Imagine you are a self-building homeowner in Meerut, Uttar Pradesh, having finally saved enough to construct your dream three-story residence. By July 2026, the structure is 60% complete, with premium electrical conduits and expensive Teak wood frames installed. Suddenly, an unprecedented monsoon downpour triggers a localized flash flood that submerges the ground floor and collapses an unfinished boundary wall, ruining thousands of bags of cement stored on-site. You might assume your future home insurance will handle this, but without specific insurance for building under construction, you could face a financial setback of years.

Standard home insurance policies in India, like the Bharat Griha Raksha, are designed strictly for occupied, completed dwellings and explicitly exclude properties that are still under development. This gap is filled by specialized insurance for building under construction, often referred to as Builders Risk Insurance or a core component of a Contractors All Risk (CAR) policy. It acts as a vital safety net, protecting the physical anatomy of your project—including raw materials, temporary works like scaffolding, and even third-party liabilities—during its most vulnerable state.

For anyone managing a self-construction project in regions like the Delhi-NCR or preparing a Bill of Quantities (BOQ), understanding this insurance is critical for accurate project costing. This guide will explore the nuances of coverage, 2026 cost benchmarks, and why every Indian construction project needs this robust shield. By the end, you will know exactly how to protect your investment from the ground up.

Why Standard Home Insurance Does Not Cover Buildings Under Construction?

A common misconception among first-time builders in India is that home insurance starts the day the first brick is laid. However, IRDAI guidelines for standard products like “Home Secure” or Bharat Griha Raksha are clear: they are only for completed, ready-to-live-in dwellings. These policies typically require a completion certificate or for the building to be fit for habitation before coverage becomes effective.

The reasons for this exclusion are grounded in risk assessment. An active site is a high-risk environment characterized by a lack of security like doors and windows, making it prone to material theft. Furthermore, without a finished roof or waterproof plastering, the structure is highly susceptible to weather damage. The constant presence of laborers and heavy machinery also introduces third-party liability risks that standard homeowner policies aren’t priced to handle. If you attempt to file a claim for a collapsed wall or stolen copper wiring under a standard home policy, it will likely be rejected because the “nature of the risk” has fundamentally changed from the policy’s intent.

What is Insurance for Building Under Construction?

At its heart, insurance for building under construction is a comprehensive safety net for “work-in-progress”. It provides specialized protection for the physical project from the moment of groundbreaking until the final handover or the issuance of a completion certificate. In the Indian residential market, this is most commonly obtained through a Contractors All Risk (CAR) policy or Builders Risk Insurance.

These terms are often used interchangeably in the 2026 market. While “Contractor All Risk” typically emphasizes the builder’s liability, “Builders Risk Insurance” or “Property in Course of Construction” (PCOC) focuses on the project assets. Regardless of the name, the core philosophy is “all-risk,” meaning it covers all sudden and unforeseen physical loss or damage except for what is specifically excluded. This policy treats the site as a dynamic environment, protecting the permanent structure, construction materials (like steel and cement), and temporary works like site offices and formwork.

What Does Insurance for Building Under Construction Cover?

The core value of this insurance lies in the exhaustive list of protected risks within the CAR framework. In the context of 2026 Indian residential construction, especially in volatile weather zones like North India, these covers are indispensable.

Physical Damage to Works and Materials

This is the primary shield covering the actual permanent structure (walls, slabs, foundations) and temporary works.

- Fire and Natural Perils: Protection against fire, lightning, and explosions, as well as “Special Perils” like monsoonal floods, cyclones, and earthquakes.

- Theft and Burglary: Specifically covers the theft of raw materials like TMT bars and copper wiring on-site, provided there is evidence of housebreaking.

- Structural Failures: Covers the cost of clearing debris and rebuilding if a slab or wall collapses due to soil shifts or unexpected events.

Third-Party Liability

A critical but often overlooked component, this covers legal and compensatory costs if your site activities accidentally cause bodily injury to a passerby or damage a neighbor’s property. This prevents your project from being derailed by expensive litigation.

Maintenance and Testing Period

Most policies include a “maintenance period” (usually 12 months post-handover) to cover defects or damage discovered shortly after the project is completed.

Popular Add-ons and Riders

- Escalation Clause: Automatically increases the sum insured to account for rising material costs like steel and cement during a long build.

- Debris Removal: Covers the cost of hauling away ruins after a major fire or structural collapse.

- Architect and Surveyor Fees: Pays for professional fees required to plan repairs after an insured loss.

Major Exclusions You Must Know

While “all-risk” sounds all-encompassing, it does not cover every scenario. To ensure a successful claim, you must be aware of these standard 2026 exclusions:

- Faulty Workmanship and Design: The insurance will not pay to fix a wall built crookedly or a slab that cracked due to an incorrect cement ratio.

- Willful Negligence: Intentional violation of safety norms or leaving expensive materials in an unsecured open field can lead to claim rejection.

- Normal Wear and Tear: Gradual deterioration, such as rusting of steel left in the rain for months or natural erosion, is generally not covered.

- War and Nuclear Risks: Universal exclusions for losses arising from war or nuclear radiation.

- Penalties for Delay: The policy covers repair costs but not the penalties you might owe for missing project deadlines.

- Inventory Shortages: You cannot claim for materials that simply “go missing” during an audit; evidence of a specific theft event is required.

Who Needs Insurance for Building Under Construction?

If you are an individual homeowner building an independent floor or villa, you need this insurance to protect your life savings. Similarly, small-scale contractors taking on “material + labor” contracts need it to protect their profit margins from site disasters. Real estate developers in India are often mandated by RERA to maintain insurance for the project until handover.

While not strictly mandatory by law for all private builds, insurance for building under construction India is almost always mandated by banks and NBFCs for construction-linked home loans. Lenders require it to ensure their collateral is protected against total loss. Even if you are self-funding, the rising costs of labor and materials in 2026 make this a logical requirement for any sensible project manager.

How Much Does Insurance for Building Under Construction Cost in India?

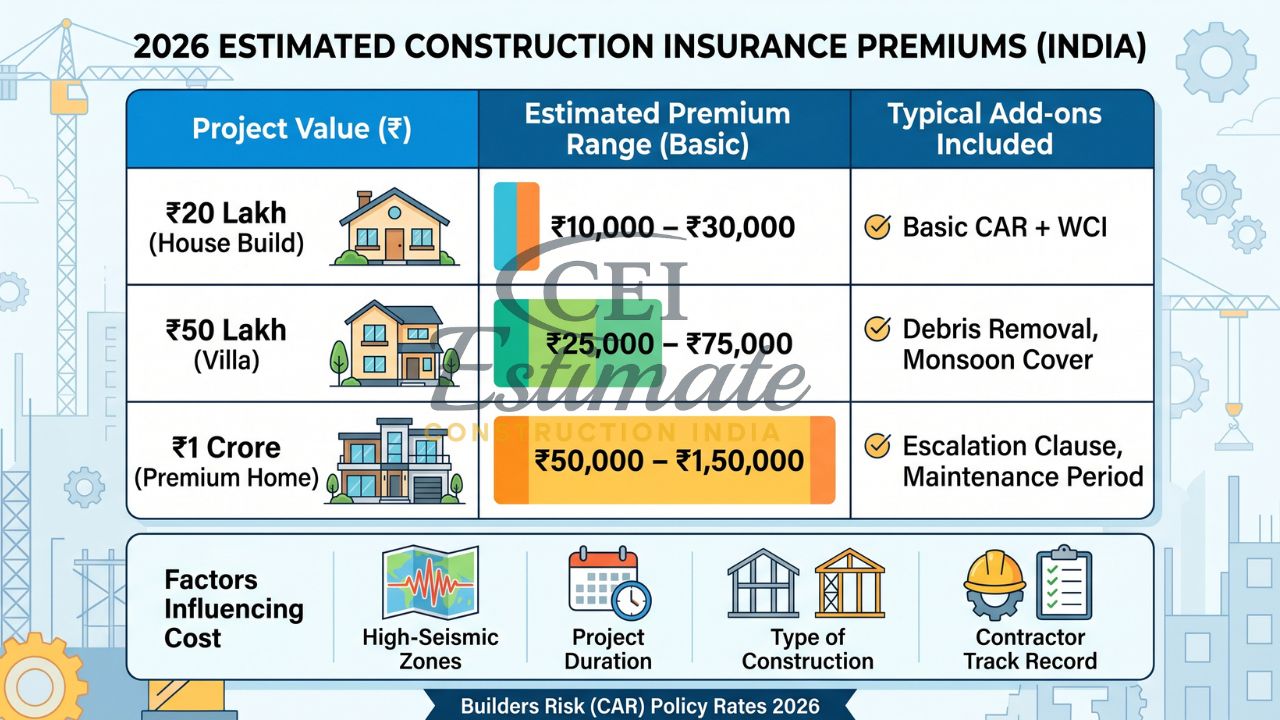

The cost of insurance for building under construction 2026 is surprisingly affordable given the peace of mind it provides. Generally, the premium for a CAR or Builders Risk policy ranges from 0.5% to 1.5% of the total project value. For a residential project in Meerut with an estimated construction cost of ₹80 Lakhs, the annual premium might range between ₹40,000 and ₹1,20,000, depending on risk factors.

Several factors influence this cost:

- Project Location: Building in a high-seismic zone like Delhi-NCR or a flood-prone area in UP will attract higher premiums.

- Duration: A policy for a 12-month build is naturally cheaper than one for a 36-month high-rise project.

- Type of Construction: RCC frame structures are often viewed as lower risk than those involving significant timber or steel frames.

- Contractor Track Record: Firms with a history of safe sites and zero claims can often negotiate more competitive rates.

Sample 2026 Premium Ranges

| Project Value | Estimated Premium Range (Basic) | Typical Add-ons Included |

|---|---|---|

| ₹20 Lakh (House Build) | ₹10,000 – ₹30,000 | Basic CAR + WCI |

| ₹50 Lakh (Villa) | ₹25,000 – ₹75,000 | Debris Removal, Monsoon Cover |

| ₹1 Crore (Premium Home) | ₹50,000 – ₹1,50,000 | Escalation Clause, Maintenance Period |

Step-by-Step Guide to Buying Insurance for Building Under Construction

- Define the Sum Insured: Use the “Total Contract Value,” which includes materials, labor, and professional fees. Do not include land value.

- Gather Documents: Prepare the project site address, building plans/drawings, estimated construction schedule, and contractor details.

- Choose the Right Policy: Decide between a standalone Builders Risk policy or a comprehensive CAR policy based on project complexity.

- Compare Quotes: Obtain at least three quotes from major Indian insurers like New India Assurance, HDFC Ergo, or ICICI Lombard.

- Review Add-ons: Ensure you include critical riders like the escalation clause and third-party liability.

- Finalize the Policy: Ensure the policy is in the “Joint Names” of the owner, contractor, and lender (if applicable).

When to Switch from Construction Insurance to Building Insurance?

The transition from construction-phase insurance to post-completion building insurance is a critical “switch point”. You should purchase building insurance for a new build—typically a Bharat Griha Raksha policy—precisely when the construction risk ends. This usually occurs once you receive the Occupancy Certificate (OC) or Completion Certificate (CC) from your local authority, such as the MDA in Meerut.

Delaying this switch is dangerous. If a fire occurs during the gap between the last contractor leaving and the family moving in, a claim could be rejected if you haven’t switched policies, as the nature of the risk has changed. Ensure your new building insurance is ready to kick in the day your construction policy expires.

How Estimators Should Include This Insurance in Project Costing?

For any project to be successful, financial planning must be as sturdy as the foundation. As an expert at Construction Estimator India, I advocate for the inclusion of insurance for building under construction premiums as a distinct line item in every accurate BOQ and tender document.

Listing insurance under “Preliminaries” or “Project Overheads” demonstrates professionalism and ensures these “soft costs” don’t erode your profit margins. By factoring in these costs early, you protect your client from 100% loss if a calamity strikes. Always use actual market quotes rather than historical data to ensure your bid is both competitive and secure.

Conclusion

Building a home in India is one of the most significant investments you will ever make. From the humid plains of Uttar Pradesh to the seismic zones of Delhi-NCR, the risks of construction are ever-present. Proper insurance for building under construction is not just an added expense; it is the invisible foundation of your project’s financial security. By choosing the right CAR insurance and accurately factoring these costs into your initial estimates, you ensure your dream home survives the construction phase to become a reality.

Don’t leave your project’s future to chance. Arrange the right coverage early and contact Construction Estimator India for professional BOQ and construction cost estimation services that accurately include insurance for building under construction based on 2026 market rates.

FAQ Section

What is insurance for building under construction in India?

It is a specialized policy, usually a Contractors All Risk (CAR) or Builders Risk policy, that protects a building structure, raw materials, and temporary works from damage or theft while it is being constructed.

Can I use normal home insurance for a building under construction?

No. Standard home insurance (Bharat Griha Raksha) only covers completed and occupied buildings. It excludes properties that are still under construction.

What is the difference between CAR insurance and Builders Risk insurance?

In India, they are often used interchangeably. CAR is generally more comprehensive, including third-party liability and protection for both the owner and contractor.

How much does insurance for building under construction cost?

Typically, the premium ranges from 0.5% to 1.5% of the total construction cost, depending on location, duration, and project risk factors.

Is insurance mandatory for buildings under construction?

While not always legally mandated for private individuals, it is almost always required by Indian banks for construction-linked home loans and by RERA for developer projects.

What is covered under CAR policy for house construction?

It covers damage from fire, natural calamities (floods, earthquakes), theft of materials, structural collapse, and third-party liability for injury or property damage.

When should I buy insurance for my new build?

You should purchase the policy before groundbreaking or as soon as materials start arriving at the site.

How is sum insured calculated for under construction building?

It is calculated based on the “Total Contract Value,” which includes materials, labor, and professional fees, excluding the land value.

Can self-build homeowners get construction insurance easily?

Yes, individual homeowners can purchase these policies to protect their investment, even if they are managing the project themselves.

How do I include this insurance cost in my BOQ?

List it as a specific line item under “Project Overheads” or “Preliminaries” based on actual current market quotes.