), property age, and carpet area. The platform will then display a list of quotes from different insurers.

Can I buy Bharat Griha Raksha from both platforms?

Yes. Bharat Griha Raksha is the mandatory standard policy in India. Both Policybazaar (via various insurers) and Niva Bupa (directly) offer this policy.

What documents are needed when buying building insurance?

Usually, no documents are required for the purchase. You just need the property address, area, and construction year. Documents like the sale deed are only required during a claim.

How to choose the right sum insured for building insurance?

Calculate the “Reinstatement Value”: [Total Built-up Area] x [Current Construction Rate per sq. ft.]. Do not include the land value.

Is direct purchase from Niva Bupa better for high-value properties?

Direct purchase can be beneficial for high-value villas as it allows for more detailed discussion with the insurer regarding specific structural risks.

How to include building insurance cost in my construction BOQ?

Add it under the “Project Overheads” or “Insurance & Compliance” section of your estimate, using a realistic premium based on the total construction cost.