Imagine you are a homeowner in Meerut or Noida who has just finished a three-story dream residence. You find yourself staring at a dozen different insurance tabs on your browser, wondering which policy truly secures your investment. Every insurer claims to be the best, but their terms look like a maze of legal jargon. Knowing how to choose building insurance is not just about finding the lowest premium; it is about ensuring that if a disaster strikes, you have the financial means to rebuild. Whether you are an individual builder, an apartment owner, or a rental property investor, selecting the right building insurance (also known as home structure or dwelling insurance) is one of the most critical financial decisions for protecting your biggest physical asset.

As construction costs in India continue to rise in 2026, understanding how to choose building insurance allows you to navigate the nuances of reinstatement values and seismic risks in North India. This guide will walk you through a clear, seven-step process to select the best building insurance for new builds, apartments, and mortgaged homes. We will explore how this choice directly impacts your project budget, project viability, and long-term peace of mind. By the end of this article, you will have a practical roadmap to selecting the best building insurance India 2026 has to offer, tailored to your specific property needs.

Understand What Building Insurance Actually Covers

Before diving into the selection process, you must understand the “bricks and mortar” nature of this coverage. Building insurance is specifically designed to protect the “immovable” components of a property—the foundation, walls, roof, floors, and permanent fixtures. If you were to turn your house upside down and shake it, everything that stays attached is what this insurance protects. This includes concealed plumbing, electrical wiring, built-in kitchen cabinets, and even Italian marble flooring.

It is vital to differentiate this from contents insurance. Building insurance protects the “shell,” while contents insurance covers movable items like furniture, electronics, and jewelry. For a comprehensive shield, many Indian homeowners opt for a “package policy” that combines both, but as a builder or estimator, your primary focus must remain on the structure to protect the capital investment. Standard policies in 2026 provide coverage against “Fire and Special Perils,” which includes natural calamities like floods, earthquakes, and storms.

Step 1: Assess Your Specific Needs

The first step in how to choose building insurance is evaluating the unique anatomy of your property. A homeowner in a seismic zone like Delhi-NCR or Meerut (Zone IV/V) has different risk priorities than someone in a coastal region. You must ask:

- Is it a new build? If your home is still under construction, you need a “Contractors All Risk” (CAR) policy first, switching to building insurance only upon receiving your completion certificate.

- Is it an apartment? In a multi-story setup, the RWA typically manages a master building policy for the shell, but you may still need flat insurance for your internal structure and fixtures.

- Is it an investment or rental property? Landlords need specialized policies that include “Loss of Rent” add-ons to protect their cash flow.

- Is it mortgaged? Banks like SBI or HDFC mandate building insurance to protect their collateral. Ensure your policy meets their specific structural requirements.

Step 2: Decide the Right Sum Insured – The Core of How to Choose Building Insurance

Calculating the “Sum Insured” is where most Indian homeowners fail. You should never insure your home for its market value, which includes the land cost; land does not burn or wash away. Instead, use the sum insured for building insurance based on the “Reinstatement Value”—the actual cost to rebuild the structure from scratch at current 2026 labor and material rates.

To calculate this, use the following formula:

Total Carpet Area (sq. ft.) × Current Construction Rate per sq. ft. = Sum Insured

For example, if high-quality RCC construction in Meerut costs ₹2,500 per sq. ft. and your home is 2,000 sq. ft., your sum insured should be at least ₹50 lakhs. Under-insuring can lead to “pro-rata” settlements where the insurer only pays a fraction of the actual loss. Using a professional Bill of Quantities (BOQ) from an estimator is the most accurate way to determine this value in 2026.

Step 3: Choose the Right Type of Policy

Since 2021, the IRDAI has simplified the landscape through the Bharat Griha Raksha vs other building insurance comparison. The Bharat Griha Raksha (BGR) is a standardized policy that every general insurer in India must offer for residential properties. It is often the best choice for homeowners because it offers:

- Standardized Coverage: Uniform protection against fire, floods, and earthquakes regardless of the insurer.

- Automatic Features: Includes a 10% annual escalation of the sum insured to combat inflation and 20% automatic contents cover without itemization.

- No Underinsurance Penalty: Most BGR policies will not penalize you if your sum insured is within 85% of the actual value.

For larger commercial properties or high-value estates, you might still look at “Standard Fire & Special Perils” (SFSP) policies which allow for more complex customization.

Step 4: Compare Key Features and Add-ons

When selecting your policy, look for tips for selecting home building insurance that focus on “add-ons.” These riders can turn a basic policy into a comprehensive shield.

| Feature / Add-on | Importance for Homeowners | Importance for Landlords |

|---|---|---|

| Escalation Cover | High (protects against rising material costs) | High (ensures ROI is protected) |

| Loss of Rent | Low | Very High (compensates for lost income) |

| Alternative Accommodation | High (pays for your stay during repairs) | Low (covers tenant relocation) |

| Debris Removal | Medium (essential after major collapse) | Medium (standard in BGR) |

| Architect Fees | Medium (covers professional redesign) | Medium (up to 5% standard) |

| Public Liability | High (for injury to visitors/neighbors) | High (covers legal liabilities) |

For North Indian residents, ensuring that “STFI” (Storm, Tempest, Flood, Inundation) and “Earthquake” covers are active is non-negotiable.

Step 5: Compare Insurers and Get Quotes

The final choice of how to choose building insurance providers comes down to trust and claim efficiency. While the BGR policy structure is standardized, the experience varies by insurer. Look for companies with a high Claim Settlement Ratio (CSR) for property insurance in 2026.

- HDFC ERGO: Known for tech-savvy urban homeowners and fast digital processing.

- ICICI Lombard: Excellent for long-term (5-10 year) plans with competitive discounts.

- SBI General: Highly reliable for loan-linked sites and properties in tier-2 cities like Meerut.

- New India Assurance: A PSU giant preferred for high-value estates and government contractors.

Always obtain quotes from at least three providers to ensure your construction estimate reflects the most competitive 2026 market rates.

Step 6: Check Policy Wordings and Exclusions

To avoid “heartbreak” during a claim, you must know what is left out. A building insurance buying guide is incomplete without highlighting standard exclusions. Most policies in 2026 will reject claims related to:

- Wear and Tear: Gradual deterioration, rust, or paint peeling due to age is your maintenance responsibility.

- Willful Negligence: If you ignore a known structural crack or leave a fire unattended, your claim may be denied.

- Illegal Construction: Any portion built without municipal approval (like Meerut Development Authority) will not be covered.

- Pre-existing Damage: You cannot buy insurance for a building that already has structural flaws to claim repairs later.

Step 7: Factor Cost into Your Budget and BOQ

As a professional construction estimator, I view insurance as a vital component of risk management, not an optional expense. For a standard 2,000 sq. ft. home in Meerut with a reconstruction cost of ₹1 Crore, the annual premium is roughly ₹5,000 to ₹8,500.

When preparing a Bill of Quantities (BOQ), always include the first year’s insurance premium as a distinct line item under “Project Overheads” or “Soft Costs”. This demonstrates professionalism to your clients and ensures their largest asset is protected from the day the foundation is poured. For real estate investors, adding this premium as a fixed operating expense when calculating Net Operating Income (NOI) is essential for an accurate Cap Rate.

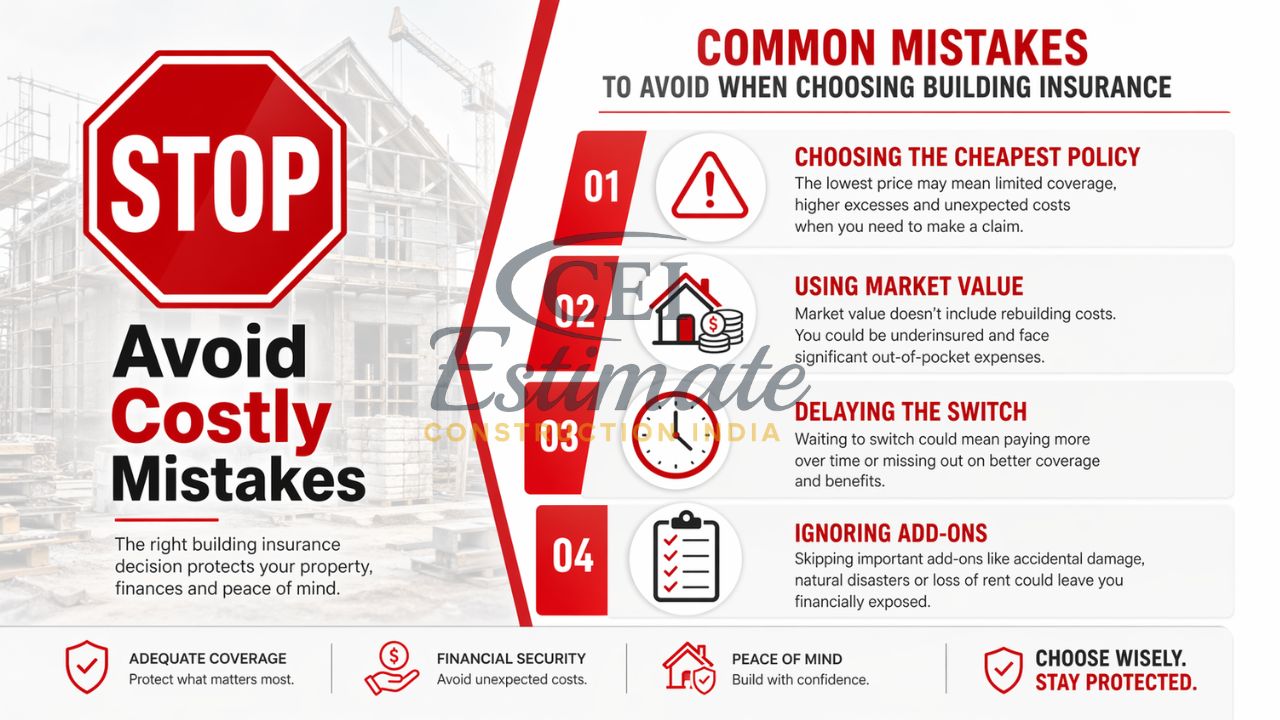

Common Mistakes to Avoid When Choosing Building Insurance

Even with a guide, many fall into these traps when deciding how to choose building insurance:

- Choosing the Cheapest Policy: A low premium often means limited add-ons or a poor claim settlement reputation.

- Using Market Value: Insuring for the market price means you are paying high premiums for land that doesn’t need structural protection.

- Delaying the Switch: Homeowners often forget to switch from “Contractors All Risk” to a standard building policy once the house is finished, leaving a dangerous coverage gap.

- Ignoring Add-ons: Missing out on an “Escalation Clause” can leave you severely under-insured if material costs spike by 15% in a single year.

Conclusion

Mastering how to choose building insurance is the final, non-negotiable step in your construction journey. By following this 7-step process—from assessing your location risks in Uttar Pradesh to calculating an accurate reinstatement value using a BOQ—you bridge the gap between a vulnerable asset and a protected family home. Whether you choose the digital agility of ICICI Lombard or the institutional trust of SBI General, ensure your sum insured reflects 2026’s material rates.

Don’t let your hard work go unprotected. At Construction Estimator India, we specialize in providing professional BOQs and cost estimation services that include accurate insurance valuations from day one. Follow these steps, secure a robust policy, and build with confidence. For expert assistance in project costing that includes comprehensive building insurance analysis, contact Construction Estimator India today.

FAQ Section

How do I choose the best building insurance in India?

Start by assessing your property type (apartment, villa, or rental) and location risks. Use the reinstatement value for your sum insured and prioritize insurers with high claim settlement ratios and robust digital processes.

What is the correct sum insured for building insurance?

It is the reconstruction cost: (Total Carpet Area × Current Construction Rate per sq. ft.). Do not include land value.

Should I buy Bharat Griha Raksha or a traditional policy?

For most residential homeowners, Bharat Griha Raksha is superior because it is standardized, offers automatic 20% contents cover, and has built-in inflation protection.

What add-ons are worth buying for building insurance?

“Escalation Cover” is vital for inflation, while “Loss of Rent” is essential for landlords. “Debris Removal” and “Architect Fees” are also highly recommended.

How much does building insurance cost in 2026?

Annual premiums typically range from 0.15% to 0.40% of the sum insured. For a ₹50 Lakh structure, this is roughly ₹7,500 to ₹15,000 per year.

Is building insurance different for new builds vs existing homes?

Yes. New builds require “Contractors All Risk” during construction, whereas existing homes need a standard building/structure policy like BGR.

Can I buy building insurance for a rental or investment property?

Yes, but you must declare it as “Tenant Occupied” and should include “Loss of Rent” to protect your income stream.

How does building insurance differ from contents insurance?

Building insurance covers the immovable shell (foundation, walls), while contents insurance covers movable items like furniture and electronics.

What should I check before buying building insurance?

Check the insurer’s claim settlement ratio, the “STFI” (natural calamity) coverage, and the list of exclusions like wear and tear or illegal construction.

How do I include building insurance in my construction BOQ?

Calculate the estimated first-year premium (approx. 0.20% of civil costs) and list it under “Project Overheads” or “Insurance & Compliance”.