Imagine you have just completed your dream home in Meerut, Uttar Pradesh, after months of meticulous planning and a significant financial investment. The plaster is fresh, and the premium electrical wiring—which typically accounts for 10–18% of your total construction cost—is safely concealed behind the walls. Suddenly, you find yourself staring at a dozen different insurance tabs on your browser, wondering which is the best home insurance in India to protect this massive asset. Whether you are in Noida, Delhi-NCR, or a growing tier-2 city, the confusion is real. Every insurer claims to be the “best,” but their policies often look like a maze of legal jargon and fine print.

The truth is that there is no universal “best” home insurance that fits every single person perfectly. The ideal choice for you depends entirely on your specific property type—be it a high-end apartment, an independent villa, or a rental property—as well as your budget, location risks, and claim process preferences. However, in 2026, there is a clear frontrunner for the title of the most reliable base policy: the Bharat Griha Raksha (BGR). Mandated by the IRDAI, this standardized policy has transformed the landscape by offering uniform protection, affordability, and automatic features that were previously complex add-ons.

In this comprehensive guide, we will explore why Bharat Griha Raksha is often the top choice for Indian homeowners, compare the leading insurers in the market, break down the realistic costs for 2026, and show you how to properly factor these insurance premiums into your construction cost estimates or Bill of Quantities (BOQ). By the end of this article, you will have a clear roadmap to selecting the protection that ensures your home remains a safe haven, not a financial liability.

Why There Is No Single “Best” Home Insurance for Everyone?

When asking which is the best home insurance in India, you must first look at the unique anatomy of your property. A homeowner in a seismic zone like Delhi-NCR or Meerut has different risk priorities compared to someone in a coastal region. Similarly, the insurance needs of a landlord in Uttar Pradesh are vastly different from those of a tenant in a Noida high-rise.

Several factors determine the “best” policy for your specific scenario:

- Property Type: New builds require coverage based on current reconstruction costs, while older apartments might focus more on contents and internal fixtures.

- Occupancy: If you live in the house, you need comprehensive cover for both structure and contents. If you are a rental property investor, you primarily need building insurance to protect your capital asset.

- Mortgage Status: Banks and lenders like SBI or HDFC often mandate specific structural insurance terms to protect their collateral.

- Location Risks: Properties in areas prone to localized flooding or earthquakes (Zones IV and V) require insurers with robust “Fire and Special Perils” track records.

- Desired Add-ons: You might value specialized covers like “Loss of Rent” or “Temporary Resettlement” more than a basic premium discount.

Ultimately, the best policy is the one that aligns your reconstruction value with a seamless claim settlement experience when disaster strikes.

Why Bharat Griha Raksha is Often the Best Home Insurance in India?

Since its introduction in April 2021, the Bharat Griha Raksha (BGR) policy has become the benchmark for home insurance in India 2026. The IRDAI designed this policy to eliminate the deep-seated confusion regarding insurance terminology that often led to rejected claims. It is widely considered the best Bharat Griha Raksha policy framework because it provides a uniform level of protection across all general insurance companies in the country.

Key advantages that make BGR the top choice include:

- Standardized Coverage: Whether you buy it from a public sector giant or a private digital insurer, the core coverage against fire, floods, earthquakes, and riots remains identical.

- Automatic Contents Cover: One of the most consumer-friendly features is the automatic inclusion of general home contents coverage. If you insure your building, the policy automatically covers contents up to 20% of the building’s sum insured (capped at ₹10 lakh) without requiring a tedious itemized list.

- 10% Annual Escalation: To combat the rising costs of construction materials like steel and cement, the sum insured automatically increases by 10% every year during the policy term.

- No Underinsurance Penalty: In traditional policies, if you were slightly under-insured, your claim amount would be reduced proportionally. BGR removes this penalty if your sum insured is at least 85% of the actual value, providing a major safety net for homeowners.

- In-built Benefits: It includes essential covers like “Loss of Rent” and “Rent for Alternative Accommodation” as standard features, rather than expensive optional riders.

Top Home Insurance Companies Offering the Best Policies in 2026

While the BGR policy structure is standardized, the “best” experience comes down to the insurer’s claim settlement ratio, digital interface, and additional rider options. Here is a comparison of the top home insurance companies India for 2026.

| Insurer | Core Strength | Claim Experience | Best Suited For |

|---|---|---|---|

| HDFC ERGO | High trust and digital ease. | Excellent; fast processing via app. | Tech-savvy urban homeowners. |

| ICICI Lombard | Long-term discounts and wide reach. | Robust; multi-channel support. | Homeowners seeking 5-10 year plans. |

| Bajaj Allianz | Comprehensive add-on packages. | Very good; strong surveyor network. | Premium villas and independent houses. |

| SBI General | Vast network in Tier-2/3 cities. | Reliable; preferred for home loans. | Property owners in cities like Meerut. |

| Tata AIG | Transparent wording and expertise. | High quality; detailed assessments. | High-value property investors. |

| Go Digit | Simple, jargon-free digital process. | Fast; smartphone-enabled claims. | First-time home insurance buyers. |

| New India Assurance | Stability of a Public Sector Undertaking. | Traditional; deep local presence. | Those prioritizing long-term stability. |

Each of these companies offers the Bharat Griha Raksha policy as their primary home insurance product. When looking for the best building insurance India, consider ICICI Lombard for their competitive long-term protection discounts or HDFC ERGO for their seamless integration with home loan requirements.

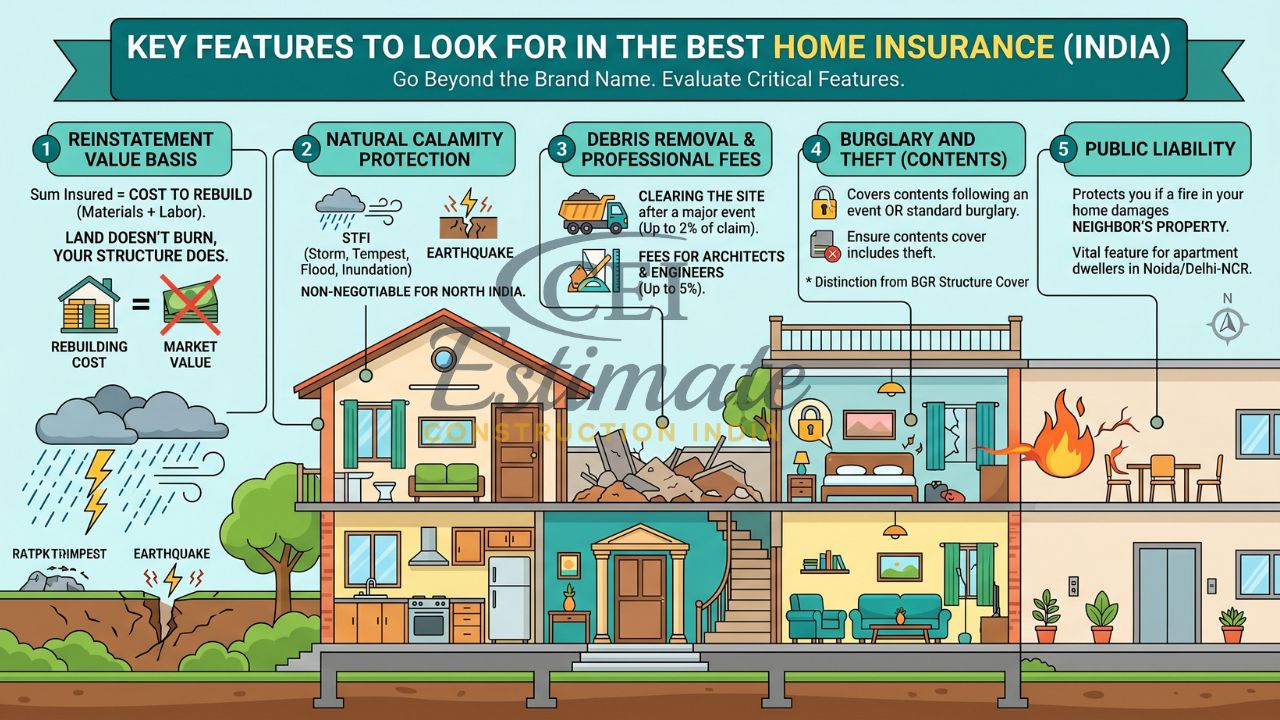

Key Features to Look for in the Best Home Insurance

To ensure you are getting the best home insurance in India, you must look beyond the brand name and evaluate these critical features:

- Reinstatement Value Basis: Ensure the sum insured is based on the “cost to rebuild” (materials + labor) rather than the market value of the land. Land doesn’t burn or wash away; your structure does.

- Natural Calamity Protection: This is non-negotiable for North India. Your policy must cover STFI (Storm, Tempest, Flood, Inundation) and earthquakes.

- Debris Removal & Professional Fees: After a major event, clearing the site can cost a fortune. The best policies cover debris removal (up to 2% of the claim) and fees for architects or engineers (up to 5%).

- Burglary and Theft: While BGR covers structure, ensure your contents cover includes theft following an event or standard burglary.

- Public Liability: This protects you if a fire in your home damages a neighbor’s property—a vital feature for apartment dwellers in Noida or Delhi-NCR.

How Much Does the Best Home Insurance Cost in India?

One of the biggest surprises for Indian homeowners is how affordable the best home insurance actually is. In 2026, the premium for a high-quality BGR policy typically ranges from 0.15% to 0.40% of the sum insured.

Sample Calculation for 2026:

If you have a 1,000 sq. ft. home in Meerut with a reconstruction cost of ₹3,000 per sq. ft., your sum insured should be ₹30 Lakhs.

- Annual Premium: Approximately ₹4,500 to ₹10,000.

- High-Value Protection: For a property with a sum insured of ₹1 Crore, the annual premium can be as low as ₹15,000 to ₹25,000 depending on the location and age of the building.

Factors that can lower your cost include choosing a long-term tenure (up to 10 years), having fire safety equipment installed, or living in a lower seismic zone. For construction estimators, including these nominal premiums in the initial project budget demonstrates a high level of professional foresight.

How to Choose the Best Home Insurance for Your Needs?

Knowing how to choose best home insurance involves a practical, step-by-step approach:

- Assess Your Property: Determine if you need only building cover (for landlords) or a comprehensive package (for residents).

- Calculate Reinstatement Value: Use current 2026 material and labor rates. Don’t guess; an accurate BOQ from a professional estimator is invaluable here.

- Perform a Home Insurance Comparison India: Use digital platforms to compare BGR quotes from at least 3-4 top insurers like HDFC ERGO or ICICI Lombard.

- Evaluate Add-ons: Decide if you need extra protection for high-value jewelry or specific equipment.

- Check Claim Settlement History: Look for companies with a high settlement ratio and a reputation for fair assessments.

- Read the Fine Print: Be aware of exclusions like gradual wear and tear or pre-existing structural issues.

Building Insurance vs Full Home Insurance – What You Really Need

A common point of confusion is whether to buy “Building Insurance” or “Home Insurance.”

- Building Insurance (Structure Only): This protects the physical shell, plumbing, and wiring. It is ideal for landlords or builders who are not living in the property.

- Full Home Insurance (Package): This covers the building structure PLUS your movable contents like electronics and furniture.

If you live in the property, you always need the full package. The price difference is often negligible, but the protection for your lifestyle assets is significant. For a new home builder in Meerut, starting with building insurance and upgrading to a full package upon move-in is the smartest financial move.

Conclusion

Determining which is the best home insurance in India ultimately comes down to finding a balance between robust coverage and a reliable claim experience. While no single company is perfect for everyone, the Bharat Griha Raksha policy stands out as the best base choice for the vast majority of Indian homeowners in 2026 due to its standardized and transparent nature. Whether you choose a digital-first insurer like Go Digit or a traditional giant like ICICI Lombard, ensure your sum insured reflects the true cost of reconstruction.

Don’t leave your most valuable asset to chance. Compare policies today based on your specific property needs and location risks. For professional assistance in creating an accurate BOQ and construction cost estimation that properly includes your home insurance premiums, contact Construction Estimator India. We help you build with confidence and protect with precision.

FAQ Section

Which is the best home insurance in India in 2026?

The “best” varies by need, but the Bharat Griha Raksha (BGR) policy offered by insurers like HDFC ERGO, ICICI Lombard, and Bajaj Allianz is widely considered the best standard choice for its comprehensive and transparent coverage.

Is Bharat Griha Raksha the best home insurance policy?

Yes, for most homeowners, it is the best base policy because it is IRDAI-mandated, includes 20% automatic contents cover, and has a 10% annual sum insured escalation feature.

How do I choose the best home insurance company?

Look for a high claim settlement ratio, ease of digital claim filing, and competitive premiums for long-term policies (up to 10 years).

What is the difference between building insurance and home insurance?

Building insurance covers only the physical structure, while home insurance is usually a package covering both the structure and the contents inside.

How much does the best home insurance cost in India?

Annual premiums typically range from ₹3,000 to ₹8,000 for a sum insured of ₹20 Lakhs, depending on the insurer and location.

Does home insurance cover earthquake and flood?

Yes, under the standard Bharat Griha Raksha policy, natural calamities like earthquakes, floods, and storms are covered by default.

Which company has the best claim settlement for home insurance?

Companies like HDFC ERGO and ICICI Lombard are known for high settlement ratios and efficient digital claim processes in 2026.

Can I buy home insurance for a new build property?

Yes, but ensure it is based on the reinstatement value. For properties still under construction, you actually need a “Builder’s Risk” or “Contractor’s All Risk” policy.

Is home insurance mandatory for home loans?

While not mandatory by national law, most banks like SBI and HDFC require building structure insurance to approve and maintain a home loan.

How to include home insurance cost in my construction estimate?

Include it as a “soft cost” in your Bill of Quantities (BOQ), typically calculating the premium as 0.20% of the total estimated construction cost per year.