Imagine you are a contractor in Meerut, overseeing a ₹10 crore residential development during the peak of the 2026 monsoon. Without warning, a series of unseasonal, torrential downpours hit West Uttar Pradesh, causing a massive landslide that collapses your foundation shoring and destroys ₹40 lakhs worth of TMT steel and cement stored on-site. For many, this would be a business-ending catastrophe. However, because you prioritized the benefits of insurance for construction projects, your claim was processed swiftly, allowing you to reinstate the site and complete the project without a single rupee of personal loss. This is the reality of modern risk management in India’s volatile infrastructure landscape.

Many contractors still view insurance as a burdensome, unnecessary expense that eats into their thin profit margins. In reality, the right portfolio—centered around a comprehensive Contractors All Risk (CAR) policy—is a high-performance business tool. In India’s high-stakes construction environment, characterized by extreme weather, seismic threats in the Delhi-NCR (Zone IV), and rising material theft in tier-2 cities, insurance is your ultimate shield. It is not just about protection; it is about growth, winning prestigious tenders, and maintaining a professional reputation that attracts high-value clients.

In this guide, we will explore the multifaceted advantages of insurance for construction projects India, from quantifiable financial gains to the intangible peace of mind it provides. We will also discuss how professional construction estimators integrate these costs into a Bill of Quantities (BOQ) to ensure your bids remain competitive yet secure. By the end, you will understand why insurance is not a cost to be minimized, but an investment in your firm’s survival and success.

Financial Protection – The Biggest Benefit

The most immediate and significant financial benefits of construction insurance lie in its ability to absorb catastrophic losses that would otherwise bankrupt a mid-sized firm. Construction sites are inherently vulnerable to a wide array of perils, ranging from fire and natural calamities to burglary and structural failures.

In 2026, the cost of raw materials like steel and copper has reached new heights. A single localized theft of high-value TMT bars or premium electrical wiring can drain lakhs from your project. A CAR policy provides comprehensive “all-risk” coverage, meaning it shields your physical anatomy—the permanent structure, raw materials, and temporary works like scaffolding—from sudden and unforeseen physical loss.

Consider a real-world scenario in Noida: A site fire caused by a short circuit in a temporary office shed spreads to the main structure, damaging the newly installed premium Italian marble flooring. Without insurance, the contractor faces a total loss. With a robust policy, the insurer covers the cost of clearing debris and replacing the materials. This financial safety net ensures that a single mishap does not derail your annual profits or lead to total insolvency.

| Quantifiable Financial Benefit | Description | Potential Saving in 2026 |

|---|---|---|

| Asset Protection | Covers reinstatement of walls, slabs, and foundations after collapse. | Up to 100% of Reconstruction Cost |

| Theft Recovery | Reimburses cost of stolen materials like TMT steel and copper. | 10–15% of Material Budget |

| Liability Shield | Pays for third-party property damage or bodily injury claims. | Unlimited Legal & Settlement Costs |

| Natural Peril Cover | Covers damage from earthquakes (Zone IV/V) and floods. | Full Project Reinstatement Value |

Risk Transfer and Business Continuity

One of the most profound advantages of insurance for construction projects India is the formal transfer of risk from your company’s balance sheet to the insurer’s. This strategic shift allows your business to maintain operational continuity even when a disaster strikes.

In the high-stakes Indian market, liquidity is king. If you are forced to pay out-of-pocket for a major site accident or a structural failure, your cash flow for other active projects is instantly choked. Insurance acts as a buffer, providing the necessary liquidity to resume work immediately after a loss. This ensures you don’t miss project deadlines, which in 2026 often carry heavy RERA-mandated penalties or contractual “liquidated damages”. By transferring the risk of “worst-case scenarios” to a professional insurer, you ensure that your firm remains a stable, long-term player in the industry.

Legal Compliance and Penalty Avoidance

In 2026, navigating the legal landscape of Indian construction requires more than just good workmanship; it requires strict adherence to statutory mandates. Why contractors need insurance for projects is often answered by the stringent requirements of the Building and Other Construction Workers (BOCW) Act and the Employees’ Compensation Act.

Workmen Compensation Insurance (WCI) is a non-negotiable legal requirement. If a worker suffers an injury or fatality on your site in Meerut or Delhi-NCR, you are legally liable to pay compensation based on their age and wages. Failing to maintain this insurance can lead to:

- Criminal Charges: Potential imprisonment for negligence.

- Heavy Fines: Penalties often exceeding ₹50,000 per violation.

- Project Shutdowns: Authorities can issue “Stop Work” notices until compliance is met.

- Blacklisting: Permanent debarment from bidding on government tenders.

Proper insurance ensures you meet these legal obligations seamlessly, protecting your license to operate and your future eligibility for high-profile contracts.

Easier Access to Bank Loans and Tenders

If you aim to scale your business and secure prestigious government or private projects, insurance is your ticket to the table. Most modern tenders in India, from smart city initiatives to high-speed rail corridors, mandate a comprehensive CAR policy and worker’s compensation as a prerequisite for bidding.

Furthermore, bank financing from institutions like SBI or HDFC is almost impossible to secure without a “Builders Risk” or CAR policy. Lenders view insurance as an essential safeguard for their collateral. By having a robust insurance portfolio, you improve your firm’s credibility and financial standing, making it significantly easier to secure the capital needed for large-scale developments. It signals to both banks and clients that you are a low-risk, professional partner.

Protection for Workers and Third Parties

The humanitarian and social benefits of insurance for construction projects are often the most vital for long-term sustainability. Construction is one of the highest-risk sectors in India, with falls, collapses, and machinery accidents being daily threats to an unorganized workforce.

- Workmen Compensation: Beyond fulfilling legal mandates, WCI ensures that injured workers like Ramesh, a mason in Meerut, receive immediate medical care and disability support without depleting your company’s funds. This boosts worker morale and loyalty, which is critical in a market facing a shortage of skilled labor.

- Public Liability: Third-party liability (TPL) coverage is essential in crowded urban areas. If falling debris damages a neighbor’s car or causes a pedestrian injury, your insurance handles the legal defense and compensation payouts, preventing expensive and reputation-damaging lawsuits.

Peace of Mind and Reputation Management

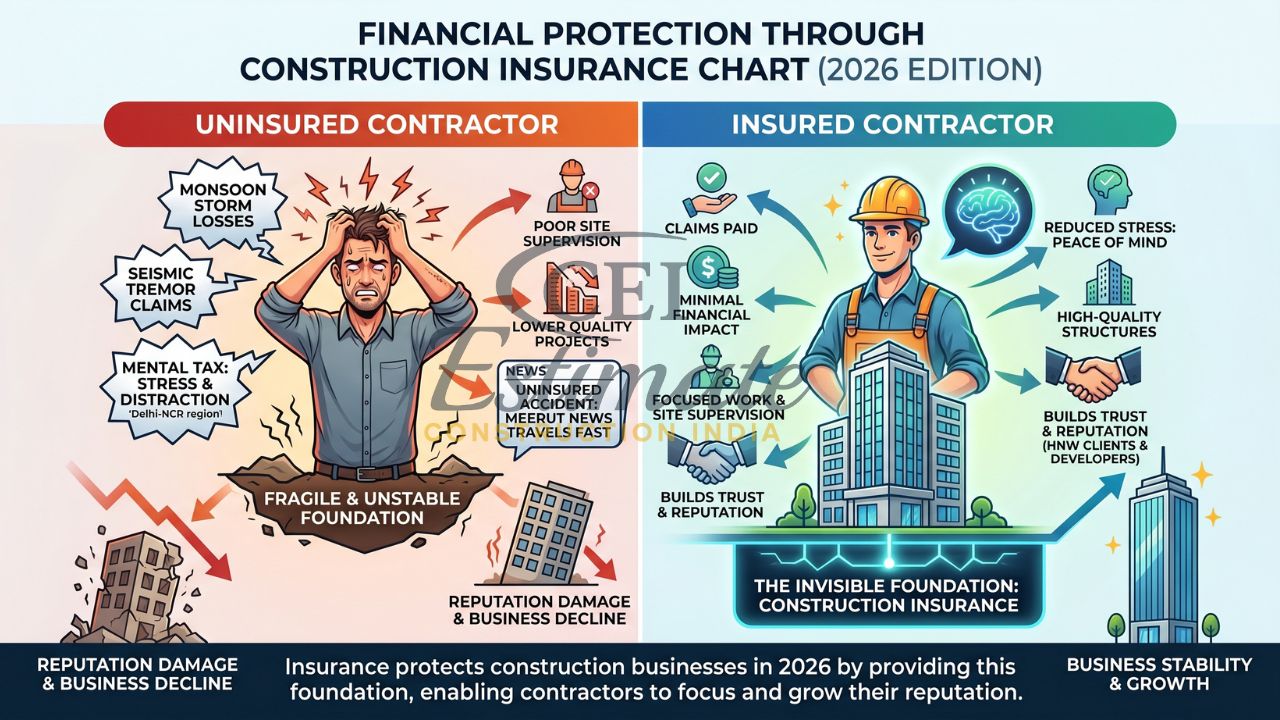

Insurance allows you to focus on what you do best: building high-quality structures. Without insurance, every monsoon storm or seismic tremor in the Delhi-NCR region becomes a source of extreme stress. This “mental tax” can distract you from site supervision and project quality.

Furthermore, your reputation is your most valuable asset. In tier-2 cities like Meerut, news of an uninsured site accident travels fast. Being known as a contractor who “takes care of their own” and has the financial backing to handle disasters builds immense trust with high-net-worth clients and developers. How insurance protects construction business 2026 is through this invisible foundation of trust and stability.

Cost-Benefit Analysis – Is Insurance Really Expensive?

When you perform a realistic cost-benefit analysis, insurance often emerges as one of the most affordable components of a project. In 2026, a standard CAR policy typically costs between 0.5% and 1.5% of the total project value. For a ₹1 crore project, a premium of ₹75,000 protects ₹100,00,000 of your capital.

Compare this to the potential loss: A single structural collapse or a significant fire can easily cost ₹20–50 lakhs. In such cases, the insurance policy pays for itself many times over. From the perspective of risk management in construction projects, paying a small, fixed premium is infinitely better than facing an unpredictable, potentially business-ending financial blow. When factored correctly into your BOQ, the cost of insurance is passed on to the client as a “fixed soft cost,” ensuring your profit margins remain untouched.

How to Maximize the Benefits of Insurance for Your Construction Projects?

To truly reap the rewards of your coverage, you must manage it actively:

- Set Accurate Sum Insured: Use current 2026 material and labor rates to determine the “reinstatement value”. Never under-insure to save on premiums, as this triggers the “Condition of Average” which reduces your payout.

- Include Essential Add-ons: Don’t settle for basic cover. Add riders for Escalation (to account for rising material costs), Debris Removal, and Surrounding Property.

- Maintain Safety Standards: Insurers often offer lower premiums or faster claim settlements to firms with a history of zero accidents and strict safety protocols.

- Meticulous Documentation: Keep detailed site logs, muster rolls, and photos of all materials delivered. This evidence is vital during a claim.

- Reliable Partners: Work with insurers like ICICI Lombard, HDFC Ergo, or New India Assurance who have high claim settlement ratios in the construction sector.

How Estimators Should Factor Insurance Benefits into Project Costing?

As a professional estimator, you should never treat insurance as a “lump sum” guess or a hidden overhead. It must be a distinct line item in your Bill of Quantities (BOQ). By categorizing it under “Preliminaries” or “Statutory Compliance,” you demonstrate professionalism to your client and protect your firm’s margins. Use actual market quotes based on the project duration and location to ensure your bid is both competitive and secure.

Conclusion

Mastering the benefits of insurance for construction projects is what separates a stable, long-term industry leader from a firm vulnerable to the next monsoon storm or site mishap. From the massive financial protection of a CAR policy to the legal safety of Workmen Compensation, insurance is the invisible foundation of your company’s growth in the competitive Indian landscape of 2026. It transforms unpredictable site hazards into manageable risks, allowing you to bid with confidence and build with total peace of mind.

Don’t let a single unforeseen accident derail your corporate vision or drain your hard-earned profit margins. Secure your future today by investing in a robust insurance portfolio. For professional BOQ and construction cost estimation services that accurately factor in all necessary insurance costs and benefits, contact Person at Construction Estimator India. Let us help you build a more resilient and profitable business.

FAQ Section

What are the main benefits of insurance for construction projects?

The primary benefits include total financial protection against material damage, risk transfer from the company to the insurer, legal compliance with acts like BOCW, and improved eligibility for bank loans and prestigious tenders.

How does CAR insurance benefit contractors?

CAR insurance acts as a “gold standard” shield, covering the permanent structure, raw materials, and temporary works from fire, flood, theft, and natural calamities. It also typically includes a third-party liability section.

Is insurance really necessary for small construction projects?

Yes. For a small residential project, a total loss from fire or a structural collapse can be even more devastating than for a large firm. Premiums for small projects are highly affordable, often starting at less than 1% of the project value.

Can insurance save money in the long run?

Absolutely. One major claim for material theft or structural damage can pay for decades of premiums. It also prevents costly lawsuits and government penalties for non-compliance.

What are the financial benefits of having proper construction insurance?

It protects your capital investment, ensures business continuity after a loss by providing liquidity, and prevents the erosion of your profit margins by covering unforeseen site disasters.

How does insurance help in winning tenders?

Most government and large private developers mandate proof of comprehensive insurance before awarding contracts. Having a robust policy signals that you are a low-risk, professional partner.

Does insurance cover worker injuries on construction sites?

Yes, Workmen Compensation Insurance (WCI) specifically covers medical expenses and compensation for workers who suffer injury, disability, or death while on duty.

How should I include insurance costs and benefits in my BOQ?

List insurance as a specific line item under “Project Overheads” or “Preliminaries” based on actual market quotes for the project’s duration and location.

What happens if I don’t have insurance for my construction project?

You face total personal liability for all site accidents, potential criminal charges for non-compliance with labor laws, and the risk of total insolvency if a natural disaster hits.

Which type of insurance gives the most benefits for construction projects?

Contractors’ All Risk (CAR) insurance is generally the most beneficial as it provides the broadest coverage for project assets and third-party liabilities in one package.