Buying a home is more than just a financial transaction; it is a milestone that marks the beginning of a new chapter in your life. In the Indian real estate market of 2026, the choice between a ready-to-move-in property and an under-construction flat is a pivotal decision. Buying an under-construction flat can be a smart investment—often cheaper than ready-to-move homes and with flexible payment structures. As an expert with over 15 years in the field, I have seen thousands of homeowners navigate this path. The key to a stress-free experience lies in understanding the financial instrument that makes it possible: the Home Loan for Under-Construction Property.

👉 Planning to Buy an Under-Construction Property? Get Expert Home Loan Guidance Today.

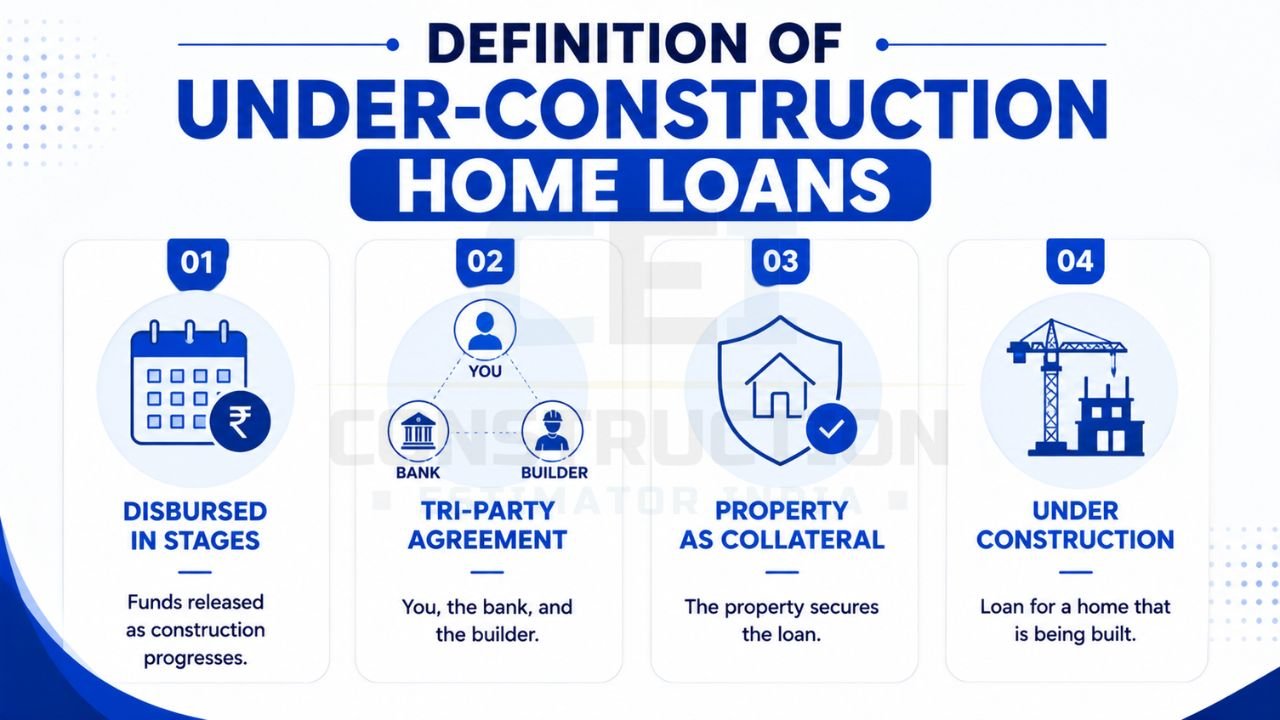

A home loan for an under-construction property is just like any other home loan — but disbursed in stages, not all at once. This fundamental difference is what allows you to manage your cash flow effectively while your dream home rises from the ground. When a Home Loan is taken on an under-construction property, the entire loan amount is not disbursed to the builder at once. Instead, the disbursal happens in parts on the basis of the completion of the stages of construction by the builder. This stage-wise funding ensures that the bank’s and your money are released only when physical progress is visible on-site. Knowing how to plan home construction in India from day one will save you massive financial headaches later.

A home loan for an under-construction property is usually disbursed in tranches. You will avail portions of the loan as and when the builder demands payment. This mechanism is designed to protect the buyer. If construction stalls, the bank stops the release of funds. Furthermore, some lenders only charge the EMIs on the amount disbursed. This means you aren’t paying interest on the full sanctioned amount from day one, which is a massive relief for those currently living in rented accommodation. The lender approves your total loan amount, but releases the money to the builder in parts (called tranches) as the construction progresses. This aligns the loan with actual work done, allowing you to pay interest only on the disbursed amount.

At Construction Estimator India, we believe that informed buyers are successful owners. Whether you are a first-time buyer or a seasoned investor, navigating the nuances of Pre-EMI, tax implications, and stage-wise disbursement requires professional guidance. Construction Estimator India offers a free home loan eligibility check at +91 8630676890 to help you start your journey with confidence.

What Is Home Loan for Under Construction Property: Definition & Key Features

Definition of Under-Construction Home Loans

A home loan for an under-construction property is just like any other home loan — but disbursed in stages. In simple terms, it is a credit facility provided by financial institutions to purchase a residential unit that is currently being built. Unlike a ready property where the bank pays the full amount to the seller immediately, here the relationship is a tri-party agreement between you, the bank, and the builder. The property acts as collateral, even though it doesn’t “exist” in its final form yet.

Feature 1: Stage-wise Disbursement (Tranches)

The most defining characteristic is that the loan is disbursed in tranches. The disbursal happens in parts on the basis of the completion of the stages of construction. For instance, once the foundation is laid, the builder issues a “demand letter.” The bank then sends a technical officer to verify the work before releasing the next installment. This ensures the builder remains accountable throughout the project lifecycle.

👉 Find the Right Home Loan Solution for Your Under-Construction Property.

Feature 2: Interest Only on Disbursed Amount

One of the most buyer-friendly features is that some lenders only charge the EMIs (or Pre-EMIs) on the amount disbursed. You pay interest only on the amount disbursed at each stage. If your total loan is ₹50 Lakhs but the bank has only released ₹10 Lakhs for the foundation, your interest obligation is calculated only on that ₹10 Lakhs. This significantly lowers your monthly financial burden during the construction years.

Feature 3: Loan-to-Value (LTV) Ratio

The LTV ratio determines how much the bank will lend against the property value. Usually, you can get up to 80% of the property’s agreement value, depending on your income and credit profile. In many cases, you can typically get 75% to 90% of the construction cost as a loan. This means you need to have at least 10% to 25% of the total cost as your “own contribution” or down payment.

Feature 4: Pre-EMI Option During Construction

During the construction stage, the borrower doesn’t have to pay the full EMI (Principal + Interest) on the sanctioned loan amount, but has to pay an interest amount only, called the Pre-EMI.

- Pre-EMI: Pay interest only on the disbursed amount. The actual EMI starts after full disbursement or possession.

- Full EMI: You can choose to start the full EMI immediately even if the full loan isn’t disbursed. This helps in repaying the principal faster and reduces the total interest paid over the loan tenure.

Step-by-Step Process to Get Home Loan for Under Construction Property

Step 1: Shortlist a Legally Approved Project

Before applying for a home loan, ensure the builder and project are approved by reputed lenders. Banks do their own due diligence, and if a project is “pre-approved,” the loan process is much faster. You must check for the RERA registration number, building plan approvals, the Commencement Certificate (CC), and the clear title deed of the land.

Step 2: Check Your Loan Eligibility

Banks evaluate your eligibility based on several factors: monthly income, credit score (a score of 700+ is preferred), current EMIs and other financial obligations, age (you should typically be under 60 years at the time of loan completion), and employment status. You can use online eligibility calculators to get a rough estimate before applying. For a precise assessment, Construction Estimator India offers a free eligibility check at +91 8630676890.

Step 3: Choose the Right Bank

Don’t just look at the interest rate. Compare the LTV ratio, prepayment charges (usually zero for floating rates), processing fees, and the bank’s reputation for smooth stage-wise disbursement. Top lenders in 2026 include SBI Home Loan, HDFC Ltd., ICICI Bank, Axis Bank, and LIC Housing Finance.

Step 4: Submit Required Documents

You will need a mix of personal and property documents:

- Personal: PAN Card, Aadhaar, and address proof.

- Income: Salary slips for 3–6 months, Form 16/ITR for 2 years, and 6 months of bank statements.

- Property: Allotment letter from the builder, registered Sale Agreement, Project’s RERA number, builder-buyer agreement, payment schedule, and sanctioned plans.

Step 5: Get Loan Sanctioned

After document verification and credit assessment, the bank issues a sanction letter. This letter is a formal offer containing the sanctioned amount, interest rate, tenure, and other terms. It is NOT the actual disbursement, but a promise to lend.

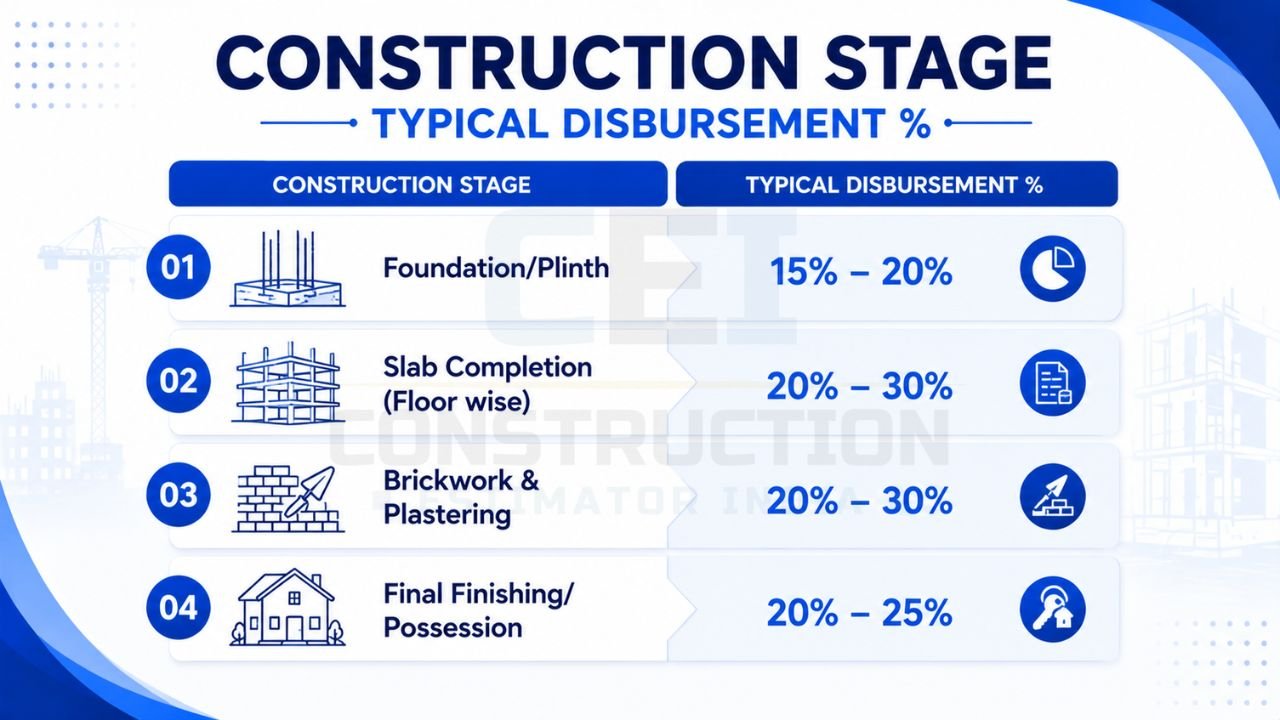

Step 6: Stage-wise Disbursement

Unlike ready-to-move flats, where the full loan amount is disbursed at once, loans for under-construction properties follow a stage-wise disbursement model.

| Construction Stage | Typical Disbursement % |

|---|---|

| Foundation/Plinth | 15% – 20% |

| Slab Completion (Floor wise) | 20% – 30% |

| Brickwork & Plastering | 20% – 30% |

| Final Finishing/Possession | 20% – 25% |

You will need to submit a demand letter from the builder to get each installment released.

Step 7: EMI vs Pre-EMI Payments

During construction, you have two repayment options:

- Pre-EMI: Pay interest only on the disbursed amount. Full EMI starts after construction is completed or full disbursement is made.

- Full EMI: Start the full EMI (Principal + Interest) immediately. This reduces the overall interest burden. The full EMI starts once the construction is completed if you chose the Pre-EMI path earlier.

Step 8: Registration & Possession

Once the builder completes construction and obtains the Occupancy Certificate (OC), you will pay the remaining dues, register the property in your name, and take possession. At this point, any Pre-EMI arrangement ends, and the loan transitions into a standard EMI-based repayment.

👉 Simplify Your Home Loan Process with Professional Financial Guidance.

Pre-EMI vs Full EMI: Which Option Is Better for You?

Understanding Pre-EMI

Pre-EMI is the interest paid on the portion of the loan disbursed by the bank. For example, if your sanctioned loan is ₹50 Lakhs but only ₹10 Lakhs is disbursed, and the interest rate is 8.5%, your Pre-EMI would be approximately ₹7,083 per month. This is ideal for buyers who are currently paying rent and cannot afford a full EMI of ₹40,000+ simultaneously.

Understanding Full EMI

Under this option, you start paying the EMI on the entire sanctioned amount from day one, even if the builder hasn’t received the full money. While this puts a strain on your monthly budget, the principal component of your loan starts reducing immediately. This can save you lakhs of rupees in interest over the 20-year tenure.

Comparative Analysis

| Feature | Pre-EMI | Full EMI |

|---|---|---|

| Monthly Outgo | Lower (Interest only) | Higher (Principal + Interest) |

| Principal Repayment | Starts only after possession | Starts immediately |

| Total Interest Cost | Higher (Longer duration) | Lower (Principal reduces early) |

| Best For | People paying rent | People with high disposable income |

Cost Impact: Choosing Pre-EMI for a 3-year construction period on a ₹50 Lakh loan can increase your total interest cost by approximately ₹10–12 Lakhs compared to starting Full EMI immediately. Construction Estimator India provides a free Pre-EMI calculation at +91 8630676890 to help you decide.

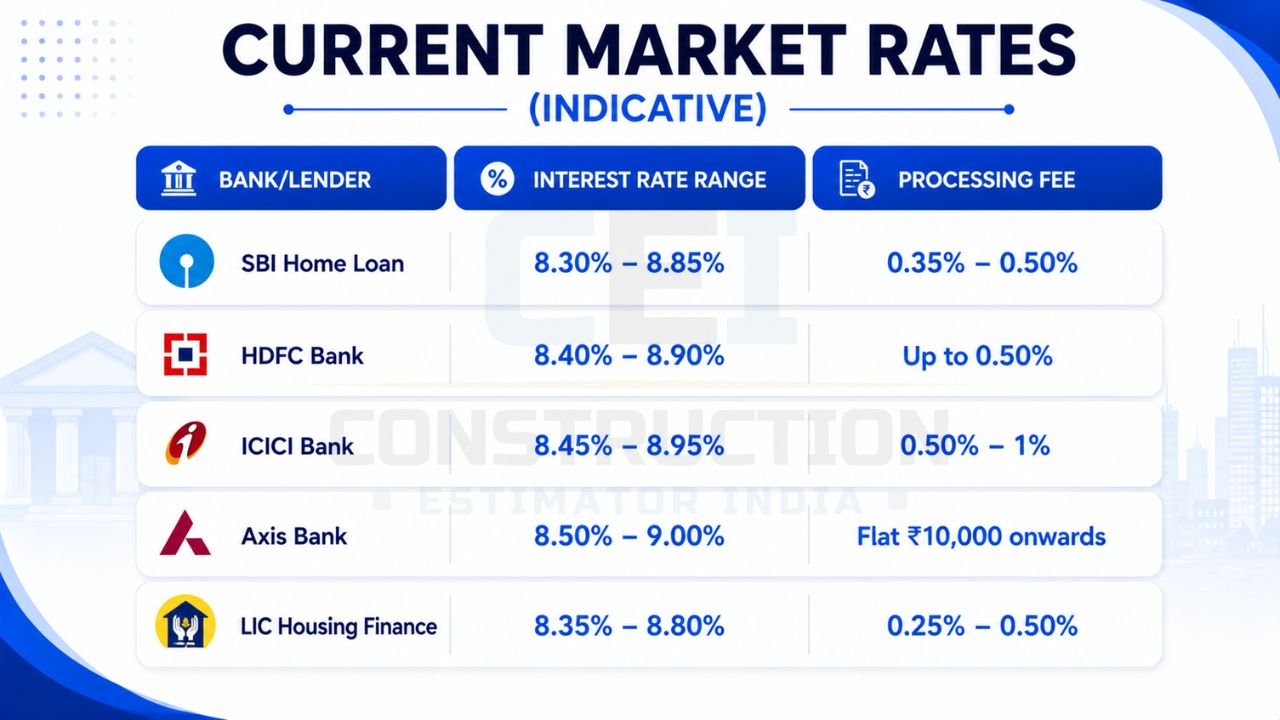

Home Loan Interest Rates for Under Construction Property 2026

Interest rates in 2026 remain competitive as banks compete for high-quality borrowers. Most banks offer “Floating Rates” linked to the Repo Rate, meaning your interest can change if the RBI modifies its policy.

Current Market Rates (Indicative)

| Bank/Lender | Interest Rate Range | Processing Fee |

|---|---|---|

| SBI Home Loan | 8.30% – 8.85% | 0.35% – 0.50% |

| HDFC Bank | 8.40% – 8.90% | Up to 0.50% |

| ICICI Bank | 8.45% – 8.95% | 0.50% – 1% |

| Axis Bank | 8.50% – 9.00% | Flat ₹10,000 onwards |

| LIC Housing Finance | 8.35% – 8.80% | 0.25% – 0.50% |

Floating vs Fixed Rates

While fixed rates offer certainty, they are usually 1–2% higher than floating rates. In 2026, over 95% of Indian homebuyers opt for floating rates because there are no prepayment penalties, allowing them to close the loan early using bonuses or savings.

👉 Secure the Best Financing Option for Your Dream Home.

Tax Benefits on Home Loan for Under Construction Property

The tax treatment for under-construction properties is unique and often misunderstood. A home loan for under-construction property can get tax deductions up to ₹2 Lakhs on interest paid in a year and up to ₹1.5 Lakhs for principal paid. However, there is a catch.

The “Completion” Rule

Income tax benefits on home loans are not available for under-construction properties. You can only avail the tax exemptions after the construction is complete. If you pay interest during 2024, 2025, and 2026 while the building is under construction, you cannot claim it in those years’ tax returns.

Claiming Pre-Construction Interest

You can avail the tax benefits on the interest paid during the construction in 5 equal installments starting from the year construction is completed.

- Section 24(b): Interest deduction up to ₹2 Lakhs (includes current year interest + 1/5th of pre-construction interest).

- Section 80C: Principal repayment up to ₹1.5 Lakhs (Note: Principal paid during construction is generally not eligible for deduction; only payments made after completion qualify).

Crucial Warning: If the construction takes longer than 5 years from the end of the financial year in which the loan was taken, the interest deduction under Section 24 is capped at only ₹30,000 instead of ₹2 Lakhs.

Loan Eligibility: How Much Home Loan Can You Get?

Your eligibility is the foundation of your home-buying journey. Banks use a “Fixed Obligation to Income Ratio” (FOIR) to decide your limit. Usually, banks don’t want your total EMIs to exceed 50–60% of your net monthly income.

Factors Affecting Eligibility

- Income: Higher stable income leads to higher loan amounts.

- Credit Score: A score above 750 often gets you the lowest interest rates.

- LTV Ratio: You can typically get 75% to 90% of the construction cost as a loan. For properties above ₹75 Lakhs, the LTV is usually capped at 75%.

- Age: A 30-year-old can get a 30-year tenure, while a 50-year-old might only get a 10-year tenure, reducing the loan amount.

Example Calculation

If your monthly take-home is ₹1,00,000 and you have no other loans, the bank might allow an EMI of ₹50,000. At an 8.5% interest rate for 20 years, this qualifies you for a loan of approximately ₹58 Lakhs. For a personalized analysis, contact Construction Estimator India for a free property financial analysis at +91 8630676890.

Costs: Processing Fees, Prepayment Charges & Other Expenses

The “Agreement Value” of the flat is not your only cost. You must budget for several additional expenses:

- Processing Fees: Usually 0.50% to 1% of the loan amount. Some banks offer waivers during festive seasons.

- Prepayment Charges: As per RBI guidelines, there are no prepayment charges for floating-rate home loans for individual borrowers.

- Legal & Technical Fees: Banks charge ₹3,000 to ₹10,000 to verify the property’s legal title and construction progress.

- MODT (Memorandum of Deposit of Title Deed): A government tax on the loan agreement, ranging from 0.1% to 0.5% depending on the state.

- Insurance: Lenders often insist on Mortgage Guarantee Insurance or Term Insurance to cover the loan amount.

Benefits of Buying Under Construction Property with Home Loan

-

Price Advantage: These properties are often cheaper than ready-to-move homes, sometimes by 10% to 20%. Knowing the local house construction per sq ft rate ensures you pick an affordable, asset-growing development.

- Staggered Payments: With flexible payment structures, you don’t need the full capital upfront. You pay as construction progresses.

- Lower Interest Outgo: Some lenders only charge the EMIs on the amount disbursed, keeping your initial costs low.

- Modern Amenities: Newer projects usually come with the latest technology, better energy efficiency, and modern lifestyles.

- Customization: You can often request minor changes in flooring or electrical layouts while the building is being constructed.

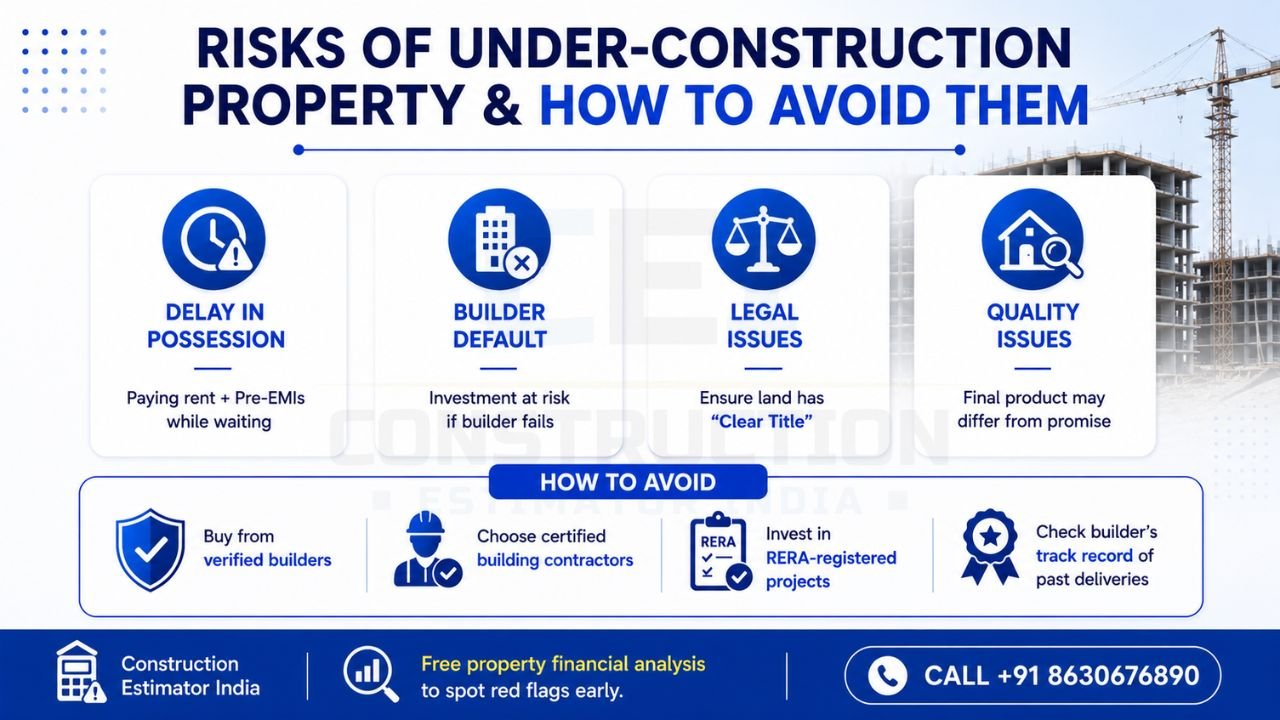

Risks of Under Construction Property & How to Avoid Them

The primary risk is the delay in possession. A delayed project means you continue paying rent and Pre-EMIs while losing out on tax benefits.

- Builder Default: If the builder goes bankrupt, your investment is at risk. Always turn to your lender for help with property analysis as they have the resources to check a builder’s financial health.

- Legal Issues: Ensure the land has a “Clear Title.”

- Quality Issues: The final product might differ from the sample flat.

Solution: Only buy from verified builders who employ certified building contractors in RERA-registered projects. Check the builder’s track record of past deliveries. Construction Estimator India provides free property financial analysis to help you spot red flags early. Call +91 8630676890.

👉 Need Help with a Home Loan? Connect with Our Experts Today.

When to Contact Construction Estimator India for Home Loan Help

Navigating the 2026 home loan market requires more than just an online search. You need an expert who understands the local nuances of Indian real estate. If you require subsequent structural layout overhauls via a house renovation or simply a baseline check, you should reach out to us if:

- You are confused between Pre-EMI and Full EMI.

- You want to know your maximum loan eligibility without affecting your credit score.

- You need a detailed cost-benefit analysis of an under-construction project.

- You want to compare the latest interest rates from 15+ banks in one go.

Contact Construction Estimator India via WhatsApp or Call at +91 8630676890. We offer:

- Free Home Loan Eligibility Check

- Free Pre-EMI vs Full EMI Calculation

- Free Property Financial Health Analysis

FAQs

Q1: What is a home loan for under construction property?

It is a loan for a residential property that is still being built. The bank releases money in stages to the builder rather than in one lump sum.

Q2: How is the loan disbursed for under construction property?

It is disbursed in “tranches” based on construction milestones (e.g., plinth, 1st floor slab, brickwork).

Q3: What is Pre-EMI and when do I pay it?

Pre-EMI is the interest paid only on the disbursed amount during the construction phase. You pay it monthly until construction is complete.

Q4: Should I choose Pre-EMI or Full EMI during construction?

Choose Pre-EMI if you have tight cash flow (e.g., paying rent). Choose Full EMI if you want to reduce your total interest cost and close the loan faster.

Q5: When does full EMI start for under construction property?

It typically starts after the property is completed and the full loan amount is disbursed.

Q6: Can I claim tax benefits during the construction period?

No, tax benefits can only be claimed after the construction is complete and you have the completion certificate.

Q7: How do I claim tax benefits after construction completion?

You can claim the interest paid during construction in 5 equal yearly installments starting from the year of completion.

Q8: What is the loan-to-value (LTV) ratio?

It is the percentage of the property value the bank will fund. It usually ranges from 75% to 90%.

Q9: What documents are required?

Income proof (salary slips, ITR), personal ID (Aadhaar, PAN), and property documents (allotment letter, builder-buyer agreement).

Q10: Which banks offer home loans for under construction flats?

Major banks like SBI, HDFC, ICICI, Axis, and LIC Housing Finance are top providers.

Q11: What are the risks?

Project delays, builder insolvency, and construction quality issues. Always check RERA registration.

Q12: How do I contact Construction Estimator India?

You can Call or WhatsApp us at +91 8630676890 for expert assistance.

Contact Construction Estimator India for Property Financial Services

At Construction Estimator India, we bridge the gap between your dream home and the complex world of finance. Our team of experts provides end-to-end support for homebuyers across India.

Our Specialized Services Include:

- Free Home Loan Eligibility Check: Know exactly how much you can borrow before you start house hunting.

- Free Pre-EMI Calculation: Get a month-by-month breakdown of your interest obligations.

- Free Property Financial Analysis: We evaluate the builder’s payment plan and the project’s financial viability.

Connect with us today:

- WhatsApp/Call: +91 8630676890

Don’t let financial jargon stop you from making the best investment of your life. Let Construction Estimator India simplify the process for you.

Conclusion: Smart Investment with Under Construction Property Home Loan

Buying an under-construction flat can be a smart investment—often cheaper than ready-to-move homes and with flexible payment structures. While the process involves more stages than buying a ready home, the financial flexibility it offers is unmatched. A home loan for an under-construction property is just like any other home loan — but disbursed in stages, not all at once.

By leveraging stage-wise disbursement (Foundation 15–20%, Slab 20–30%, Brickwork 20–30%, Finishing 20–25%), you ensure your money is used productively. While you cannot claim tax benefits immediately, the ability to claim pre-construction interest in 5 equal installments after completion offers significant long-term savings. With LTV ratios allowing you to get 75% to 90% of the construction cost as a loan, your dream of homeownership is closer than ever.

Take the first step today. Construction Estimator India offers a free home loan eligibility check at +91 8630676890. Invest wisely, plan financially, and build your future on a solid foundation.