Imagine you are a plumbing contractor in Meerut, Uttar Pradesh, working on a premium bathroom renovation. You’ve just installed a high-end wall-hung WC and a multi-way diverter. Suddenly, a joint fails overnight while you are off-site, flooding the client’s new Italian marble flooring and causing structural seepage in the flat below. Without proper coverage, you could be facing a repair bill of over ₹1 lakh—a massive out-of-pocket expense that could wipe out your profits for months. Knowing what insurance do you need as a plumber is the only way to protect your business from such unexpected financial disasters.

As a plumber in 2026, whether you are a solo freelancer, a small plumbing business owner, or a contractor managing a team in Delhi-NCR, you face unique daily risks. These include extensive water damage to client property, the theft of expensive tools, injuries in confined spaces, and even legal claims regarding faulty workmanship or design errors. Many professionals wrongly assume that their personal health insurance or vehicle insurance covers their business activities. In reality, you need a specific mix of personal, professional, and business insurance to safeguard your livelihood. This guide explores the essential insurance for plumbers in India, realistic 2026 costs, and how to include these premiums in your job quotes to ensure you remain profitable and protected.

Why Plumbers Specifically Need Insurance?

Plumbing is inherently high-risk because you deal with the one element that can cause the most silent and expensive damage: water. A single improperly tightened fitting or a miscalculated pipe slope can lead to structural compromises or mold issues that appear months later. In the dense urban environments of cities like Noida or Ghaziabad, a leak in one apartment doesn’t just affect your client; it impacts third parties in the units below.

Beyond physical damage, you are at risk of tool theft—a growing concern on active construction sites where drilling machines and pipe cutters are frequently left unattended. Furthermore, legal liability in India is becoming stricter. With the enforcement of the Building and Other Construction Workers (BOCW) Act and increased consumer awareness, clients are more likely to seek legal recourse for perceived professional negligence. Without insurance, your personal assets—including your savings and vehicle—could be at stake to settle a claim.

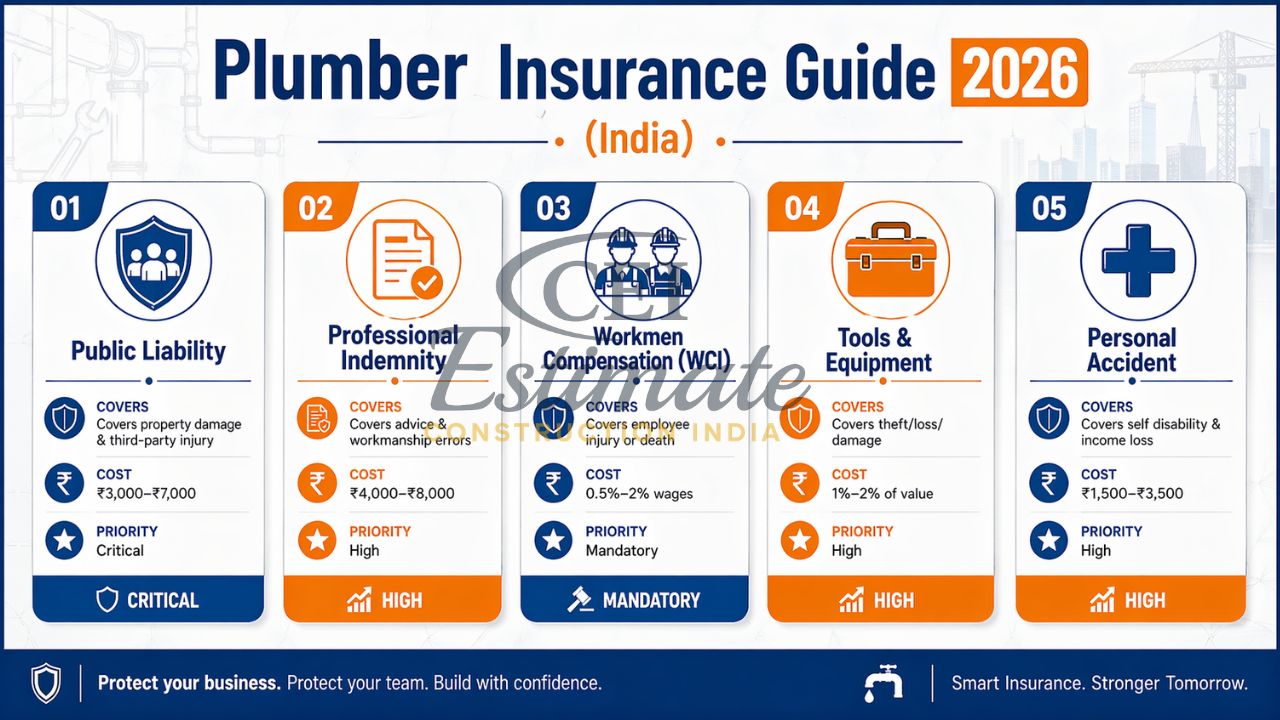

1. Public Liability Insurance (Most Important for Plumbers)

Public liability insurance for plumbers is widely considered the most critical policy for anyone in the trade. This insurance protects you if your work causes accidental injury to a third party or damage to their property. For a plumber, this typically covers scenarios like accidental flooding or a visitor tripping over your tool kit on a site.

In the Indian context, if you are working in a high-rise residential complex and a pipe burst during a pressure test damages the elevator system or a neighbor’s expensive woodwork, this policy steps in to cover the repair costs and any legal fees. Typical coverage limits for small contractors range from ₹5 lakhs to ₹25 lakhs, depending on the scale of projects you handle. It provides the “peace of mind” that a single mistake won’t lead to bankruptcy.

2. Professional Indemnity Insurance

While public liability covers accidental damage, professional indemnity insurance for plumbers covers claims arising from professional negligence, faulty workmanship, or errors in your advice. For example, if you provide the design for a complex drainage system and the pipe sizing is incorrect—leading to frequent blockages and requiring a total rework—the client can sue for financial loss.

In 2026, as more plumbers transition into “design-build” services for independent villas in tier-2 cities, this cover is essential. It protects you against:

- Errors in technical drawings or BOQs (Bill of Quantities).

- Loss of client documents or data.

- Claims of professional negligence that result in financial damage to the client even without physical injury.

3. Workmen Compensation Insurance / Group Personal Accident

If you employ helpers or junior plumbers, workmen compensation for plumbing contractors is a statutory mandate under the Employees’ Compensation Act, 1923. You are legally liable to pay compensation if a worker suffers an injury, disability, or death while on duty.

For a plumbing business, premium rates for Workmen Compensation Insurance (WCI) typically range from 0.5% to 2% of your total wage bill. If you are a solo freelancer without employees, you should prioritize a Group Personal Accident (GPA) or a standalone Personal Accident policy. For a very low cost, you can also facilitate government-backed schemes like the Pradhan Mantri Suraksha Bima Yojana (PMSBY), which provides ₹2 lakh accidental death cover for just ₹20 per year.

4. Tools and Equipment Insurance

Your tools are your livelihood. Expensive equipment like high-pressure jetting machines, thermal imaging cameras for leak detection, and heavy-duty pipe threaders are significant investments. Tools and equipment insurance for plumbers (often part of a Contractors Plant & Machinery or CPM policy) protects these items against theft, fire, and accidental damage on-site or while in transit.

In North India, where site security can vary greatly between projects, having your drill machines and testing kits insured ensures you can replace them quickly without a major financial hit. Most policies require you to maintain an updated inventory of your tools with their purchase values to ensure a smooth claims process.

5. Other Important Insurance for Plumbers

To build a truly resilient best insurance for plumbing business portfolio, consider these additional covers:

- Personal Accident Insurance: Since you are the engine of your business, this provides income replacement if you are injured and unable to work.

- Health Insurance (Mediclaim): Essential for covering hospitalization costs due to illnesses unrelated to work.

- Vehicle Insurance: If you use a van or bike to transport materials, ensure it has “commercial use” coverage, as standard private insurance may reject claims during work trips.

- Cyber Liability: If you store client data or offer “Smart Home” plumbing solutions (like IoT leak sensors), this protects against data breaches and digital errors.

What Insurance Do You Need as a Plumber? (Comparison)

Choosing the right coverage requires balancing your specific risks with your budget. Use the table below to prioritize your insurance needs for 2026.

| Insurance Type | What it Covers | Who Needs It | Approx. 2026 Cost (Annual) | Priority Level |

|---|---|---|---|---|

| Public Liability | Property damage & third-party injury | All Plumbers | ₹3,000 – ₹7,000 | Critical |

| Professional Indemnity | Advice, design, & workmanship errors | Design-Build Contractors | ₹4,000 – ₹8,000 | High |

| Workmen Comp (WCI) | Employee injury or death | Contractors with teams | 0.5% – 2% of wages | Mandatory |

| Tools & Equipment | Theft, loss, or damage to tools | All Plumbers | 1% – 2% of tool value | High |

| Personal Accident | Self-disability & income loss | Solo/Freelancers | ₹1,500 – ₹3,500 | High |

How Much Insurance Costs for a Plumber in India?

The cost of insurance for plumbers in 2026 is surprisingly affordable when compared to the potential risks. For a solo plumber in a city like Meerut, a basic package covering public liability and personal accident can cost as little as ₹5,000 to ₹8,000 per year. For a small plumbing company with 3–5 helpers and a total annual wage bill of ₹15 lakhs, the total insurance and compliance cost (including WCI and tools) might range from ₹25,000 to ₹45,000 annually.

Several factors influence these premiums:

- Scope of Work: Working on high-rise residential towers or industrial plants attracts higher premiums than minor home repairs.

- Location: Projects in seismic Zone IV/V (like Delhi-NCR) may have slightly higher rates for property damage.

- Claims History: Maintaining a “clean” record without previous accidents can help you negotiate better rates with insurers.

Step-by-Step Guide to Buying Insurance as a Plumber

Navigating the insurance market in 2026 is faster thanks to digital platforms. Follow these steps to get protected:

- Assess Your Risks: Determine the maximum value of property you could potentially damage and the number of workers you need to cover.

- Choose Your Sum Insured: Never under-insure to save money; ensure the coverage limit reflects current 2026 repair and medical costs.

- Compare Quotes: Use aggregators or visit portals of reputable providers like HDFC Ergo, ICICI Lombard, New India Assurance, or Go Digit.

- Check for “Maintenance Period” Riders: Ensure your policy covers leaks or defects that appear after the job is handed over.

- Review Exclusions: Understand what is not covered (e.g., intentional damage or working under the influence).

How to Include Insurance Costs in Your Plumbing Quotes?

One of the biggest mistakes small contractors make is absorbing insurance costs into their profit margin. You must treat insurance as a legitimate business expense. When preparing a plumbing detailed estimate template, include insurance as a specific line item under “Preliminaries” or “Statutory Compliance”.

Typically, you should add 1% to 2% of the total project value to cover insurance and safety overheads. When you explain to the client that this fee protects their home from accidental damage, most will appreciate your professionalism and be willing to pay the premium.

Conclusion

In the fast-paced construction environment of 2026, the question of what insurance do you need as a plumber is central to your professional reputation and financial stability. From public liability that shields you against accidental flooding to Workmen Compensation that protects your team, these policies form the invisible safety harness for your business. Being “insured and assured” is what separates a professional contractor from a risky freelancer.

Don’t wait for a site disaster to realize the value of protection. Secure your business today and ensure your career remains leak-proof. For professional help with job costing, BOQs, and ensuring every insurance expense is accurately factored into your bids, contact Construction Estimator India today. Let’s build a safer, more profitable future for your plumbing business.

FAQ Section

What insurance do you need as a plumber in India?

In India, you primarily need Public Liability, Professional Indemnity, and Workmen Compensation (if you have employees). Solo plumbers should also have Personal Accident insurance.

Is public liability insurance mandatory for plumbers?

While not always a legal requirement for private residential work, it is often mandatory for commercial contracts, government tenders, and projects in RERA-registered buildings.

How much does insurance cost for a plumber?

For a solo plumber, basic cover starts around ₹5,000/year. Small businesses may pay between ₹20,000 and ₹50,000 depending on the number of workers and tool values.

What is professional indemnity insurance for plumbers?

It covers you if a client sues for financial losses caused by your professional errors, such as incorrect pipe sizing, faulty design, or poor technical advice.

Does workmen compensation cover helpers?

Yes, Workmen Compensation Insurance (WCI) is specifically designed to cover medical costs and compensation for any laborer or helper injured while working under you.

How to insure my plumbing tools and equipment?

You can buy a “Contractors Plant & Machinery” (CPM) policy or a “Portable Equipment” cover. You must provide a list of tools with their current market value.

Can a freelance plumber buy insurance easily?

Yes, most Indian insurers now offer digital portals where freelance tradespeople can buy public liability and personal accident cover in minutes using their Aadhaar and PAN cards.

What happens if I damage a client’s property?

If you have Public Liability insurance, the insurer will handle the legal claim and pay for the repairs (up to your policy limit), protecting you from huge personal losses.

How to add insurance cost to my plumbing quotations?

Add a separate line item labeled “Insurance & Safety Compliance” in your BOQ. Calculate it as 1-2% of the total labor and material cost.

Which insurance company is good for plumbers in India?

Top providers for 2026 include ICICI Lombard, HDFC Ergo, New India Assurance, and Go Digit, known for their quick digital claims and specialized trade policies.